- 11 Jan 2023

- By API Magazine

Borrowers are refinancing in record numbers as their lower-priced fixed rate loans end, only to be switched to higher priced variable rates.

A Google analysis in 2022, conducted by a Queensland bank, found that the number of people searching the term ‘refinancing’ had increased by a staggering 5,000 percent.

Helen Avis, Director of Finance, SMATS Group

Lending indicator data released Friday (13 January) from the Australian Bureau of Statistics (ABS) shows a whopping $19.5 billion worth of mortgages were refinanced in November – the highest monthly amount in Australian history.

This figure smashed the previous record set in September 2022 by almost $1 billion.

“Recent ABS data has revealed that enormous numbers of borrowers are refinancing their home loans, indeed, the past six months have been the six biggest months in refinancing history,” Helen Avis, SMATS Group’s Director of Finance, said.

“Part of the reason so many borrowers are refinancing right now is because many lenders charge lower interest rates to new borrowers than loyal customers, as shown by Reserve Bank data.

“In October, owner-occupiers who took out new variable loans were charged, on average, 0.51 percentage points less than owner-occupiers with existing loans.

“Refinancing to a comparable lower-rate loan could potentially save tens of thousands of dollars over the life of your loan.”

Megan Keleher, Chief Customer Officer, Great Southern Bank

The source of the Google analysis, the Great Southern Bank’s Chief Customer Officer, Megan Keleher, said rising interest rates and the increased cost of living have affected household budgets and driven more customers to seek options to save on their home loans.

“They’re using the internet to find out how much they can borrow, how to refinance, and what support may be available for first home buyers.

“Using tools like a refinance calculator can really help; we’ve seen a 16 per cent increase in people using our refinance calculator over the last three months,” Ms Keleher said.

Negotiating a lower rate with their lender or switching in pursuit of a better deal is one of the best ways for mortgagees to prepare for even higher interest rates, Canstar’s Financial Services Group Executive and chief spokesperson, Stephen Mickenbecker told API Magazine.

“The Canstar Consumer Pulse Report released recently, found just a small proportion of mortgage holders (15 per cent) have switched lenders in the past year and secured a better deal, while only 8 per cent tried and failed. This means 77 per cent of borrowers could potentially be paying a lot more for their loan than what is on offer in the market today,” he said.

Stephen Mickenbecker, Group Executive, Financial Services & Chief Commentator, Canstar

Released in mid-December 2022, the Canstar report surprisingly revealed that when it came to mortgage holders coping with higher interest rates, almost one in two – 48 percent – of homeowners with a mortgage and 37 percent of investors with a loan – are unsure how much their mortgage interest rate has risen since the Reserve Bank started aggressively lifted interest rates in 2022.

“When asked how prepared they are for even higher interest rates, close to two-fifths (39 per cent) of homeowners and more than one-quarter (27 per cent) of investors are not prepared. The majority of these indicated they would need to cut their living costs further to make ends meet,” Mr Mickenbecker said.

“It’s disappointing that borrowers are not more engaged with getting a better deal, either from their own bank or by switching banks.

“Most borrowers are paying interest rates well above the relatively low rates being offered to new customers, and the monthly savings are too big to ignore.

“Borrowers can’t wait until they are unable to pay the bills to refinance into a lower rate loan as by then their desperation will be matched by lender aversion and they may find themselves out of luck with new lenders,” he said.

Fixed Rates About To Fall Off Cliff

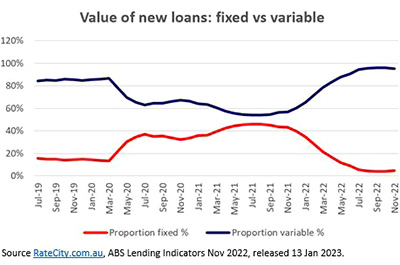

As the countdown to the fixed-term cliff approaches for many property owners, few new borrowers are fixing their home loans.

The housing market, as well as borrowers, will be faced with $478 billion in fixed rates loans transferring to variable rates.

This is the so-called mortgage cliff that arises from the rollover of fixed rate mortgages taken out mid-2020 to early 2022 at interest rates around 2.5 per cent, and transitioning within the next 18 months into loans priced at 5.5 to 6 per cent. There is a large proportion of these loans falling due before the end of 2023.

“Unlike a year earlier when about half of borrowers were doing so, only 4 per cent of borrowers fixed their loans – both new loans and refinance – in October (the most recent data available).

“By contrast, 44 per cent of borrowers fixed in October 2021 and 46 per cent in August 2021, when fixing peaked,” Ms Avis said.

“While the Reserve Bank only started increasing the cash rate in May 2022, lenders knew it was coming, so they’d already started raising interest rates on their fixed- rate loans.

“In response, borrowers had begun shifting towards lower-rate variable loans.”

This is confirmed by Reserve Bank data on new owner-occupied loans.

In October 2021, the average interest rate on a new fixed loan (with a fixed period of three years or less) was 0.63 percentage points lower than a new variable loan. By February 2022, new fixed loans had become 0.09 percentage points dearer; by May they’d become 0.70 percentage points dearer.

That has since declined – by October, they were only 0.30 percentage points dearer.

Mr Mickenbecker said 39 percent of homeowners and 27 percent of borrowers polled in Canstar’s Consumer Pulse Survey in 2022 were unprepared for further rate rises.

“According to the survey, a small group of property owners (5 per cent) say they are considering selling in the next two years because they can’t afford higher loan repayments.

“While this is a small minority, the group is likely to be concentrated among more recent borrowers, with their larger loans and repayments, who have no time to have put together a buffer and have low equity.

“The impact of interest rate rises and falling property prices spreads unevenly, and recent first home buyers who overreached to get into the market will carry more than their share of the pain,” Mr Mickenbecker said.

Mortgage Stress Mounting

That pain will translate into falling house values and mortgage stress.

When surveyed for the Pulse Report, close to two fifths (39 per cent) of homeowners and more than a quarter (27 per cent) of investors were not prepared for higher interest rates.

The majority of these indicated they would need to to cut their living costs to make ends meet.

“If the price declines deepen to the point where many new loans in particular start falling into negative equity, the concern will heighten.

“At that stage, individuals will be feeling extreme pain and the system will be at risk,” Mr Mickenbecker said.

“With the full force of interest rate increases yet to take its toll, borrowers in particular look to be on a knife-edge, and have a limited buffer.

“A worthwhile New Year’s resolution for Australians might be to sit down and do a refresh of their household budget to work out a way to restore their financial resilience.”

Can There Be High Demand For Housing With High Interest Rates?

Dr Kristle Romero Cortes, Economist and real estate markets expert, UNSW Business School of Banking and Finance associate professor

Economist and real estate markets expert, UNSW Business School of Banking and Finance associate professor Dr Kristle Romero Cortés, told API Magazine she believes housing demand can withstand these financial pressures.

“Intrinsically, mortgage rates and house prices are related via supply and demand channels. If we see that the trend is that home purchases become unaffordable due to repayments, you may see a decrease in home purchases.

“However, high-income earners need more incentive to accept lower prices when selling their homes if they can afford their repayments.

“The repayment rates would need to reach a level that selling the house now to purchase one in the future eventually becomes an attractive option.

“There has already been a move to short-term fixed loans to stabilise payment expectations. This will remain the case for borrowers; it will be interesting to see how the long-run rates on fixed loans react (3 to 5 years) because, currently, those are priced high,” Ms Cortes said.

This article, first published 11 January, was updated on 13 January with the latest ABS refinancing data.

Article Q&A

What is a mortgage cliff?

When interest rates were at historic lows during Covid, many homebuyers entered the property market on very low fixed rate loans. The terms of a large proportion of these loans end over the next 12-18 months, meaning billions of dollars in loans will switch to higher variable rate mortgages. This steep, looming rise in repayments is termed a mortgage cliff.

Is now a good time to refinance the home loan?

A Google analysis in 2022, conducted by a Queensland bank, found that the number of people searching the term ‘refinancing’ had increased by a staggering 5,000 percent. Australians refinanced $17.8 billion of mortgages in October, close to the August record volume. Property finance experts suggest now is a good time to sit down and do a refresh of the household budget to work out a way to restore financial resilience.