Buying a property in Australia can be a significant milestone and a complex process that requires careful consideration of various factors. From navigating the property market to managing finances and legalities, there are numerous aspects to address to ensure a successful purchase. We’ve compiled our Top 9 factors you need to consider when buying Australian property, covering everything from market research to the settlement process.

1) Property market research

Conduct thorough research on the property market, including historical sales data, recent trends, and projected growth. Familiarise yourself with the local market conditions and property prices in the area you’re interested in. If it’s an investment property, rental data will also be important to analyse.

Will this be the property that you and your family be living in long term? If yes, and you have young or school aged children you might want to look at the local amenity of the suburb too – factor in local schools, transport hubs and accessibility, shopping centres and activities (parks and recreation) in the area.

2) Budget and affordability

Determine your budget and assess your financial capacity to purchase a property. Consider factors such as your income, savings, borrowing capacity, and any additional costs associated with buying a house, such as stamp duty, legal fees, and ongoing maintenance.

3) Government grants and incentives

Research and determine if you’re eligible for any government grants or incentives available to first-time home buyers or specific property types. These can provide financial assistance and help reduce the overall cost of buying a house. We are here to help you every step of the way and have access to all updated information and grants that you may apply for.

4) Financing options

Explore different financing options, including home loans from various lenders. Compare interest rates, loan terms, fees, and features to find the most suitable loan for your needs. Consult with your mortgage broker to help navigate the lending process. Ensure you get pre-approval before you start seriously searching for property to buy. Our team is happy to assist with getting the pre-approvals you need.

5) Contract of sale and legal advice

Seek legal advice from a licensed conveyancer or solicitor to review the contract of sale and ensure all legal obligations are met. They will can guide you through the legal aspects of the purchase, including title searches, property transfers, and any special conditions in the contract.

6) Building and pest inspections

Consider obtaining building and pest inspections to identify any hidden problems with the property, such as termite infestations or structural issues. These inspections can help protect your investment and potentially negotiate repairs or a price reduction.

7) Property insurance

Arrange property insurance to protect your investment against potential risks, such as fire, theft, or natural disasters. It’s important to have adequate coverage in place before settlement, you may have to consider house and contents insurance as well as landlord insurance for investment properties.

8) Settlement process

Understand the settlement process; this involves finalising the purchase and transferring of Australian Property ownership. Your nominated conveyancer or solicitor will ensure all necessary paperwork, payments, and contractual obligations are fulfilled on time.

Purchasing a property in Australia demands thorough research, meticulous planning, and careful attention to detail. By considering the key factors outlined above including market research, budgeting, financing options, inspections, legalities, insurance, government incentives, and the settlement process, you can navigate the property buying journey with confidence and make informed decisions that align with your goals and objectives. Whether you’re a first-time homebuyer or an experienced investor, being well-informed and proactive can help you achieve success in the Australian property market.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

Six Sydney property experts reveal the suburbs and property types real estate investors should be looking to buy in 2024.

The Sydney property market has undeniably become unaffordable to many, with a median dwelling value $300,000 above the next highest median, Canberra, and almost $400,000 above Melbourne’s.

But like all city property markets, it is a diverse real estate landscape with its mix of sour lemons and appetising fruit cocktails awaiting property investors.

Despite its wince-inducing median dwelling value of $1,139,375 the city as a whole last month still notched up another 0.3 per cent price uptick, according to CoreLogic.

With price trends still in the positive, some suburbs are still delivering the type of capital growth, complemented by high rental returns, that captures the attention of property investors.

Houses remain the preferred investment vehicle but unit prices have been outstripping houses in recent months.

PropTrack’s Senior Economist, Eleanor Creagh, on Friday (11 April) said that in Sydney, six of the top 10 suburbs where unit growth is outpacing house price growth this year are in the Inner West, Inner South West, or City and Inner South, namely Dulwich Hill, Mortdale, Rozelle, Bexley, Balmain and Petersham.

Of all the suburbs in Australia, the house price premium over units is the most extreme in Clontarf, Queens Park, Bellevue Hill, and Vaucluse, in Sydney’s Northern Beaches and Eastern Suburbs. In these suburbs, houses can cost almost 10 times as much as units, with the difference in value ranging from $3 to $8 million.

So where should property investors turn their attention in Sydney?

Six property experts spoke to API Magazine and shared their thoughts on the suburbs that offered the best prospects for medium-term return on investment.

From the top end of town to more affordable outskirt suburbs, here are the suburbs they think will have investors sipping cocktails on the beach in the future.

Sydney’s 2024 Property Investment Hotspots

Aaron Downie, founder and buyers agent, Mackenzie Property Group

The East, Lower North Shore, and Northern Beaches could potentially see above-average capital growth

Suburbs like Coogee, Neutral Bay and Curl Curl really stand out. These areas, with median house values in the $3m to $4 million range, are known for their quality of life, access to amenities and strong demand from families, professionals and investors, which may drive property values up.

I anticipate units to continue outperforming in the Sydney market, driven by an upturn of investor interest, as well as by downsizers and those preferring the lifestyle Sydney offers over relocation alternatives.

Allen Habbouchi, Head of Project Sales & Distribution, aussieproperty.com

Sydney’s top three suburbs likely to keep delivering stronger than normal trends are Coogee, Kingsford and Kensington.

This is mainly due to their strategic positioning within 10km of the CBD, university campuses, beaches and infrastructure.

Two of our commentators named Coogee as a suburb worthy of property investor attention.

They offer lifestyle and investment opportunities to residents and investors alike.

Ultimately these factors could potentially contribute to deliver stronger than expected growth for houses and units.

Locations like Liverpool and Campbelltown are already seeing 17 per cent annual increases in searches and this renewed interest will flow on to higher prices with the increased demand.

Much of the outperformance of the luxury end of the market has been due to the immunity of that segment to interest rate rises compared to the lower quartile. With the rate cuts now priced into rate market into the end of the year and start of 2025, we expect some of the serviceability constraints and buffers to ease.

Five Dock is also a suburb seeing a lot higher search volumes, in Sydney’s Inner west, where the Sydney Metro West project station is underway, which will enhance its already good transport links. It is close to the CBD and is relatively affordability compared to other nearby locations.

The Agency, CEO of Real Estate, Matt Lahood

Sydney’s price trajectory is slowing due to high interest rates and people having less disposable income. People don’t have the borrowing power of previous years, which is reducing the rate of growth.

The most likely places to resist this price pressure are Alexandria, Burwood and, on the Central Coast, Kincumber.

Liam Carmody, General Manager, Palise Property

Despite the significant median price difference compared to other capital cities, outer suburbs in Sydney may not necessarily be the best performing.

This can be attributed to various factors, including infrastructure, amenities, employment opportunities and lifestyle preferences.

Inner suburbs often offer better access to amenities and employment hubs, attracting higher-income individuals willing to pay premium prices.

Additionally, limited supply and high demand in inner suburbs contribute to price growth. In contrast, outer suburbs may have more affordable housing but lack the same level of amenities and infrastructure, resulting in comparatively slower price growth.

Three suburbs positioned to deliver stronger than trend capital growth this year could include:

Surry Hills: An inner-city suburb experiencing gentrification and attracting young professionals and investors.

Marrickville: Known for its cultural diversity and vibrant lifestyle, with ongoing development projects driving demand.

Parramatta: Sydney’s second CBD undergoing significant infrastructure improvements and development, and offering investment opportunities.

Julian Khursigara, Partner, Search Party Property

We would expect demand for units to remain particularly strong in metro areas as affordability issues persist and investor interest picks up throughout the year.

Some recent industry surveys have indicated a growing trend of families opting to downsize in Sydney.

Along with seasoned Sydney investors returning to the market, this is probably another reason for the recent exuberance for units and townhouses.

By comparison, interstate investor attention is largely focused elsewhere, and first home buyers are also finding it increasingly difficult to break into the Sydney market.

Six property experts interviewed by API Magazine identified a range of suburbs where property prices were expected to deliver strong capital growth, ranging from affluent coastal areas like Coogee to outer suburban Endagine.

What is the median property price in Sydney?

Despite its wince-inducing median dwelling value of $1,139,375 the city as a whole last month still notched up another 0.3 per cent price uptick, according to CoreLogic.

Our Top 5 2024 Tips For Accessing If Its Time For An Update To Your Home Loan.

Refinancing a home loan can offer financial benefits, such as lower interest rates, improved loan terms, or access to additional funds. However, deciding when to refinance requires careful consideration of various factors.

1) The Interest Rate Environment

One key factor to consider when contemplating refinancing is the prevailing interest rate environment. If interest rates have significantly dropped since your initial loan, it may be a good time to refinance. By securing a lower interest rate, homeowners can potentially reduce their monthly repayments and save money over the life of the loan.

2) Better credit.

If your creditworthiness has improved since obtaining your original loan, you may qualify for better loan terms and interest rates. Factors such as an improved credit score, increased income, or reduced debt can positively impact your eligibility for more favourable refinancing options if you have gone with a non-banking lender.

3) Changing Financial Goals.

Changing financial goals can also prompt refinancing. For instance, if you wish to consolidate multiple debts, such as credit cards or personal loans, into a single mortgage with a lower interest rate, refinancing can provide a solution. Additionally, if you want to access the equity in your home for home improvements or investments, refinancing may be a viable option.

4) Flexibility and options.

Refinancing allows homeowners to reassess their loan features and seek more flexibility. If your current loan lacks desirable features, such as an offset account, redraw facility, or the ability to make extra repayments, refinancing can help you secure a loan that aligns with your preferences and financial needs.

It can also provide an opportunity to review the fees and charges associated with your current loan. Evaluate the costs of refinancing, such as application fees, valuation fees, and legal fees, against the potential savings or benefits gained from the new loan. It’s important to carefully compare the costs and benefits to ensure that the overall financial outcome is actually a positive one.

Keep an eye out for the cash back incentives that some banks offer, these can cover the costs of the refinance and sweeten the deal with some of the bonus left over. Your mortgage broker will be able to assist in comparing the best deals for you when it is time to refinance.

5) Loan structure.

If you currently have a fixed-rate loan and interest rates have fallen significantly, or have a variable-rate loan and interest rates have increased or predicted to rise, refinancing to a different structured loan could be advantageous. However, be aware of potential break fees associated with terminating a fixed-rate loan prematurely & the break fees alongside potential savings to determine if refinancing is economically beneficial in your situation.

You can quickly weigh the costs of breaking the fixed term by simply reaching out to the bank and asking them what the break cost of the fixed loan is. They should be able to give you an answer on the spot.

How can Specialist Mortgage Assist You?

Seeking advice from mortgage professionals can provide valuable insights and guidance in determining the optimal time to refinance. At Specialist Mortgage our brokers can help assess your financial situation, analyse loan options, and recommend the most suitable refinancing strategy based on your individual circumstances and goals.

Deciding when to refinance requires careful evaluation of various factors. Monitoring the interest rate environment, assessing improved creditworthiness, changing financial goals, and reviewing loan features and fees & weighing the costs and benefits are crucial considerations, especially when purchasing Australian property or applying for an Australian home loan as a expat.

By understanding the appropriate circumstances and conducting thorough research, individuals can take advantage of refinancing opportunities to achieve their financial objectives and potentially save money over the long term.

Is it time for a refinance? Still unsure? Touch base today and we’ll do a deep dive into your situation and see if it’s worth it.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

Our Top 10 Suburbs To Watch In 2024

Perth property prices are soaring but investors are contending with the high prices by searching out smaller properties such as villas and select hotspot suburbs.

Perth’s red hot property market has many feeling as if they’ve missed a generational period of price growth.

East Coast buyers agents are overinflating price tags for eager eastern states buyers, first home buyers desperate to escape the nation’s most stressed rental market are pushing prices at the lower end of the market through the roof, and villas, flats and townhouses are being embraced like never before.

In a rapidly rising market it can be difficult to ascertain true value.

Perth property overall, already the fastest growing market in the country, is forecast to rise at least another 10 per cent this year, on the back of 18.3 per cent growth in the 12 months to the end of February.

Some investors are now asking if the market is still delivering investment potential when competitive buyers are outbidding each other on listed prices by 10 per cent or more.

With that 10 per cent get-in-the-game increment potentially erasing a year’s growth, and stamp duty and other transaction and settlement costs, where does long term value lie?

Supply, a strong economy and population growth remain the key drivers of Perth’s market.

But if global economic and geopolitical factors were to quell the current high levels of demand and persistent global inflation continued to keep interest rates locked in, investors could feasibly be looking at lengthier times to recoup their investment.

Top 10 Unit And House Suburbs For Price Growth

Whether its location, price range or property type, there are sectors of the market that are in greater demand than others and with resilient prospects going forward.

Most of the action is in the upper and lower portions of the market in terms of price, with outer suburban houses in the $400,000 to $550,000 price range experiencing annual price growth of more than 25 per cent, while suburbs in the $1.1 million to $1.4 million range are moving at that same rate of knots.

TOP SUBURBS BY ANNUAL CHANGE IN MEDIAN HOUSE PRICE

Price growth in the year to February 2024 (28 or more annual sales; <1HA) Source: REIWA.

Villas and townhouses are fairly similar to houses. They may not be set on their own block, but they often come with some land, usually in the form of private courtyards, and the low-maintenance aspect also appeals to buyers.

“There is often talk about density in Perth and these stats show buyers are quite willing to embrace medium density living, we just need to build more of these types of homes and in locations where buyers want to live,” Ms Hart said.

Within six kilometres of the Perth city centre, two-bedroom apartments such as this one in The Crest Burswood for around $700,000.

The growth in the median sale price for flats reflected their affordability.

“Flats are often a great way for first home buyers to enter the market,” she said.

“They also offer good value for investors.”

Units are now selling 13 days faster than they did a year ago.

The growing demand for units is seeing prices start to rise at a greater rate. The median unit sale price increased 1.2 per cent in January and was 3.8 per cent higher year-on-year.

The median house sale price rose 0.8 per cent to $605,000 over the month. This was 10 per cent higher than February 2023.

Perth’s Hotspots That Could Outperform Market

Perth owner occupiers have an appetite for landed property, more so than owner occupiers on the East Coast who have become accustomed to unit living just to be closer to the city centres.

Julie Kelley, Global Sales and Marketing Manager for aussieproperty.com, said a trend was emerging of buyers compromising to be within 10 kilometres of the CBD and shifting their search to townhouses, villas and apartments.

For investors this can be favourable as there is often less maintenance, higher rental yields and lower vacancy rates, in addition to a lower purchase price and reduced stamp duty.

Homes such as this four-bedroom Canning Vale property on a block of 756 square metres is available are available just 17 kilometres from the city.

In Burswood, for example in the The Crest development, and Como, buyers can purchase a two-bed, two-bath, two-car apartment in a complex with resort-style facilities in the $660,000-$770,000 bracket.

When it comes to houses, Ms Kelley said many buyers with a budget of $1 million or less and wanting a large four-bed, two-bath, two-car family home on a good-sized block are expanding their searches to beyond 20 kilometres of the CBD.

“They are well established suburbs, with good amenities and schools, lovely parks and a great sense of community.

“The houses in these suburbs were typically built as house and land packages in well-designed leafy estates from the 1990s into the 2020s, with land releases and new builds continuing even now.”

Buyers with similar budgets and goals looking for homes north of the river and content to settle outside a 20 kilometre range from the CBD, were making houses in suburbs such as Hamersley, Greenwood, Kingsley and Darch highly sought after assets.

Supply Crunch To Linger Despite Government Efforts

Driving the Perth market is an unprecedented housing shortage, with supply and demand disparities at historic levels.

Source: REIWA/Momentum Wealth Research

In response, the Western Australian government has launched initiatives such as the Builders’ Support Facility (BSF), applications for which opened on Monday (11 March), to help boost supply.

Western Australia’s population increased 3.1 per cent in the year leading up to June 2023, the highest growth rate nationwide.

Peter Gavalas, a buyer’s agent from Resolve Property Solutions, said this has far outstripped housing supply, which has been plagued with low completions and dwindling approvals.

“Initiatives like the BSF facility are a positive step but don’t fully address the underlying issues affecting Perth’s housing supply, and as a result Perth’s property prices and rents are likely to continue rising, adding yet more pressure on potential homebuyers and tenants.

“Perth’s property market is in dire straits.”

According to recent REIWA data, the number of listings for sale across Perth plummeted to a record low of 3,648 at the end of December, marking a 23.4 per cent drop from November and a staggering 49.0 per cent decline compared to December 2022.

“The gap between the number of homes available and the number of people wanting them has never been wider, fuelling intense competition among buyers and driving up prices,” Mr Gavalas said.

“Meanwhile, homes are flying off the market, with houses selling in just 10 days on average.”

Article Q&A

Where are property prices growing fastest in Australia?

Perth property overall, already the fastest growing market in the country, is forecast to rise at least another 10 per cent this year, on the back of 18.3 per cent growth in the 12 months to the end of February.

Should property investors buy in Perth?

Some investors are now asking if the market is still delivering investment potential. API Magazine identifies the property types and suburbs best placed to deliver investor returns in 2024 and beyond.

Why are Perth property prices rising so fast?

Supply, a strong economy and population growth remain the key drivers of Perth’s market.

Where are property prices rising fastest in Perth?

As these API Magazine top ten lists show, most of the Perth property action is in the upper and lower portions of the market in terms of price, with outer suburban houses in the $400,000 to $550,000 price range experiencing annual price growth of more than 25 per cent, while suburbs in the $1.1 million to $1.4 million range are moving at that same rate of knots.

Our Top 5 2024 Tips For Accessing If It’s Best To ‘Stay Put’ With Your Current Home Loan.

Refinancing a home loan can be a smart financial move in certain situations, offering potential benefits such as lower interest rates and improved loan terms. However, there are circumstances when refinancing may not be advantageous or appropriate.

1) The Early Bird On Aussie Mortgages.

Refinancing early in the life of a loan may not be financially beneficial. In the initial years, a significant portion of the mortgage repayments typically goes towards interest, and the principal balance may not have decreased significantly. Refinancing too early can result in resetting the loan term and extending the overall repayment period, potentially outweighing any potential savings from lower interest rates.

2) High Break Costs.

If you have a fixed-rate loan and decide to refinance before the fixed-rate period ends, you may incur break costs. These costs are fees charged by the lender for terminating the loan early and can offset any potential savings from refinancing. It is crucial to carefully consider the break costs and compare them against the potential benefits of refinancing before making a decision.

It can be very costly for newly established loans with long loan terms and a long fixed rate period to be ‘broken’. The banks will usually pass off their losses for breaking the fixed term early.

Look at it this way, if you fixed your loan for $500,000 at 6% pa for 4 years, and the variable rate was at 3% pa, the bank would have missed out on 4 years of interest at 3% pa.

3) A little bit weak.

If your creditworthiness has declined since obtaining your current loan, refinancing may not be advisable. Lenders assess credit history and financial standing when considering refinancing applications. If your credit score has significantly decreased or your financial situation has deteriorated, you may struggle to secure a new loan with favourable terms or interest rates.

4) In the Short-Term.

If you plan to sell your property in the near future, refinancing may not be worthwhile – this is especially true if you are thinking about fixing your loan. As mentioned above, this can prove to be quite a costly mistake. The costs associated with refinancing, such as application fees, valuation fees, and legal fees, can erode any potential savings. Consider the break-even point—the time it takes for the savings from refinancing to surpass the costs incurred. If you are unlikely to recoup the costs before selling, it may not be a good time to refinance.

5) Limited Equity.

Insufficient equity in your property or a low property value can hinder your refinancing options. Lenders typically require a certain level of equity or a loan-to-value ratio (LVR) to approve a refinance. If the value of your property has decreased or you have minimal equity, it may be challenging to secure a beneficial refinance deal or access competitive interest rates.

How’s The Australian Property Market Faring?

Refinancing decisions can be influenced by prevailing market conditions. If interest rates are expected to rise or the Aussie housing market is experiencing a downturn, it may not be the right time to refinance. Waiting for more positive market conditions can potentially result in better loan options and interest rates in the future.

Before deciding to refinance, carefully evaluate the potential benefits and savings. Calculate the potential monthly savings on repayments, compare interest rates, and consider the overall financial impact. If the potential benefits are minimal and do not outweigh the costs and effort associated with refinancing, it may be best to postpone the decision. Seeking advice from mortgage professionals can provide valuable insights and assist in determining whether refinancing is the right choice at a given time.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

Experts are divided on the likelihood of an RBA interest rate cut in the next few months, but all agree borrowers are banking on it.

With inflation figures having fallen to the lowest level in almost two years, even the prospect of a cash rate rise in 2024 is up for debate.

Mortgage broker Helen Avis (pictured above left), director of Specialist Mortgage, said her clients would breathe a sigh of relief if there were no further rate hikes over the next 12 months, with many feeling the pinch of the rising cost of living.

“Many buyers are concerned about the prospect of rate increases and their ability to service their mortgage,” Avis said.

“This is particularly evident within the first home buyer market who are often shopping at their maximum borrowing capacity, investors using property as collateral to secure finance, and our overseas clients who are often faced with higher rates than Australian residents.”

High Hopes That Interest Rates Won’t Rise In First Half

Avis said her clients are hopeful rates will remain on hold for the next six months, with most believing they won’t see rate cuts until 2025.

“Nearly all of our clients are choosing variable loans over fixed rates. This is in significate contrast to the height of the pandemic when borrowers were opting for low-rate fixed mortgages.”

Avis said clients’ sentiment towards the property market was still positive, “but they are approaching it with a little more caution”.

She said many clients were factoring in potential rate increases, often looking at property well under their maximum borrowing capacity.

Now is a great time for borrowers to take advantage of the competitive rate market.

“Our brokers are negotiating aggressively with our clients’ existing lenders to get the best variable rates, which is often preferable compared to switching to a new loan provider,” Avis said.

Buyers Need To Spend Within Means

aussieproperty.com buyers agent Julie Kelley said rate relief would instil confidence in the property market.

“As we all know taking on too much debt can lead to unnecessary stress; I always advise clients to shop in their comfort zone,” Kelley said.

“In such a competitive market, I understand buyers can feel frustrated by not being able to secure their dream home due to budget constraints, and they may feel pressured by selling agents to quickly submit an offer above their initial budget. But it’s important not to let emotions take over.

“We always advise our buyers that are considering pushing their borrowing limits to first speak with their mortgage broker and factor in all increased costs such as stamp duty, repayments and LMI before submitting an offer on a property”.

Financial comparison site Mozo’s money expert Rachel Wastell (pictured above centre), money expert at financial comparison site Mozo, said mortgage holders would welcome a rate cut, no matter how small.

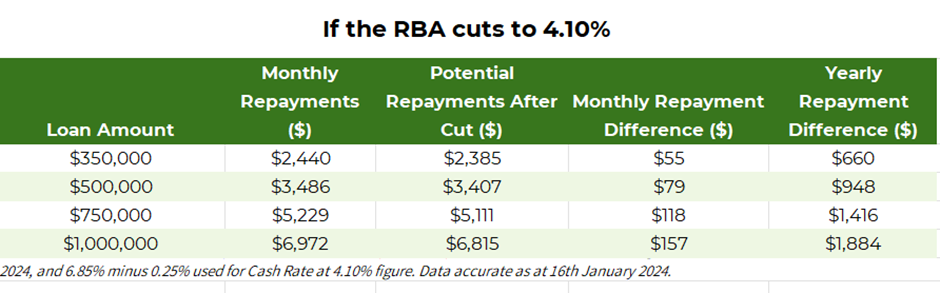

Mozo analysis shows someone with a $1 million mortgage, following a rate cut to 4.1%, will have an extra $157 a month in their pocket, equating to $1,884 a year based on the variable rate staying the same (see Mozo data below).

Source: Mozo

“I think borrowers will be cheering when a rate cut comes through,” Wastell said. “After one of the most aggressive rate hiking cycles since the early 1990s news about rates has unfortunately been quite doom and gloom.”

RBA On Track To Meet Inflation Goal?

Wastell said a rate cut will likely give borrowers some hope that the RBA is on track to meet their inflation target, and that more rate cuts could be on the horizon.

“In a cost-of-living crisis every cent counts; $100 more a month might not seem like much, but for those mortgage holders who have now resorted to credit cards or buy now pay later services to cover their everyday expenses,” Wastell said.

“That $100 could be the difference between clearing those monthly balances or being in the red.”

Despite what borrowers want, Wastell said a rate cut in the next few months was unlikely, as the unemployment rate was holding steady and inflation in services, particularly insurance, was still high.

“Later in the year, if there are no further rate hikes, and the CPI data for the June quarter shows we’re much closer to the RBA’s target of 2% to 3% we will probably see a rate cut or two, but I think it’s important homeowners don’t count their chickens before they hatch.”

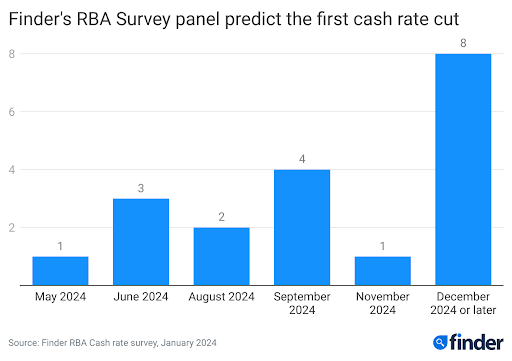

Experts Predict February Cash Rate Pause

In this month’s Finder RBA Cash Rate Survey, 19 experts and economists weighed in on future cash rate moves and almost all of the experts, 89%, said the RBA would hold the cash rate at 4.35% in February.

Head of consumer research at Finder Graham Cooke (pictured above right) said many Australians were in urgent need of reprieve following the last rate rise in November.

“Homeowners are still reeling from 13 rate hikes in the last two years,” Cooke said.

“Our data shows a staggering 40% struggled to pay their mortgage in December. Even though inflation is falling, I expect the RBA will hold the cash rate for most, if not all of 2024.”

While one in three Finder panellists predict a cash rate cut by at least August this year, almost half, or 40%, don’t expect the RBA to start cutting rates until December 2024 or later.

The majority of Finder experts, or 71%, said they expected the cost-of-living crisis to ease eventually in 2024.

“While the gauge remains in the extreme range, it’s likely that this will be where the cost-of-living pressure peaks,” Cooke said. “We expect to see some relief on the horizon, and with a little luck the pressure will reduce slowly over many months.”

Earlier this month, Bank of Queensland chief economist Peter Munckton said talk of rate increases by the RBA this year were “in the rear mirror” and said the big question for 2024 is when would interest rates start to fall.

Investors and first home buyers are making a big return to the property market, with three state capitals seeing particularly strong real estate demand and higher loan values.

As the inflation beast is gradually brought to heel, borrowers are becoming increasingly confident that interest rates have reached their zenith and are again borrowing with relative gusto.

It’s first home buyers who are leading the charge, with investors not too far behind.

The latest Australian Bureau of Statistics (ABS) data shows that in November new home and investment property loans were up 13.1 per cent over the year.

The value of new loan commitments for investors was rising higher than owner-occupier borrowers. Investment lending increased by 18 per cent to reach $9.72 billion while owner-occupier new loan commitments were up only 10.6 per cent over the year to reach $17.86 billion in loans.

But it was first home buyer activity that stood out, with a 25.8 per cent increase in the value of new loan commitments for first-time buyers that saw the value of new loans reach $5.25 billion.

Source: CoreLogic

Canstar’s lending expert, Steve Mickenbecker, said the figures suggested Australian had confidence in the property market excelling in 2024.

“You could say investors are back, with new lending up by 18 percent year-on-year, suggesting they hold a healthy expectation for property prices over the coming few years.

“Looking at the number of buyers, first home buyers’ participation represents 37 percent of all new loans.

“First home buyers have in recent years had to weather the impact of rate rises on borrowing power.

“Canstar’s analysis shows for the average income, a solo borrower has seen their borrowing capacity fall since April 2022 by $137,000 and likewise, a double-income couple’s budget has been depleted by $331,000.”

Real Estate Institute of Australia (REIA) President, Leanne Pilkington, expressed relief that there was a return of investors.

“The results follow the latest ABS data showing the consumer price index rose 4.3 per cent in the 12 months to November 2023, down from 4.9 per cent per cent in October.

“The 13 interest rate rises have finally curtailed inflation, with all signs showing the economy is now heading in the right direction.”

Ms Pilkington said owner-occupier loans recorded moderate growth in November with some states such as Tasmania and NSW showing signs of stabilising.

Investors as a portion of total lending by state (based on value, excluding refinancing)

Source: CoreLogic

ABS data shows new loan commitments in Queensland rose 3.3 per cent, Victoria rose 2.0 per cent, South Australia rose 6.9 per cent, in the Australian Capital Territory rose 9.4 per cent and in the Northern Territory rose 6.0 per cent while New South Wales fell 1.1 per cent, in Western Australia fell 2.9 per cent and Tasmania fell 15.2 per cent.

While new loans may have slipped in Western Australia, the value of the average loan size reached record levels there, as well as in Queensland and South Australia, reflecting the strong capital growth in those property markets over the past year.

Queensland reached $557,510, South Australia $510,057 and Western Australia $497,275 in average loan size.

Helen Avis, Director of Finance, Specialist Mortgage, said Perth was seeing a lot of interest from eastern states buyers.

“With stock levels so low – there are now just over 3,000 properties for sale in Perth and many are being sold as soon as they are listed – it’s little surprise that borrowers are taking bigger loans to achieve their property goals.”

Maree Kilroy, Senior Economist for Oxford Economics Australia, agreed that Perth could expect further strong growth in 2024.

Following the rebound over 2023, we expect 2024 will be a softer year with home prices increasing a more muted 2.7 per cent nationally.

“Units are expected to outpace houses as affordability pressures, migration patterns, and weak apartment completion volumes intensify competition in the city apartment markets.

“While Sydney and Melbourne are expected to record relatively softer growth, Perth is well-equipped to lead the pack as the city develops a more sizeable dwelling stock deficiency.”

Rate Cuts Could Mean Game On For Refinancing

Refinancing largely stabilised in November after three months of steep declines.

The value of refinanced mortgages rose slightly in the month of November, lifting by a modest $121 million – the first increase in four months.

RateCity.com.au research director, Sally Tindall, said that while we’re now well past the peak in refinancing, the value of mortgages switching each month is still at elevated levels.

“Rock bottom rates in 2021 might have shone a spotlight on refinancing, but the rising cash rate has been the blowtorch that’s spurred many borrowers into action.

“The latest ABS data shows over 700,000 mortgages have refinanced since the start of the rate hikes, switching more than $360 billion worth of loans.

“Refinancing could well drop further in the first half of 2024, however, if we do see cash rate cuts later in the year it could be game on for some borrowers ready for their next move.

“It’s fantastic to see first home buyer numbers rising again in the month of November, despite rising rates and property prices.

“These numbers are likely to lift further in 2024, particularly when the government’s much touted Help to Buy scheme finally gets up and running.

“While this scheme will help lower-income first home buyers on to the property ladder without having to shackle themselves to super-sized debts, the places in this scheme are set to be capped at just 10,000 per year, which is unlikely to be enough to cater for the potential demand,” she said.

Article Q&A

Who are the most active buyers of Australian property?

The value of new loan commitments for investors was rising higher than owner-occupier borrowers. Investment lending increased by 18 per cent to reach $9.72 billion while owner-occupier new loan commitments were up only 10.6 per cent over the year to reach $17.86 billion in loans. But it was first home buyer activity that stood out, with a 25.8 per cent increase in the value of new loan commitments for first-time buyers.

Which states have the most new loan activity?

ABS data shows new loan commitments in Queensland rose 3.3 per cent, Victoria rose 2.0 per cent, South Australia rose 6.9 per cent, in the Australian Capital Territory rose 9.4 per cent and in the Northern Territory rose 6.0 per cent while New South Wales fell 1.1 per cent, in Western Australia fell 2.9 per cent and Tasmania fell 15.2 per cent.

With housing affordability at its lowest level in three decades thanks to higher cost-of-living pressures, interest rate raises and healthy property prices, Perth’s property market is proving a standout.

Helen Avis, director of specialist mortgage at brokerage SMAT Services, said Perth was experiencing a massive boom generated by younger home buyers, with housing affordability better than it was in the late 2000s and early 2010s during the height of the mining investment boom.

Avis (pictured above left) said young home buyers had shown an increased interest in the property market during the pandemic.

“But post pandemic there has been a marked decline in first home buyers in Sydney and Melbourne, which we put down to affordability, rising interest rates and the difficulties of saving for a deposit.

“The opposite can be said about Brisbane and Perth, where there is still strong demand from the first home buyer market.”

Julie Kelley, sales and marketing manager at national real estate group aussieproperty.com, (pictured above centre) said across Australia there had been an increase in the number of first home buyers attending open homes with their parents, indicating the bank of mum and dad could be the key to entering the market.

East Coast Investors Buying Lower-Priced Perth Property

However, Kelley said Perth property in the lower price range, particularly in the outlying suburbs, was being snapped up by east coast investors.

“Unfortunately, this is resulting in first home buyers facing more competition for homes priced under $600,000 and they are being forced to broaden their search to the outskirt suburbs or consider buying smaller apartments and cottage homes,” Kelley said.

“The biggest increases in enquiries are from investors and buyers looking to upgrade their homes.

“There has been an enormous increase of interstate interest in Perth real estate particularly from Sydney and Melbourne.

“We have also seen a record night numbers of interstate migration and given Perth’s vacancy rate of 0.9% it’s difficult to secure rental properties, so many cashed up eastern states’ migrants are looking to purchase. “

Avis said many interstate buyers were guided by buyers’ advocates with limited local area knowledge or by big data, which could lead to poor long-term investment decisions.

“Off-the-plan developments hasn’t been popular for the past 12 months mainly due to the risk factors associated with the current state of the building and construction industry,” Avis said.

“Inner city suburbs and the western suburbs are still the most desirable locations for owner occupiers and investors, the north west coastal suburbs are also very popular.

“They are well established suburbs, close to the river and ocean, have excellent amenities, recreational facilities and public transport to the CBD and universities.”

A recent PropTrack Housing Affordability Index 2023 report highlights just how dire affordability is now particularly in NSW, Tasmania, and Victoria, with Perth the most affordable state in Australia.

“That is a marked change from a decade ago, when Western Australia was the least affordable state from 2007-2010 amid the height of the mining investment boom,” the report states.

“[This is] the only time any state has displaced NSW as the least-affordable state.”

Peter Gavalas, a buyer’s agent from Resolve Property Solutions, (pictured above right) cautioned that fierce buyer competition amid the booming Perth property market could see some buyers settle for low-quality properties that they might one day regret owning.

“The bottom line is that, right now, the Perth property market doesn’t have enough supply to cater to all the demand,” Gavalas said.

“So buyers are reacting the same way they do in any boom – they’re compromising on quality, by settling for less desirable homes, such as ones with structural problems, or less desirable locations, such as on noisy main roads, because they fear they’ll never enter the market any other way.”

Gavalas said even though buyers were experiencing FOMO, it was likely they would suffer a case of buyer’s remorse in the years ahead if they compromised on quality.

“A better option would be to buy a higher-quality property with stronger resale value in a cheaper neighbouring suburb,” Gavalas said.

In the complex world of real estate, purchasing a home or investment property is a significant financial decision. For most people, it’s one of the most substantial investments they’ll ever make. With so much at stake, it’s crucial to navigate the mortgage process with expertise and confidence. This is where a mortgage broker can be an invaluable ally.

A mortgage broker acts as an intermediary between borrowers and lenders, offering an array of services and benefits that can make your mortgage experience more manageable and rewarding. Let’s explore the advantages of engaging a mortgage broker, helping you understand why this is a smart choice for your next property purchase.

One of the primary benefits of working with a mortgage broker is tapping into their expertise and market knowledge. Mortgage brokers are trained professionals who stay up to date with the ever-evolving lending landscape. They have a deep understanding of the mortgage market, including various loan types, interest rates, and lender policies.

These professionals can offer valuable insights into the market conditions, helping you secure the best loan terms and conditions based on your unique financial situation and property goals.

When you walk into a bank, you’re limited to their specific loan products. However, mortgage brokers have an in-depth knowledge of the lending industry and an extensive network of contacts providing access to a vast network of lenders, including major banks, credit unions, private lenders, and non-traditional financial institutions. This extensive lender network provides borrowers with more options and greater flexibility when choosing a loan that suits their needs.

With a keen understanding of your financial situation and goals, mortgage brokers can leverage their expertise to find suitable loan options from various lenders. They can even tap into lenders that might not be easily accessible to the general public or have access to exclusive deals, promotions and interest rates.

Due to their established relationships with lenders, brokers can negotiate competitive rates and favourable terms on your behalf. It’s these exclusive deals and rates that you gain access to when you work with a broker. They can help you secure a loan with the best possible interest rate, potentially saving you thousands of dollars over the life of your mortgage.

Whether you’re a first-time buyer or an experienced investor, a mortgage broker can find the right loan for your needs. They will shop around on your behalf, finding the best loan product from a multitude of lenders, potentially saving you time and money.

Personalised And Simplified

One of the key advantages of working with a mortgage broker is the personalised service they provide. They take the time to understand your unique circumstances, financial goals, and preferences. They assess your financial situation, long term goals and preferences to tailor loan solutions that are most suitable for you. Instead of a one-size-fits-all option, brokers will provide tailored advice to match you with the right loan.

Based on this information, they can recommend loan options that align perfectly with your needs. Whether you’re a first-time buyer, a property investor, or a self-employed individual, brokers can assist in structuring loan terms, negotiating interest rates, and selecting features that best suit your situation. Their valuable advice can help you structure your loan for maximum benefit.

Don’t forget, mortgage applications can be time-consuming and complex, often requiring extensive paperwork and communication with lenders. A mortgage broker simplifies this process for you. They collect your financial documents, complete applications, and work closely with lenders, streamlining the application process.

Lenders have strict criteria for approving loans. What may seem like a straightforward application to you can be declined by a bank for various reasons. A mortgage broker, with their industry expertise, can increase your odds of loan approval.

Brokers understand each lender’s specific requirements and can match you with one that aligns with your financial situation. This increases your chances of securing the loan you need.

This not only saves you time and stress but also increases the chances of loan approval. Brokers are well-versed in lender requirements and can ensure your application meets all necessary criteria.

Negotiation is a crucial aspect of securing a favourable mortgage. Mortgage brokers are skilled negotiators who can haggle with lenders on your behalf to secure the best interest rates and loan terms. Their ability to negotiate can result in lower monthly payments and substantial long-term savings.

They can also leverage their relationships with lenders to gain more favourable terms for their clients.

Your mortgage broker will be by your side during the application and settlement process. They will act as a liaison between you, the lender, and other professionals involved, such as solicitors and real estate agents. This support ensures that all required documentation is submitted accurately and on time, contributing to the smooth progression of the mortgage application and settlement.

Less Stress, Less Fees

Purchasing a property is a significant life event, and it often comes with high levels of stress. A mortgage broker can alleviate this stress by handling the complexities of the mortgage process for you, all while keeping you informed.

The mortgage market can be overwhelming, with numerous loan products, features, and terminology. Mortgage brokers simplify this complexity by providing clear and concise comparisons of loan options. They’ll explain the fine print, terms, and conditions, ensuring you have a thorough understanding of each loan product’s benefits and limitations. This empowers you to make informed decisions that align with your financial goals.

Researching, comparing, and applying for mortgages can be a time-consuming and overwhelming process. Mortgage brokers can save you precious time by doing the legwork for you. They’ll research and compare loan options, prepare the necessary documentation, and submit applications on your behalf. This frees up your time, allowing you to focus on other aspects of your property purchase or your life in general. Finding and securing a mortgage can be a daunting task, so why not engage a professional to handle it for you?

A common misconception is that using a mortgage broker comes with hefty fees. In reality, many brokers don’t charge borrowers for their services. Instead, they are compensated by the lenders themselves, receiving a commission upon the successful placement of a loan.

While it’s essential to discuss fees with your broker, most borrowers find that the benefits of using a broker far outweigh any potential costs.

Mortgage brokers offer more than just loan recommendations. They provide comprehensive financial guidance and support throughout the mortgage process. Brokers can help you understand the costs associated with buying a property, assist in budgeting and financial planning, and advise on strategies to improve your borrowing capacity. Their expertise extends beyond mortgages, making them a valuable resource for overall financial well-being. Brokers continue to be a valuable resource throughout your loan term, offering guidance on repayment strategies, refinancing opportunities, and financial management. Their ongoing support ensures you make informed decisions about your mortgage, making your financial journey smoother and more successful.

By offloading these responsibilities to a mortgage broker, you can focus on other aspects of your property purchase, such as property selection and inspections.

From navigating legal documentation to ensuring your application adheres to lender requirements, brokers can save you from the errors that often arise when borrowers go it alone.

Their commitment to your financial well-being and their ability to secure the most favourable loan terms make them an indispensable ally on your journey to homeownership or investment property success.

Mortgage Broker Engagement Checklist:

Engaging a mortgage broker can significantly streamline the home loan process and offer a range of benefits. Before making a decision, consider the following checklist to ensure you fully understand the advantages of having a mortgage broker:

Lender Access

Understand the breadth of lenders the broker has access to.

Confirm if the broker works with a variety of institutions, including banks, credit unions, and non-bank lenders.

Personalised Service

Assess the broker’s commitment to understanding your unique financial situation and goals.

Ensure the broker tailors loan recommendations to your specific needs.

Time Savings

Evaluate how the broker streamlines the application and approval process.

Confirm if the broker handles research, documentation, and submission on your behalf.

Cost Efficiency

Understand the fee structure of the broker and how they are compensated.

Compare potential savings on interest rates and fees offered by the broker.

Exclusive Deals

Inquire about the broker’s ability to access exclusive deals and rates.

Understand how the broker’s relationships with lenders can benefit you.

Loan Comparison

Confirm the broker’s ability to provide clear and concise comparisons of loan options.

Ensure the broker explains terms, conditions, and the fine print.

Support During Settlement

Confirm the broker’s role during the application and settlement process.

Ensure they act as a liaison between you, the lender, and other professionals involved.

Understanding Loan Terms

Thoroughly review the loan terms presented by the broker.

Seek clarification on any terms, conditions, or provisions you find unclear.

Client Reviews and Testimonials

Look for client reviews and testimonials about the broker’s services.

Qualifications and Accreditation

Ensure the broker is qualified, licensed, and accredited.

Long-Term Relationship

Consider the potential for a long-term relationship with the broker.

Assess their commitment to assisting you in future financial endeavours.

By systematically evaluating these factors, you can make an informed decision about engaging a mortgage broker and reap the full benefits of their expertise in navigating the complex landscape of home loans.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

I pen down this note with great enthusiasm and a deep sense of gratitude for the recent acknowledgment that has brightened my professional journey – a nomination for the Mortgage Broker of the Year at the prestigious Women in Finance Awards 2023. The finance industry is vast, complex, and filled with incredible talent. It is an honour to be a part of such an esteemed community.

Being nominated alongside outstanding women in the finance sector was an experience that filled me with pride and humility. The calibre of nominees and winners alike showcased the remarkable achievements and contributions women are making in our industry. Congratulations to all the winners; your accomplishments are truly inspiring.

In the intricate tapestry of this industry, acknowledgment serves as a powerful catalyst for change. This nomination, aligned with the Women in Finance Awards, is a celebration of the resilience, innovation, and excellence that women bring to the forefront of mortgage brokerage. It’s a moment that resonates beyond individual recognition, embodying the collective prowess of women in the financial sphere.

This nomination is not just about me. It’s about inspiring others to dream big and break free from conventional moulds. Together, we’re building a community where women empower women, and success knows no gender.

Celebrating achievements is a must, whether or not they come with a trophy. The nomination itself is a win—a win for every woman striving to make a mark in finance. It’s a testament to the strides we’re making collectively, and it deserves its own spotlight.

So, let’s talk about the power of nomination. Being recognised in the Women in Finance Awards is more than a nod to my work; it’s a celebration of the collective strength of women in the mortgage world. It’s about breaking barriers, challenging stereotypes, and showing the world that we are forces to be reckoned with.

While the coveted trophy may not have found its way onto my shelf this time, the journey has been rich with invaluable lessons. The Women in Finance Awards go beyond recognising individual victories; they spotlight the collective power of women shaping the financial landscape. It’s about breaking barriers, fostering diversity, and creating a more inclusive future for all. I’ve grown both professionally and personally, learning more about the intricate dynamics of the mortgage industry and discovering new dimensions of my capabilities.

It has afforded me the opportunity to delve deeper into the complexities of the mortgage industry, fostering a continuous cycle of professional development. Lessons learned, challenges overcome – each distinction contributing to a more nuanced understanding of the financial landscape.

It’s a testament to the meritocratic strides that women are making in an industry traditionally dominated by gender norms. Recognition, in any form, is a pivotal step toward dismantling barriers.

As I reflect on this nomination chapter and the year itself as we glide even closer to the end of it, I find myself energised for the future. The nomination has reignited my commitment to excellence, and I eagerly anticipate the positive impact this will have on future endeavours, with a keen focus on elevating client experiences and industry standards.

This nomination is not just a recognition of past achievements; it’s a compass pointing toward future milestones. The journey continues, marked by excitement, continuous learning, and a resolute commitment to making a meaningful contribution to the realm of mortgage brokerage.

As we collectively strive for excellence, may this nomination serve as a beacon guiding us toward greater achievements and a more inclusive future for all in the finance sector.

So as the dust settles on this award winning year, I’m already setting my sights on new horizons. This journey has fuelled my passion for excellence, and I’m excited about the positive impact it will have on my future endeavours and the experiences I can create for my clients.

To that end, to every client, past and present I extend my sincere thanks. Your steadfast support is a testament to the collaborative spirit that drives our industry forward. I extend my heartfelt gratitude to my industry peers, and mentors who have been pillars of strength. Your unwavering support has been instrumental in propelling me forward, and for that, I am profoundly thankful.

To the winners, my heartfelt congratulations. Your accomplishments are well-deserved, and I applaud the excellence and innovation you bring to the finance sector. It’s both inspiring and motivating to witness the positive change you are driving.

The Women in Finance Awards have not only celebrated individual achievements but have also underscored the importance of diversity and inclusivity within our industry. So, here’s to breaking ground, shattering ceilings, and redefining success! Until next time, stay inspired and keep chasing those dreams.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.