At a time when the household saving to income ratio declined to its the lowest level in 16 years, new data has revealed that home ownership remains the biggest source of personal happiness.

In the pursuit of happiness, there’s a special kind that comes from owning your own Aussie home.

Recent research from Great Southern Bank has revealed that homeowners are happier than renters. There’s a unique sense of fulfilment that accompanies having a place to call your own, and it extends beyond mere bricks and mortar.

The Aussie Dream: More Than A Roof Over Your Head

According to the No Place Like Home report, 70 per cent per cent of respondents agreed that owning a home is an important factor in their happiness.

Half plan to buy a home to live in within the next three years. Half of renters are also hopeful of buying a home to live in within the next three years too.

What the research shows is there is still growing aspiration to own a home, with it not just being homebuyers that are looking. Forty-two per cent of existing homeowners are thinking of buying their next home – either upsizing, downsizing or making a lifestyle change.

Embarking on the journey to home ownership is more than a transaction – it’s a voyage toward a happier, more fulfilling life – and the research proves it.

Owning a home is not just about having a roof over your head. It’s about embracing a lifestyle that reflects the warmth of the Australian spirit.

Here’s What Makes Homeownership Down Under A key To Happiness:

Stability And Security

A home is a sanctuary, a place where you feel secure, and your roots are firmly planted. It’s a stable haven in a world that’s constantly changing.

Community Connection

Aussie neighbourhoods foster a strong sense of community. From barbecues in the backyard to conversations over the fence, owning a home brings you closer to a network of friends and neighbours.

Investment In The Future

Beyond immediate joy, homeownership is an investment in your future. It’s a cornerstone for building wealth, providing a sense of financial security for years to come.

Personalisation And Pride

Your home is a canvas for self-expression. The ability to personalise and transform your space brings a deep sense of pride and accomplishment.

Freedom To Flourish

With a home of your own, you have the freedom to create the life you desire. Whether it’s raising a family, starting a new chapter, or enjoying your golden years, home ownership paves the way for your unique journey.

More Than Just Bricks And Mortar

The report found most people (81 per cent) consider their home their ‘happy place’, and almost three quarters (72 per cent) believe home is wherever their family or loved ones are.

Just over half say having a home is about having a place to celebrate their culture and traditions.

Home ownership is a journey that can be difficult.

Australian Bureau of Statistics data released Wednesday (6 December), showed the household saving to income ratio declined from 2.8 to 1.1, the lowest level since December 2007.

Household saving declined due to a strong rise in income payable (+6.3 per cent), which experienced its highest growth through the year (+27.9 per cent) since September quarter 1977. Income taxes drove the rise, in the absence of the Low and Middle Income Tax Offset, which ceased over 2022-23.

Inflationary pressure led to increased nominal household consumption (+1.4%), as consumers faced higher prices for goods and services, further contributing to the decline in household saving.

“Gen Z and millennials tell us that saving a deposit is the key barrier to taking that first step towards buying a home,” Megan Keleher, Chief Customer Officer, Great Southern Bank, said.

“It’s clear, however, that Australian home owners do become happier over time, as they build the equity in their home.”

Happiness is at its highest for mortgage-free home owners and Baby Boomers, with 57 per cent in each group saying they are happy with their current housing situation, compared to just 29 per cent of long-term renters.

The report found that 51 per cent of renters are feeling heavily burdened by their financial commitments – significantly higher than 36 per cent of home owners.

Long-term renters are also more concerned about the cost of living (84 per cent) and housing affordability (80 per cent) compared to those who have purchased their own home (73 per cent and 62 per cent).

“Every individual’s home ownership journey and personal experience is different, but the report highlights that owning your own home does bring increased happiness for the vast majority of Australians,” Ms Keleher said.

Getting Those Keys

Navigating the path to home ownership may seem daunting, but with the right guide, it becomes a joyous adventure.

Award-winning mortgage broker Helen Avis, Director of Finance, Specialist Mortgage, said finding a team that can help with the pathway to home ownership was a fundamental part of the process.

Home ownership may appear a distant dream but there are finance experts who can help make it achievable.

Tailored financial solutions – Every home owner’s journey is unique. We work closely with you to understand your goals and customise financial solutions that align with your aspirations.

Exploring the mortgage terrain – The world of mortgages can be complex. We simplify the process, providing clarity on terms, interest rates, and the various options available to you.

Maximising your buying power – We leverage the team’s expertise to ensure you get the most out of your investment. From finding the right loan to securing favourable terms, we are committed to maximising your buying power.

Ongoing support – Whether you’re a first-time buyer or looking to expand your property portfolio, we provide ongoing support to ensure your financial goals are met.

Article Q&A

How do you get to buy your first home?

According to the No Place Like Home report, 70 per cent per cent of respondents agreed that owning a home is an important factor in their happiness. The path to that ownership is difficult but mortgage professionals can implement strategies to make it achievable.

Are household savings in decline or rising?

Household saving declined due to a strong rise in income payable (+6.3 per cent), which experienced its highest growth through the year (+27.9 per cent) since September quarter 1977. Income taxes drove the rise, in the absence of the Low and Middle Income Tax Offset, which ceased over 2022-23.

In the pursuit of happiness, there’s a special kind that comes from owning your own Aussie home. As a Mortgage Broker with a passion for making dreams come true, I find immense joy in helping people embark on this journey of homeownership.

Recent research from Great Southern Bank echoes what I witness every day – homeowners are, indeed, happier than renters. There’s a unique sense of fulfillment that accompanies having a place to call your own, and it extends beyond mere bricks and mortar.

The Aussie Dream: More Than a Roof Over Your Head

According to the No Place like Home report, 70% of respondents agreed, that owning a home is an important factor to their happiness. Despite interest rates increasing and the state of the world for, let’s face it – the last three years… the report’s research still shows optimism amongst Australians wanting to purchase a home with one in two Aussies planning to buy a home to live in within the next 3 years. One in two renters are also hopeful of buying a home to live in within the next 3 years too.

What the research shows is there is still growing aspiration to own a home, with it not just being homebuyers that are looking, but 42% of existing homeowners are thinking of buying their next home – either upsizing, downsizing or making a lifestyle change.

Embarking on the journey to homeownership is more than a transaction – it’s a voyage toward a happier, more fulfilling life – the research proves it!

Owning a home in this sun-kissed land is not just about having a roof over your head. It’s about embracing a lifestyle that reflects the warmth of the Australian spirit.

Here’s What Makes Homeownership Down Under A Key To Happiness:

Stability and Security

A home is a sanctuary, a place where you feel secure, and your roots are firmly planted. It’s a stable haven in a world that’s constantly changing.

Community Connection

Aussie neighbourhoods foster a strong sense of community. From barbecues in the backyard to conversations over the fence, owning a home brings you closer to a network of friends and neighbours.

Investment in the Future

Beyond immediate joy, homeownership is an investment in your future. It’s a cornerstone for building wealth, providing a sense of financial security for years to come.

Personalisation and Pride

Your home is a canvas for self-expression. The ability to personalise and transform your space brings a deep sense of pride and accomplishment.

Freedom to Flourish

With a home of your own, you have the freedom to create the life you desire. Whether it’s raising a family, starting a new chapter, or enjoying your golden years, homeownership paves the way for your unique journey.

More than just bricks and mortar

The report found most people (81%) consider their home their ‘happy place’, and almost three quarters (72%) believe home is wherever their family or loved ones are. Just over half say having a home is about having a place to celebrate their culture and traditions.

“Home ownership is a journey and we acknowledge that it can be difficult. These results show it is worth the trade-offs people make along the way. Gen Z and millennials tell us that saving a deposit is the key barrier to taking that first step towards buying a home. It’s clear however that Australian homeowners do become happier over time, as they build the equity in their home.” Megan Keleher, Chief Customer Officer, Great Southern Bank.

Happiness is at its highest for mortgage-free homeowners and Baby Boomers, with 57% in each group saying they are happy with their current housing situation, compared to just 29% of long-term renters.

The report found that 51% of renters are feeling heavily burdened by their financial commitments – significantly higher than 36% of homeowners. Long-term renters are also more concerned about the cost of living (84%) and housing affordability (80%) compared to those who have purchased their own home (73% and 62%).

“Every individual’s homeownership journey and personal experience is different, but the report highlights that owning your own home does bring increased happiness for the vast majority of Australians,” Ms Keleher said.

Let’s get those keys!

Navigating the path to homeownership may seem daunting, but with the right guide, it becomes a joyous adventure.

Here’s How Specialist Mortgage Can Help:

Tailored Financial Solutions – Every homeowner’s journey is unique. We work closely with you to understand your goals and customise financial solutions that align with your aspirations.

Exploring the Mortgage Terrain – The world of mortgages can be complex. We simplify the process, providing clarity on terms, interest rates, and the various options available to you.

Maximising Your Buying Power – We leverage the team’s expertise to ensure you get the most out of your investment. From finding the right loan to securing favourable terms, we are committed to maximising your buying power.

Ongoing Support – Beyond the transaction, we are here for the long haul. Whether you’re a first-time buyer or looking to expand your property portfolio, we provide ongoing support to ensure your financial goals are met.

We can assist you every step of the way, from navigating the homebuying process, to understanding loan options and getting the mortgage that suits your needs. Let’s unlock the doors to your dream home together.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

Property prices in Perth are defying a gradual easing in the rate of capital growth being seen elsewhere in the nation and dominating lists of the nation’s hottest real estate markets.

If you bought property anywhere in Australia other than Perth, then your home is not among the 10 fastest rising markets in the country.

All 10 suburbs where prices have risen the fastest in 2024 are in the West Australian capital, and one affordable part of the city has dominated within that list.

The working class City of Kwinana stands atop the national podium, with its suburbs of Medina, Parmelia and Orelia the three fastest growing property markets in the nation and Calista coming in sixth overall.

Top 10 fastest rising property markets for 2024

All of the suburbs in the PropTrack top 10 were relatively affordable places to buy.

South Australia came closest to competing with Perth for price growth in 2024 to date, with top ranked Elizabeth Park having house price growth of 17.1 per cent, still 6 per cent below Perth’s tenth placed Coolbellup.

With the exception of SA’s sixth placed West Lakes’ median house price of $1,074,000, eight of the other nine had even more affordable values than Perth’s top 10, being under $550,000.

Highlighting Melbourne’s stable but subdued property market throughout 2024, the top ten suburbs delivered capital growth between 6.7 per cent (Rutherglen) and 3.6 per cent (Kyabram).

CoreLogic’s daily home value index has seen a marked easing in the rolling four week change, with national values rising just 0.5 per cent over the four weeks to 18 July, down from a 0.7 per cent rise seen the same time last month.

The recent slowdown is notably stronger across more expensive markets and property types with house values and values in Sydney recording the most noticeable easing.

Melbourne and Hobart are the only capitals recording falling values, with high stock levels placing downside pressure on values.

Perth continues to lead the pack, with a rolling 28-day increase of 1.8 per cent, followed by Adelaide (1.7 per cent) and Brisbane (1.0 per cent). The trend for softer growth is less apparent in these cities.

Perth is the property story of 2024

But the real story of capital growth in Australia at the moment belongs to one boom city.

The median Perth house sale price set a new record month after month over the financial year, and is now $665,000 for the year to June 2024. This is 18.8 per cent higher than at the end of the 2022-23 financial year.

The median unit sale price increased 11.3 per cent year-on-year to reach $445,000, according to REIWA, just $5,000 below the previous record of $450,000 in 2014.

REIWA CEO Cath Hart said she expects this record to be broken in the next few months.

Viveash, which recorded the highest price growth for houses, had its median house sale price increase 40.9 per cent over 2023-24 to $620,000, highlighting the rush to mid and lower priced property.

“Affordability remains a focus for buyers and this is reflected in the makeup of the financial year’s top 10 suburbs for house price growth,” Ms Hart said.

“The majority have a median sale price below Perth’s median and only two have a median house sale price over $1million.

“It indicates strong demand for suburbs in more affordable price brackets.

“Demand is also reflected in their selling times, with the more affordable suburbs on the list having a median time on market that is nearly half that of the suburbs with a median over $1 million.”

In the unit market, Cottesloe was the top performer, with its median sale price rising 50.9 per cent to $1,200,000. Bayswater recorded growth of more than 40 per cent.

Like the top 10 list for house price growth, seven of the suburbs in the top 10 for units have a median sale price under Perth’s median unit price.

“While the unit market was slower to respond to market conditions over most of 2023, in 2024 we have seen demand and price growth accelerate,” Ms Hart said.

“The overall demand for property, and particularly the strong motivation to exit the challenging rental market, has seen demand for units increase. Units are generally more affordable than houses, which helps people put a foot on the property ladder in a rising market. This is helping drive price growth in the unit market.”

This financial year saw houses sell incredibly quickly, with a new monthly record of a median eight days on market set in October and November.

Which suburbs have the fastest rising property prices in Australia so far in 2024?

All 10 suburbs where prices have risen the fastest in 2024 are in the West Australian capital, and one affordable part of the city has dominated within that list. The working class City of Kwinana stands atop the national podium, with its suburbs of Medina, Parmelia and Orelia the three fastest growing property markets in the nation and Calista coming in sixth overall.

How fast are properties selling in Perth?

The 2023/24 financial year saw houses sell incredibly quickly, with a new monthly record of a median eight days on market set in October and November 2023.

Where are unit prices rising fastest in Perth?

In the unit market, Cottesloe was the top performer, with its median sale price rising 50.9 per cent to $1,200,000. Bayswater recorded growth of more than 40 per cent. Seven of the suburbs in the top 10 for units have a median sale price under Perth’s median unit price.

Our Top tips to slash that mortgage in 2024

From cutting years off the length of a mortgage to maximising rental income, these seven tips highlight how there is much more to a good property manager than collecting rent and doing property inspections.

If you’re one of the 2.2 million Australians who own an investment property, cash flow is the priority.

With an estimated 80 per cent of Australian property investors employing the services of a professional property manager, your property manager should be one of the key professionals who help improve your cash flow.

While most property investors look to their accountant to help improve the cash flow of their investment property, they often forget the value a professional property manager can bring to a property’s cash flow.

Here are seven strategies your property manager can implement to improve your cash flow:

1. Optimise rent disbursement frequency

Consider the benefits of more frequent rent disbursements.

While monthly payments are common with most property managers, switching to weekly disbursements can save you on interest costs, if you match your mortgage repayments accordingly.

For example: If you consider a loan amount of $500,000, with an interest rate of 6.6 per cent, paying principal and interest on a 30-year loan term, the savings can become obvious.

Swapping from monthly mortgage payments of $3213 to weekly mortgage payments of $803, the interest savings over the 30 years could be up to $163,730 (or reducing the loan term by six years, five months).

By aligning rent disbursements with your mortgage repayment schedule, you can effectively reduce interest expenses and improve your cash flow.

2. Maximise rental income

By staying informed about market trends and conducting regular rent reviews, property managers can ensure income is not left on the table.

Many places haves generated weekly rent increases of up to $200, highlighting the potential for significant income growth.

Property managers will, of course, be bound by any state’s legislation regarding rent increases.

3. Minimise vacancy periods

Vacant periods can have a significant impact on cash flow.

A property manager should manage lease renewals and minimise downtime between tenancies.

Furthermore, your property manager can implement targeted marketing campaigns and utilise online platforms to attract prospective tenants quickly, reducing vacancy periods and optimising your cash flow.

4. Reimbursing water consumption charge

Ensure that all allowable water consumption charges are passed on to tenants.

Whether your property is new or old, your property manager can implement systems to accurately track and bill tenants for water usage, helping to offset your expenses.

In some areas, strata title properties don’t issue individual property consumption information, and this can impact your ability to seek reimbursement of water consumption from your tenants.

5. Fair pricing from tradespeople

Qualified tradespeople are essential for maintaining your property, but their costs can vary.

Your property manager can leverage their network of trusted professionals to ensure fair pricing for maintenance and repairs, preventing overcharging and minimising expenses.

Additionally, your property manager can obtain multiple quotes for larger projects and negotiate favourable rates on your behalf, ensuring cost-effective maintenance solutions without compromising on quality.

6. Implement preventative maintenance programs

Proactive maintenance can prevent small issues from escalating into costly repairs.

By scheduling regular inspections and addressing maintenance issues promptly, your property manager can help you avoid unexpected expenses and preserve your property’s value.

Additionally, a property manager can develop customised maintenance schedules tailored to your property’s specific needs, addressing potential issues before they impact tenant satisfaction and annual rental yield.

7. Manage insurance claims efficiently

In the event of an insurance claim, your property manager should be experienced in managing these claims, which can facilitate a swift resolution.

Their expertise in property management and established relationships with insurers and local tradespeople can expedite the claims process, ensuring minimal disruption to cash flow.

Your property manager can document and report property damage promptly, liaise with insurance adjusters on your behalf, and oversee repairs to ensure timely completion and reimbursement. By efficiently managing insurance claims, your property manager can safeguard your investment and maintain uninterrupted cash flow.

Article Q&A

Should I use a property manager for my investment property?

A property manager can help optimise rental income, minimise expenses and ensure a steady stream of revenue, even slashing years off the duration of a mortgage by optimising rent disbursement frequency.

Now is the time to buy Australian property. Here are tips to help you maximise your returns.

If you’ve been contemplating the idea of investing in Australian property, you’ve likely encountered the question: “When is the best time to buy?” That’s often met a wink and a nod followed by with the reply, “NOW!” But before you jump in feet first, let’s dive into some of the intricacies to consider.

Start With Tax Advice

First and foremost, let’s talk taxes. In the realm of property investment, understanding tax implications is crucial. Australia offers a range of tax benefits designed to support property investors. It’s important to be well informed about buying structures, negative gearing, capital gains tax, and to have a robust property investment strategy.

It’s also essential to remember that tax laws can be complex and subject to change. Seeking advice from a tax professional who specialises in property investments and expatriate taxation is key to ensuring that you’re maximising your tax advantages.

As a leading provider of Australian taxation, finance, and property services to Australian expatriates and foreign investors, SMATS Group has assisted thousands of clients to purchase property using tax effective and reduced risk investment strategies that are geared towards long-term success.

“Property Values Often Climb Faster Than Our Budget”

Navigating Home Loans

As any experienced investor will tell you, securing mortgage pre-approval is pivotal. Unfortunately, when you’re an expat or non-resident buyer, you’re often faced with decreased mortgage options, reduced borrowing capacity and higher rates. However, this doesn’t always have to be the case.

This is where partnering with a firm that has been successfully obtaining home loans for Aussie expats and non-residents for over 30 years is a no-brainer. Specialist Mortgage, the finance division of SMATS Group, has mastered the art of tailored expat mortgage solutions.

Mortgage pre-approval not only gives you a clear understanding of your borrowing capacity, but it establishes your credibility as a serious buyer. It can save you time, energy, and heartache by streamlining the process when you find the perfect property. In addition, pre-approval can provide you with the confidence of shopping with a budget in mind.

Buying The Aussie Dream

The physical distance, local market knowledge gap, and dealing with real estate agents can make buying Australian property whilst abroad seem like an insurmountable task. That’s where a buyer’s agent can assist.

A buyer’s agent can serve as your local eyes and ears, advocate for your interests, and leverage their expertise to find your ideal property. Navigating negotiations, conducting property inspections, and handling legal intricacies – all of these are simpler when you have a trusted professional by your side. At SMATS Group, our buyer’s agents possess an in-depth understanding of the Australian market, including emerging trends and hidden gems that you might miss from afar.

And here’s why they will tell you, NOW is the time to buy Australian property. The market has displayed remarkable resilience through various economic shifts, reinforcing its reputation as a stable and attractive investment option.

Cities like Sydney, Melbourne, Brisbane, and Perth continue to be strong contenders for property investment due to their economic growth, cultural vibrancy, and desirability. Recent data indicates that property prices are on the rise driven by factors such as buyer competition, housing demand, supply shortages and migration.

Ditch Procrastination

Many of us will reflect on our home buying journey and think “I wish I’d bought 10 years ago”. Procrastination often results in us having to downgrade from our dream home. Property values often climb faster than our budget. That once attainable property grows out of reach.

The lesson learned is that waiting doesn’t achieve results. Buying your home today means you lock in today’s price. When, it comes to buying quality Australian real estate, the sooner the better. Quality liveable real estate will always be in high demand, ride the wave of property cycles, and outperform the market.

If you’re an expat or a non-resident, the path might seem more challenging, but rest assured, solutions are within reach. SMATS Group can assess your unique circumstances and guide you through the maze of mortgages and intricacies of purchasing whilst abroad, whether that be your ideal home or an investment property.

With a blend of favourable conditions, professional guidance, and a landscape that beckons, this might just be your moment to make your mark on the Australian property market.

In just three years, the time it takes the average first home buyer to save a house deposit has leapt by almost 3.5 years in New South Wales, more than two years in Victoria and nearly a year-and-a-half in Queensland.

If you’re an aspiring first home buyer in Sydney, expect to spend the next eight years of your life saving for a deposit.

That’s the time it takes to cobble together enough coin to put down the median deposit of $145,000.

The situation is a little better, but also worsening rapidly, in Melbourne and Brisbane, where a 25-year-old will be in their 30s by the time they’ve saved enough money to pay a house deposit.

Buyers in Melbourne are estimated to take 65 months, or nearly 5.5 years, to save for the current median deposit, with buyers in Brisbane estimated to take 60 months or five years.

The latest figures from PEXA have revealed a huge leap in the deposit-saving timeframe from just a few years ago.

Notes – (2) Based on a 15% savings rate, see page-18 for details on our approach; (3) Queensland comparison based on two-year period Sep-21 Qtr to Sep-23 Qtr (Source PEXA)

Regional buyers were expected to take less time to save for a deposit due to the lower median deposit amounts in regional areas. Buyers in regional NSW were estimated to take 63 months (over 5 years), with regional Queensland 59 months (just under five years) and Victoria at 49 months (just over four years).

For young people who might want to enjoy a drink on the weekend with friends, the findings of the PEXA Buyers Deposits Report, released Wednesday (29 November) make for sobering reading.

No young buyers will be popping champagne corks over the added finding that more than half of new borrowers required lenders mortgage insurance (LMI) in financial year 2023 (FY23), even if those proportions have dropped slightly in each state.

This was highest in Victoria, with 56.5 per cent of new borrowers obligated to take out LMI.

Due to the higher average loan-to-value ratios (LVRs) of major banks, a greater proportion of their customers required LMI. This was most evident in Victoria with 63.9 per cent of major bank customers having an LVR higher than 80 per cent.

Average LVRs for new loans across the eastern states hovered around 80 per cent. NSW was just below at 79.6 per cent in FY23, with Victoria and Queensland just above at 80.5 and 80.2 per cent respectively. All states had seen average LVRs decline since FY22, with Queensland down the most, dropping 1.5 per cent.

The news for first home buyers – whether on a beer or champagne property budget – has only been made worse by a sharp rise in mortgage rates and rising property values over the past few years that have driven housing affordability to its worst level in three decades.

Notes – (1) Compared to FY22; (2) LMI generally required for loans with an LVR > 80% (Source: PEXA)

The PropTrack Housing Affordability Index 2023 found that first home buyers are the most impacted, however, even high-income households are feeling the pinch. This is particularly evident in New South Wales, Tasmania, and Victoria.

The report showed an average 25–34 year-olds’ household could afford fewer than 30 per cent of the houses sold in 2022-23 and concluded that saving a deposit remains the biggest barrier for first home buyers.

Julie Kelley, Global Sales and Marketing Manager for aussieproperty.com, said they had experienced a huge surge of first home buyers entering the market during the pandemic but that it was now in reverse.

“Low interest rates, government grants and incentives, and in the case of Western Australia an off-the-plan rebate, had attracted first home buyers to make the leap into home ownership,” Ms Kelley said.

“But post-pandemic we have experienced a marked decline of first home buyers in Sydney and Melbourne, which we put down to affordability, rising interest rates and the difficulties of saving for a deposit.

“The opposite can be said about Brisbane, even if it is taking longer to save for a deposit, and Perth, where there is still strong demand in each from the first home buyer market.”

Ms Kelley said Perth is experiencing a massive boom among younger home buyers, where housing affordability is better than it was in the late 2000s and early 2010s during the height of the mining investment boom.

“Perth property in the lower price range, particularly the outlying suburbs, is being snapped up by east coast investors.

“With limited housing availability under $600,000 and increased competition by investors and new migrants, we are noticing the competition is frustrating first home buyers and they are being forced towards the outskirt suburbs or into smaller apartments and cottage homes.”

Median deposit amounts in capital cities were significantly higher than regional areas. (source: PEXA)

The PEXA report showed that the median deposit amount in New South Wales increased from just over $73,000 in the September 2020 quarter to nearly $135,000 in corresponding 2023 quarter, with other eastern states recording similar rises.

As a result, it noted many first home buyers resorted to parental financial support to overcome the deposit hurdle.

“Nationwide, we are seeing an increase of first home buyers attending home opens with their parents, indicating the bank of mum and dad may be their key to entering the market,” Ms Kelley said.

New Scheme To Help With Deposit Challenge

A new government scheme, with legislation to be introduced this week, will provide 40,000 eligible low and middle income home buyers the opportunity to acquire a home with a deposit of just 2 per cent.

The Help to Buy scheme intends to support eligible home buyers with an equity contribution from the Government of up to 40 per cent for new homes and 30 per cent for existing homes. Buyers will have lower ongoing repayments while they take part in it.

The government hopes to have the scheme operational from 2024, although each state will need to pass their own legislation in order for the program to operate in their jurisdiction.

As they are subject to Commonwealth, not state, legislation, it will start in the Northern Territory and ACT first, following passage of the bill.

Jocelyn Martin, Managing Director, Housing Industry Association, said the legislation encouraging more young Australians to access housing would help address the declining rates of home ownership in Australia.

“These and other forms of housing incentive programs are critical to boost housing supply and home ownership rates to support first home buyers raising the deposit more quickly and easily.

“We know from previous schemes, such as the first Home Buyer Grant, that grants such as Help to Buy, are effective at getting people into their own home, and new housing supply is stimulated by these schemes,” Ms Martin said.

First home buyers in Queensland are eligible for an additional $15,000 after the state government doubled its First Home Owner Grant last week.

Article Q&A

How long does it take to save for a house deposit in Australia?

If you’re an aspiring first home buyer in Sydney, expect to spend the next eight years of your life saving for a deposit. Buyers in Melbourne are estimated to take 65 months, or nearly 5.5 years, to save for the current median deposit, with buyers in Brisbane estimated to take 60 months or five years.

What proportion of first home buyers require lenders mortgage insurance (LMI)?

More than half of new borrowers required lenders mortgage insurance (LMI) in financial year 2023 (FY23), with the the highest proportion in Victoria, with 56.5 per cent of new borrowers obligated to take out LMI.

What is the Help to Buy Scheme?

The Help to Buy federal government scheme will provide 40,000 eligible low and middle income home buyers in Australia the opportunity to acquire a home with a deposit of just 2 per cent. It intends to support eligible home buyers with an equity contribution from the Government of up to 40 per cent for new homes and 30 per cent for existing homes.

In the dynamic realm of finance, attending industry conferences is not just an option; it’s a strategic move towards growth, innovation, and personal and professional development. This sentiment was vividly echoed at the recent SFG National Conference and Awards in the tropical paradise of Port Douglas.

So Why Have Industry Conferences? Do They Matter?

As industry leaders, our commitment to excellence extends beyond our daily operations. It involves staying abreast of industry trends, fostering innovation, and building a team that thrives on knowledge and inspiration. Industry conferences like the SFG National event offer a rich tapestry of experiences, from captivating speakers to engaging panel sessions and unique team-building activities.

Last weekend I had the absolute pleasure of inviting my team to come along to the SFG National Conference and awards presentation in Port Douglas and it really did not disappoint. It kicked off with a bang on Day 1, immersing attendees in mind-bending experiences with Anthony Laye’s mind reading and Bastien Treptel’s IT hacking skills. The inspirational keynote by explorer Justin Jones set the tone for a conference focused on pushing boundaries. The day concluded with a Lender Panel Session that deepened our industry insights, followed by a laid-back Tropical beach BBQ—a stellar start to an industry event!

Day 2 commenced with sunrise reflections on Four Mile Beach, setting the stage for profound insights. Australian racing legend Craig Lowndes shared his success journey, complemented by sessions with young trailblazers and industry leaders. Award-winning Engagement & Thought Leader, Dan Gregory, enriched our perspectives on connected purpose and creativity. The day culminated with anticipation for the SFG National Awards.

An Absolute Triumph! – Celebrating Success & Camaraderie

Under the starlit skies of Port Douglas, the SFG National Awards unfolded on Day 3. The moment of pride arrived as I’m very humbled to report on receiving the coveted WA Broker of the Year award. A testament to a year marked by dedication, expertise, and outstanding achievements. The awards ceremony was a fitting conclusion to an eventful year and a prelude to the exciting prospects of 2024.

To cap off the celebration, attendees relished the SFG High Achievers Event, a blend of sophistication and relaxation. A visit to the Devil Thumbs Distillery and the Trinity Beach Palace set the stage for a delightful long-table lunch, marked by laughter, camaraderie, and shared successes. It was a day of acknowledgment, not just for individual achievements but for the collective triumphs of the finance & mortgage community on what has been a tumultuous year.

In closing, a heartfelt thank you to the entire SFG Team for orchestrating a weekend of learning, recognition, and celebration. As we raise a toast to 2024, we carry with us the lessons learned, the bonds forged, and the inspiration gained from the SFG National Conference and Awards—a pivotal milestone in our journey toward continued success. Cheers to a year of growth, collaboration, and prosperity!

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

Specialist Mortgage, a leading name in the mortgage broking industry, continues to make waves not only for its exceptional financial services but also for its dedication to diversity.

In a field where women brokers represent less than 25 per cent of employees, Specialist Mortgage stands as a shining example of gender diversity and excellence.

Having long been a leader in the field of expatriate and non-resident finance, a niche area that demands expertise, understanding, and a global perspective, Helen Avis, Director of Finance, and her team at Specialist Mortgage have consistently delivered tailored financial solutions, addressing the unique needs of clients residing both in Australia and overseas.

The Women in Finance Awards 2023 are a testament to the achievements and contributions of women professionals in the financial sector. In an industry where gender balance is still an evolving concept, her recognition as a finalist reaffirms Specialist Mortgage’s commitment to diversity and inclusion.

Ms Avis expressed her gratitude for the nomination, said she was privileged to be seen as a finalist in this year’s awards, especially in an industry where less than one in every four brokers are women according to a recent survey by the Mortgage and Finance Association of Australia.

“There are barriers to entry in every industry, but to be recognised as a bit of trail blazer in the industry that I really am so passionate about was one of those moments where it feels everything I’ve done up until now has been worth it.”

A veteran of the mortgage brokerage field with more than two decades of experience, Ms Avis has been named a finalist in the Mortgage Broker of the Year category. The announcement was made earlier this week, recognising her outstanding contributions and positive impact on the mortgage brokerage sector.

“Being in this industry for this long has allowed me to witness and adapt to the ever-changing landscape of finance,” she said.

“These nominations motivate us to continually raise the bar in providing tailored solutions for our clients.”

Specialist Mortgage continues to distinguish itself by maintaining a strong track record of assisting clients with expatriate and non-resident financing. Their dedication to excellence, coupled with their global reach, has made them a trusted name in the finance industry.

The winners of the 2023 Women in Finance Awards will be announced at a prestigious ceremony on Friday, 10 November 2023 at The Star in Sydney, where industry leaders and professionals will come together to celebrate the achievements of outstanding women in finance.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

Mortgage brokers are an intrinsic component in any real estate investment strategy, says award-winning finance expert from Specialist Mortgage, Helen Avis.

In the dynamic world of property investment, making informed financial decisions is crucial for long-term success.

As a seasoned property investor, there is an intricate web of factors that influence investment outcomes.

One of the key players in this realm is mortgage broker.

Their expertise can be an invaluable resource for any property venture, whether it’s a first home, investment property, or overseas purchase.

Helen Avis, Director of Finance, Specialist Mortgage, who has recently been recognised as a finalist in multiple categories of the Specialist Finance Group (SFG) National Awards, said an award-winning mortgage broker brings a wealth of knowledge that extends beyond the transactional aspect.

Why Engage An Award-Winning Mortgage Broker?

Tailored Solutions

A mortgage broker’s expertise lies in understanding the nuances of an investment strategy.

A personalised approach can ensure buyers’ financial needs are met with more precision than if left to an enthusiastic but unqualified investor.

Market Insights

As a property investor, staying ahead of market trends is crucial.

An award-winning broker will be well-versed in the shifting dynamics of the property landscape, offering insights that can positively influence investment decisions.

Optimised Financing

The ability to secure competitive financing options is a fundamental part of the broker’s role.

By assessing each unique financial circumstance and investment goal, a mortgage broker can guide clients towards loan structures that align with their long-term objectives.

Navigating Complexity

Property investment often involves intricate financial arrangements and regulatory considerations. A mortgage broker’s expertise can help in navigating the complexities of financing and ensuring compliance.

Overseas Property Purchases

Investing in Australian property from overseas adds a whole new layer of bureaucracy and financial complexity. Mortgage brokers with specific experience in this field, with experience working with expatriates and foreign buyers, will simplify the process significantly.

Holistic Approach

A mortgage broker’s role extends beyond securing loans. It takes into account an entire financial portfolio, aligning mortgage decisions with a client’s broader financial strategy.

“Whether you’re expanding your property portfolio, exploring your first investment, or navigating cross border transactions, an award-winning broker can be your compass in the dynamic world of property investment.”

– Helen Avis, Director of Finance, Specialist Mortgage

This year’s SFG National Awards will be held on 16 November.

While the pause in interest rates has come as a relief to many, everyone from first home buyers to owner occupiers and seasoned investors faces the prospect of harder times before they get easier.

There is a palpable sense of relief among borrowers that interest rates have been paused for a few months and may even be on their way down in the not-too-distant future.

But the reality is that many Australians are feeling the mental, physical and financial strain of a dozen rate hikes since May last year and are struggling to cope with the markedly higher mortgage repayments.

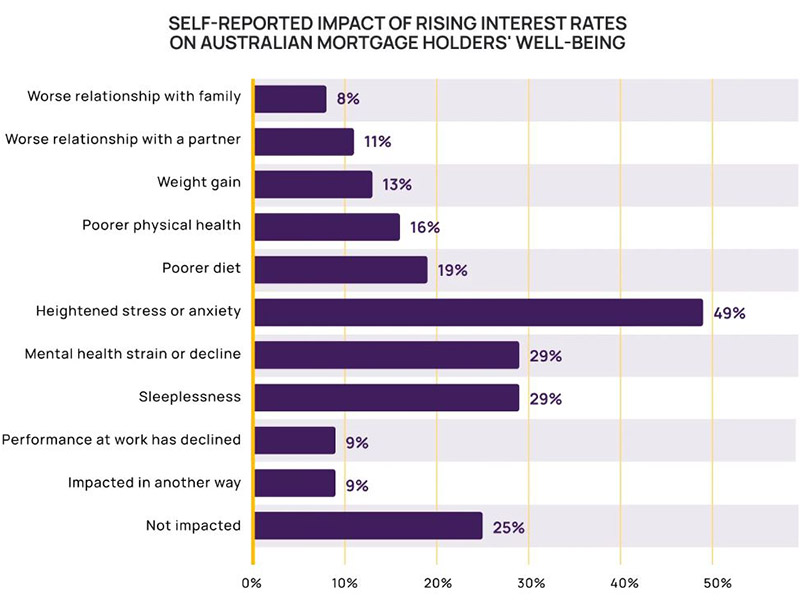

Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

That same 75 per cent said they would not trust any Reserve Bank of Australia (RBA) interest rates forecasts again.

With mortgage interest now averaging around 6.5 per cent, the reign of interest rate hikes means households with a $500,000 mortgage on a variable rate have seen their repayments increase by $1,500 per month in the midst of a cost-of-living crisis as their incomes are eaten away by high inflation.

Source: MNY.

Compounding the situation for those struggling is the argument that interest rates will likely rise, at least once more, before the tide turns and they begin to retreat.

Inflation is on a downward trajectory, which should bring rates down with it, but there some leading indicators that the battle against inflation may not be over.

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates.

“In the short term, the risks are still skewed to a further increase in interest rates and or a delay in the start of rate cuts as: inflation is still too high; the labour market remains tight with upwards risks to wages flowing from higher minimum and award wage rises; productivity growth is very weak; and the rebound in home prices is partly offsetting the tightening impact of higher interest rates.

“Consistent with this, the RBA retained its guidance that some further rate hikes may be required.

“Key to watch will be the global economy, household spending, inflation and the labour market.”

Mortgage Stress Rampant

While the RBA has consistently stressed that Australians are well placed to manage higher interest rates after accumulating savings during Covid and paying down debt ahead of time.

But researchers are also revealing that mortgage stress is rampant.

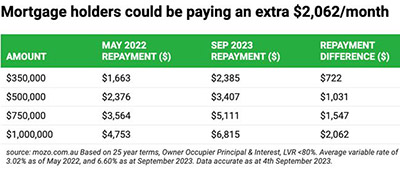

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm.

The average variable rate of an owner occupier home loan is now 6.60 per cent across all lenders, and 7.21 per cent across the Big Four banks.

Based on the average variable rate of 6.6 per cent, since May 2022 monthly repayments on a $500,000 home loan have increased by $1,031.

In a market where one in three borrowers think refinancing is too much of a hassle, Helen Avis, Director of Finance at Specialist Mortgage, said it was imperative those with stretched finances sought financial advice and better deals.

“The refinancing process may seem time-consuming but the savings on offer make it worthwhile and the application process these days is not as onerous as people may actually think.”

The incentive to refinance is also backed up by research from RateCity.com.au that reveals more than a quarter of Australians (27 per cent) are living payday to payday.

It found one third (33 per cent) of respondents were feeling stressed or uneasy about their budget, while 32 per cent couldn’t survive off their savings for more than a month if they were to lose their job.

Financial strain doesn’t just hit the hip pocket. The survey also found of those in a relationship, over a third (39 per cent) said cost of living concerns have caused increased friction with their partner about money.

First Home Buyers Facing Major Hurdles

First home buyers are being kept out the property market, often as a result of policies that had been intended to help them.

University researchers enlisted by the Australian Housing and Urban Research Institute (AHURI) found that the path to buying a first home is increasingly reliant on parental resources.

Professor Stephen Whelan, University of Sydney, said the issues confronting first home buyers were more complex than just higher property prices.

“While high and rising house prices are often cited as the biggest challenge faced by first homebuyers, our inquiry highlights that the problem is significantly more complex,” Professor Whelan said.

“Critically, we found existing policy settings are likely to have exacerbated rather than alleviated the challenge faced by first homebuyers to finance home ownership.

“Politically seductive measures such as first homeowner grants and tax concessions have failed to arrest declining rates of home ownership over time.”

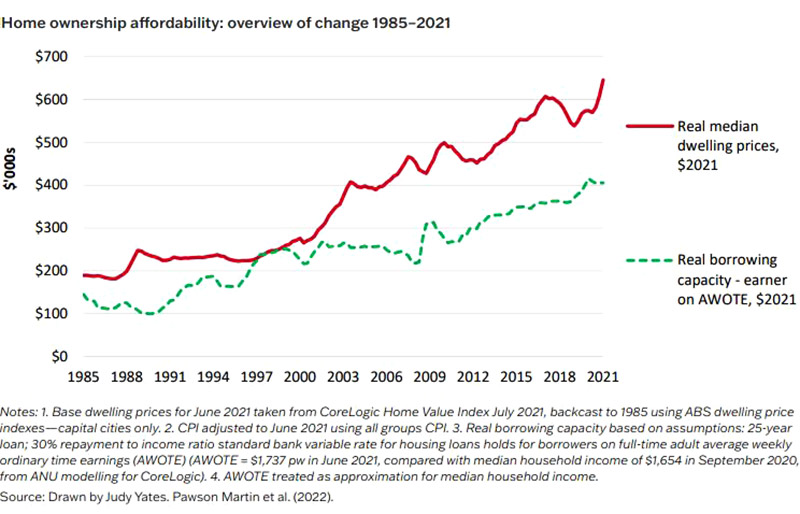

A rapid expansion of owner-occupation in the early postwar period peaked at over 70 per cent in the late 1960s but was followed by a gradually declining home-ownership rate since 2000—especially among younger adults, where the rate for the 25–34 age cohort fell from 51 per cent in 2001 to 44 per cent in 2021.

There is evidence that housing affordability has decreased over time.

AHURI’s research showed that since 2001, the national ratio of median house price to median income has almost doubled to 8.5, and the time required for the accumulation of a deposit for a typical property has increased from six years median earnings in 1994 to 14 years today.

The decline in home ownership among younger adult cohorts has occurred despite expenditures in excess of $37 billion over five decades designed to enable first home ownership.

AHURI’s findings stated that policies designed to assist first home buyers must recognise and address structural issues associated with the treatment of housing in the tax and transfer system.

“Policy settings need to encompass intermediate tenures, such as shared equity as legitimate housing outcomes that may enable households to attain homeownership,” the report said.

Article Q&A

What percentage of borrowers are in mortgage stress?

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm. Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

Will interest rates rise or fall?

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates, before easing in mid to late 2024.