Mortgage brokers are an intrinsic component in any real estate investment strategy, says award-winning finance expert from Specialist Mortgage, Helen Avis.

In the dynamic world of property investment, making informed financial decisions is crucial for long-term success.

As a seasoned property investor, there is an intricate web of factors that influence investment outcomes.

One of the key players in this realm is mortgage broker.

Their expertise can be an invaluable resource for any property venture, whether it’s a first home, investment property, or overseas purchase.

Helen Avis, Director of Finance, Specialist Mortgage, who has recently been recognised as a finalist in multiple categories of the Specialist Finance Group (SFG) National Awards, said an award-winning mortgage broker brings a wealth of knowledge that extends beyond the transactional aspect.

Why Engage An Award-Winning Mortgage Broker?

Tailored Solutions

A mortgage broker’s expertise lies in understanding the nuances of an investment strategy.

A personalised approach can ensure buyers’ financial needs are met with more precision than if left to an enthusiastic but unqualified investor.

Market Insights

As a property investor, staying ahead of market trends is crucial.

An award-winning broker will be well-versed in the shifting dynamics of the property landscape, offering insights that can positively influence investment decisions.

Optimised Financing

The ability to secure competitive financing options is a fundamental part of the broker’s role.

By assessing each unique financial circumstance and investment goal, a mortgage broker can guide clients towards loan structures that align with their long-term objectives.

Navigating Complexity

Property investment often involves intricate financial arrangements and regulatory considerations. A mortgage broker’s expertise can help in navigating the complexities of financing and ensuring compliance.

Overseas Property Purchases

Investing in Australian property from overseas adds a whole new layer of bureaucracy and financial complexity. Mortgage brokers with specific experience in this field, with experience working with expatriates and foreign buyers, will simplify the process significantly.

Holistic Approach

A mortgage broker’s role extends beyond securing loans. It takes into account an entire financial portfolio, aligning mortgage decisions with a client’s broader financial strategy.

“Whether you’re expanding your property portfolio, exploring your first investment, or navigating cross border transactions, an award-winning broker can be your compass in the dynamic world of property investment.”

– Helen Avis, Director of Finance, Specialist Mortgage

This year’s SFG National Awards will be held on 16 November.

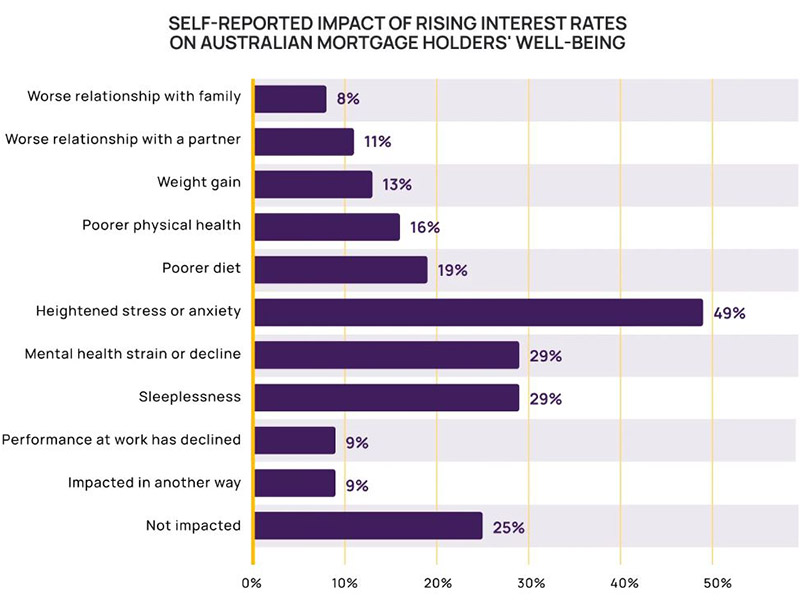

While the pause in interest rates has come as a relief to many, everyone from first home buyers to owner occupiers and seasoned investors faces the prospect of harder times before they get easier.

There is a palpable sense of relief among borrowers that interest rates have been paused for a few months and may even be on their way down in the not-too-distant future.

But the reality is that many Australians are feeling the mental, physical and financial strain of a dozen rate hikes since May last year and are struggling to cope with the markedly higher mortgage repayments.

Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

That same 75 per cent said they would not trust any Reserve Bank of Australia (RBA) interest rates forecasts again.

With mortgage interest now averaging around 6.5 per cent, the reign of interest rate hikes means households with a $500,000 mortgage on a variable rate have seen their repayments increase by $1,500 per month in the midst of a cost-of-living crisis as their incomes are eaten away by high inflation.

Source: MNY.

Compounding the situation for those struggling is the argument that interest rates will likely rise, at least once more, before the tide turns and they begin to retreat.

Inflation is on a downward trajectory, which should bring rates down with it, but there some leading indicators that the battle against inflation may not be over.

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates.

“In the short term, the risks are still skewed to a further increase in interest rates and or a delay in the start of rate cuts as: inflation is still too high; the labour market remains tight with upwards risks to wages flowing from higher minimum and award wage rises; productivity growth is very weak; and the rebound in home prices is partly offsetting the tightening impact of higher interest rates.

“Consistent with this, the RBA retained its guidance that some further rate hikes may be required.

“Key to watch will be the global economy, household spending, inflation and the labour market.”

Mortgage Stress Rampant

While the RBA has consistently stressed that Australians are well placed to manage higher interest rates after accumulating savings during Covid and paying down debt ahead of time.

But researchers are also revealing that mortgage stress is rampant.

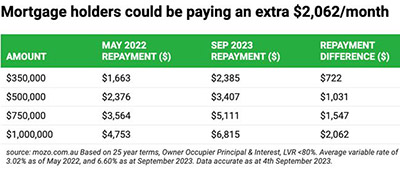

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm.

The average variable rate of an owner occupier home loan is now 6.60 per cent across all lenders, and 7.21 per cent across the Big Four banks.

Based on the average variable rate of 6.6 per cent, since May 2022 monthly repayments on a $500,000 home loan have increased by $1,031.

In a market where one in three borrowers think refinancing is too much of a hassle, Helen Avis, Director of Finance at Specialist Mortgage, said it was imperative those with stretched finances sought financial advice and better deals.

“The refinancing process may seem time-consuming but the savings on offer make it worthwhile and the application process these days is not as onerous as people may actually think.”

The incentive to refinance is also backed up by research from RateCity.com.au that reveals more than a quarter of Australians (27 per cent) are living payday to payday.

It found one third (33 per cent) of respondents were feeling stressed or uneasy about their budget, while 32 per cent couldn’t survive off their savings for more than a month if they were to lose their job.

Financial strain doesn’t just hit the hip pocket. The survey also found of those in a relationship, over a third (39 per cent) said cost of living concerns have caused increased friction with their partner about money.

First Home Buyers Facing Major Hurdles

First home buyers are being kept out the property market, often as a result of policies that had been intended to help them.

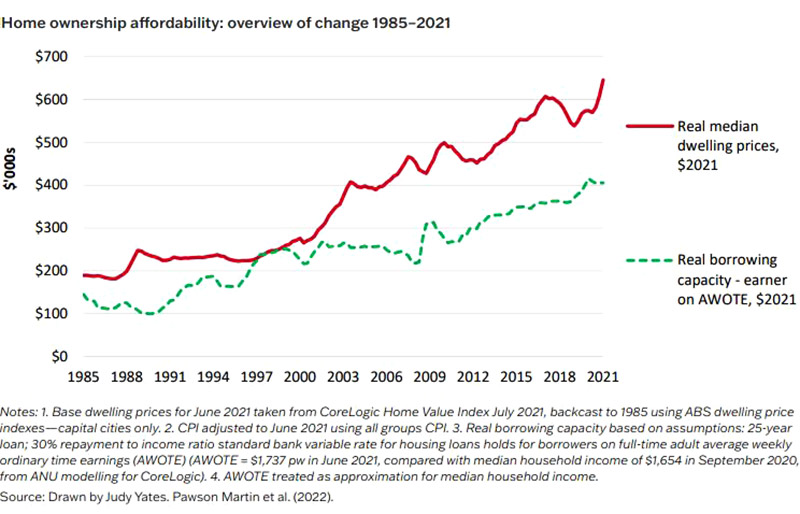

University researchers enlisted by the Australian Housing and Urban Research Institute (AHURI) found that the path to buying a first home is increasingly reliant on parental resources.

Professor Stephen Whelan, University of Sydney, said the issues confronting first home buyers were more complex than just higher property prices.

“While high and rising house prices are often cited as the biggest challenge faced by first homebuyers, our inquiry highlights that the problem is significantly more complex,” Professor Whelan said.

“Critically, we found existing policy settings are likely to have exacerbated rather than alleviated the challenge faced by first homebuyers to finance home ownership.

“Politically seductive measures such as first homeowner grants and tax concessions have failed to arrest declining rates of home ownership over time.”

A rapid expansion of owner-occupation in the early postwar period peaked at over 70 per cent in the late 1960s but was followed by a gradually declining home-ownership rate since 2000—especially among younger adults, where the rate for the 25–34 age cohort fell from 51 per cent in 2001 to 44 per cent in 2021.

There is evidence that housing affordability has decreased over time.

AHURI’s research showed that since 2001, the national ratio of median house price to median income has almost doubled to 8.5, and the time required for the accumulation of a deposit for a typical property has increased from six years median earnings in 1994 to 14 years today.

The decline in home ownership among younger adult cohorts has occurred despite expenditures in excess of $37 billion over five decades designed to enable first home ownership.

AHURI’s findings stated that policies designed to assist first home buyers must recognise and address structural issues associated with the treatment of housing in the tax and transfer system.

“Policy settings need to encompass intermediate tenures, such as shared equity as legitimate housing outcomes that may enable households to attain homeownership,” the report said.

Article Q&A

What percentage of borrowers are in mortgage stress?

Almost half (46 per cent) of mortgage holders are now under serious financial stress, according to Mozo, as home loan variable rates starting with 5, 6 and 7 become the norm. Research conducted by finance platform MNY found that three quarters of Australian mortgage holders have been adversely impacted in terms of their personal lives or wellbeing.

Will interest rates rise or fall?

Dr Shane Oliver, Head of Investment Strategy and Economics and Chief Economist, AMP Investments, said the risk in the short term is still on the upside for rates, before easing in mid to late 2024.

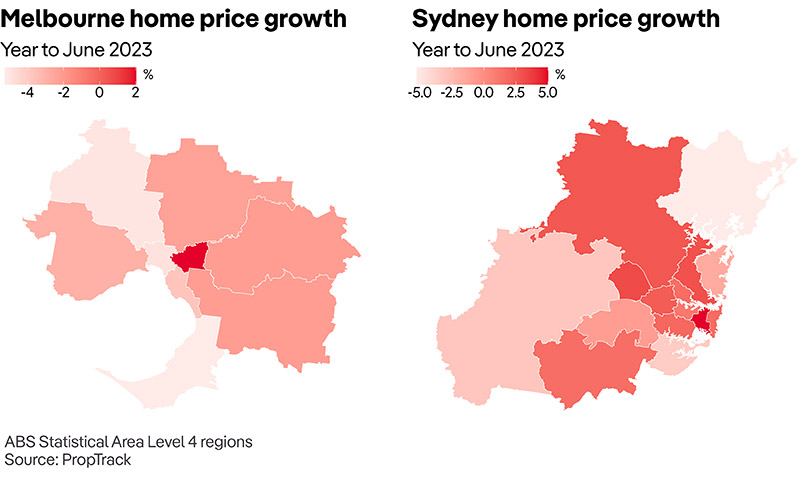

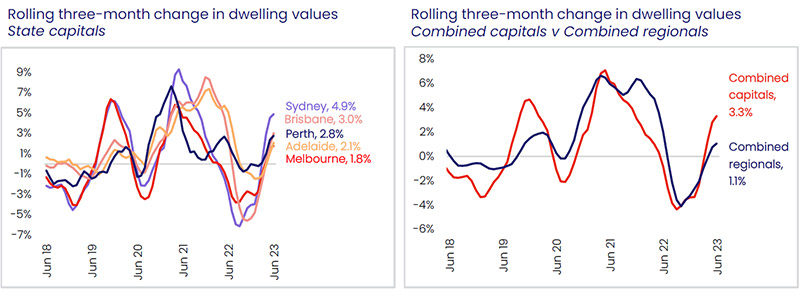

Australia’s property market has clocked up a fourth straight month of home value increases, with Sydney again leading the way, but there may be headwinds lurking.

Australia’s property market recovery has continued ticking along courtesy of a fourth consecutive month of housing value increases.

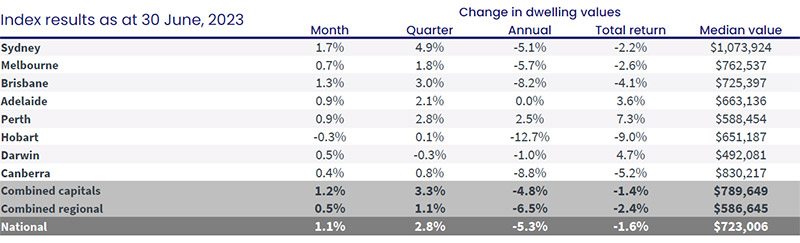

A lack of supply is outweighing the countering influence of rising interest rate and cost of living pressures, with every capital city outside Hobart (-0.3 per cent) recording gains. Regional markets outside Victoria have also trended higher.

Prices in June rose 1.1 per cent, a slight drop on the 1.2 per cent of May.

Sydney was again the frontrunner, lifting another 1.7 per cent in June and taking the cumulative recovery since the January trough to 6.7per cent, according to CoreLogic’s newly released national Home Value Index (HVI) for June.

In dollar terms, Sydney’s median housing values are rising by roughly $4,262 a week.

According to CoreLogic, since finding a floor in February, the national measure of housing values has gained 3.4 per cent, however, the market remains 6.0 per cent below peak levels recorded in April 2022. That is the equivalent of the median dwelling value still being -$45,771 below a peak of $768,777.

CoreLogic’s research director, Tim Lawless, said the number of capital city homes advertised for sale over the four weeks ending 25 June was almost 20 per cent lower than at the same time last year and 26 per cent below the average for this time of the year. Regional listings also trended lower through the month, tracking a massive 33 per cent below the previous five-year average.

Source: Corelogic

Higher interest rates were, however, slowing the pace of national property price gains.

“A slowdown in the pace of capital gains could be a reflection of a change in sentiment as interest rate expectations revise higher,” Mr Lawless said.

“Higher interest rates and lower sentiment will likely weigh on the number of active home buyers, helping to rebalance the disconnect between demand and supply.”

Deflationary Property Pressures Are Building

Also weighing on the market more and more each month is the mortgage cliff.

Helen Avis, Director of Finance at Specialist Mortgage, Australia’s mortgage market is experiencing and confronting a significant shift.

“Starting during the 2020 pandemic, there was a boom in fixed-rate borrowing as lenders slashed their fixed rates to record-low levels and many borrowers took advantage.

“At the peak, almost 40 per cent of outstanding home loans in early 2022 were fixed, which was roughly twice their usual share from prior to 2020.

“As of March 2023, about 25 per cent of fixed-rate loans outstanding in early 2022 had expired.

“By the end of 2023, another 40 per cent will expire; and by the end of 2024, another 20 per cent and presenting what has been dubbed the ‘fixed-rate, or mortgage, cliff’,” Ms Avis said, pointing out that it could play out in stifled property price pressure.

Ms Avis added that it was a good time to refinance.

“There’s a reason refinancing is at record levels and that’s because there’s significant money to be saved by doing so.”

A sign of potential trouble on the horizon is the fact the proportion of loss-making resales that were held for less than two years has trebled since late 2021, while the risk of recession from higher interest rates also weighed heavily.

Another key risk for housing conditions is the potential for a rise in advertised housing stock.

“Low inventory levels have arguably been the most important factor placing upwards pressure on housing prices,” Mr Lawless said.

“A change in the supply dynamic could become evident in spring, when the flow of listings would typically ramp up.

“We could also see more listing flow onto the market if mortgage stress becomes widespread.”

Home Values Nearing Peak Levels

Research from PropTrack released this weekend differs from CoreLogic (with a more modest 0.3 per cent national home price jump for the month) but also has prices in the black across the capitals and just 0.1 per cent lower than this time last year.

PropTrack found Sydney home prices had continued their recovery in June after leading the downturn in 2022.

Sydney home prices have now increased for seven straight months, with a 0.6 per cent rise in June. That means home prices are now up 4.5 per cent from their trough in November last year and are just 3 per cent below their February 2022 peak.

Melbourne by comparison had increased 0.2 per cent in June, bringing the city up 0.8 per cent from its low in January this year.

While Melbourne has not seen as sharp a recovery in prices this year as Sydney has, it also did not see as large a decline in 2022. Even so, prices in Melbourne are still 5.2 per cent lower than their peak in March 2022.

Across the capital cities, Perth is the only capital where home values are at record highs, having recovered from the relatively mild 0.9 per cent decline through the downturn, according to CoreLogic.

Adelaide home values are only 0.3 per cent below record highs and likely to reach a new high point in July.

Regional housing values have also trended higher, albeit at a slower pace relative to the capitals.

The combined regionals index also recorded a fourth consecutive month of growth, taking housing values 1.2 per cent higher than the recent low in February.

Source: Corelogic.

Mr Lawless said the softer growth trend across regional areas of the country align with recent shifts in demographic factors.

“After regional population growth boomed through the worst of the pandemic, internal migration trends have normalised over the past year, resulting in less housing demand across regional markets.

“Additionally, housing demand from overseas migration is skewed towards the capital cities rather than the regions.”

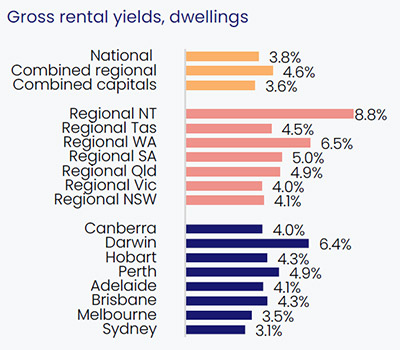

Rents Still Climbing Amid Signs Of A Slowdown

Rental conditions remain diverse across the nation, but there is growing evidence rental growth is easing.

The national rental index increased a further 0.7 per cent in June, still well above the pre-Covid decade average of 0.2 per cent month-on-month, but a continued deceleration and the smallest monthly rise since January 2023, according to CoreLogic.

The annual growth trend in rents was recorded at 11.5 per cent across the combined capital cities, down from a record high of 11.7 per cent over the 12 months ending April 2023.

Across the combined regional areas of Australia annual rental growth has slowed to 4.9 per cent, following the record high of 12.5 per cent over the year to September 2021.

Source: Corelogic.

Mr Lawless said the slowdown in rental appreciation can be seen in most cities and regional markets to different extents.

Canberra is the only capital to record a fall in rents over the past 12 months, down -2.8 per cent, while declines in Hobart rents over the past two months have dragged the annual trend to just 1.3 per cent. Both these markets have seen a loosening in supply and increase in vacancy rates.

“Although easing, the larger capitals continue to record stronger rental appreciation, especially across unit markets, where overseas migration and insufficient rental supply is continuing to place upwards pressure on rents.

“Rental vacancy rates have generally ticked a little higher over recent months, but remain well below average levels.”

Higher vacancy rates are most evident across regional Australia, rising from 1.3 per cent in February 2022 to 1.5 per cent in June, however, even at 1.5 per cent, the current rate is less than half the decade average of 3.3 per cent. Vacancy rates across the combined capitals have risen from 1.0 per cent earlier this year to 1.1 per cent but are holding well below the decade average of 2.8 per cent.

Some cities haven’t seen any signs of vacancy rates easing. Adelaide is recording the lowest vacancy rate at 0.4 per cent, up slightly from 0.3 per cent in early 2022. Perth’s vacancy rate is holding at 0.7 per cent and Melbourne’s is sitting at just 0.8 per cent.

“Despite such tight vacancy rates, it’s likely the trend in rental appreciation will continue to moderate, simply due to rental affordability pressures forcing a change in rental household formation.

“The early signs of a rebound in the average household size can already be seen in data published by the RBA,” Mr Lawless said.

In relation to the rental crisis, NSW’s Landcom was contacted on several occasions over the past few months for comment on the prospects of land supply increasing in the coming 12 months but failed to respond.

Article Q&A

Are property prices going up in Australia?

Australia’s property market recovery has continued ticking along courtesy of a fourth consecutive month of housing value increases. Prices in June rose 1.1 per cent, a slight drop on the 1.2 per cent of May 2023, according to CoreLogic.

Are rents rising in Australia?

Rental conditions remain diverse across the nation, but there is growing evidence rental growth is easing. The national rental index increased a further 0.7 per cent in June, still well above the pre-Covid decade average of 0.2 per cent month-on-month, but a continued deceleration and the smallest monthly rise since January 2023, according to CoreLogic.

Borrowers are refinancing in record numbers as their lower-priced fixed rate loans end, only to be switched to higher priced variable rates.

A Google analysis in 2022, conducted by a Queensland bank, found that the number of people searching the term ‘refinancing’ had increased by a staggering 5,000 percent.

Helen Avis, Director of Finance, SMATS Group

Lending indicator data released Friday (13 January) from the Australian Bureau of Statistics (ABS) shows a whopping $19.5 billion worth of mortgages were refinanced in November – the highest monthly amount in Australian history.

This figure smashed the previous record set in September 2022 by almost $1 billion.

“Recent ABS data has revealed that enormous numbers of borrowers are refinancing their home loans, indeed, the past six months have been the six biggest months in refinancing history,” Helen Avis, SMATS Group’s Director of Finance, said.

“Part of the reason so many borrowers are refinancing right now is because many lenders charge lower interest rates to new borrowers than loyal customers, as shown by Reserve Bank data.

“In October, owner-occupiers who took out new variable loans were charged, on average, 0.51 percentage points less than owner-occupiers with existing loans.

“Refinancing to a comparable lower-rate loan could potentially save tens of thousands of dollars over the life of your loan.”

Megan Keleher, Chief Customer Officer, Great Southern Bank

The source of the Google analysis, the Great Southern Bank’s Chief Customer Officer, Megan Keleher, said rising interest rates and the increased cost of living have affected household budgets and driven more customers to seek options to save on their home loans.

“They’re using the internet to find out how much they can borrow, how to refinance, and what support may be available for first home buyers.

“Using tools like a refinance calculator can really help; we’ve seen a 16 per cent increase in people using our refinance calculator over the last three months,” Ms Keleher said.

Negotiating a lower rate with their lender or switching in pursuit of a better deal is one of the best ways for mortgagees to prepare for even higher interest rates, Canstar’s Financial Services Group Executive and chief spokesperson, Stephen Mickenbecker told API Magazine.

“The Canstar Consumer Pulse Report released recently, found just a small proportion of mortgage holders (15 per cent) have switched lenders in the past year and secured a better deal, while only 8 per cent tried and failed. This means 77 per cent of borrowers could potentially be paying a lot more for their loan than what is on offer in the market today,” he said.

Stephen Mickenbecker, Group Executive, Financial Services & Chief Commentator, Canstar

Released in mid-December 2022, the Canstar report surprisingly revealed that when it came to mortgage holders coping with higher interest rates, almost one in two – 48 percent – of homeowners with a mortgage and 37 percent of investors with a loan – are unsure how much their mortgage interest rate has risen since the Reserve Bank started aggressively lifted interest rates in 2022.

“When asked how prepared they are for even higher interest rates, close to two-fifths (39 per cent) of homeowners and more than one-quarter (27 per cent) of investors are not prepared. The majority of these indicated they would need to cut their living costs further to make ends meet,” Mr Mickenbecker said.

“It’s disappointing that borrowers are not more engaged with getting a better deal, either from their own bank or by switching banks.

“Most borrowers are paying interest rates well above the relatively low rates being offered to new customers, and the monthly savings are too big to ignore.

“Borrowers can’t wait until they are unable to pay the bills to refinance into a lower rate loan as by then their desperation will be matched by lender aversion and they may find themselves out of luck with new lenders,” he said.

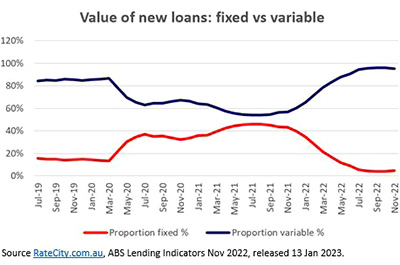

Fixed Rates About To Fall Off Cliff

As the countdown to the fixed-term cliff approaches for many property owners, few new borrowers are fixing their home loans.

The housing market, as well as borrowers, will be faced with $478 billion in fixed rates loans transferring to variable rates.

This is the so-called mortgage cliff that arises from the rollover of fixed rate mortgages taken out mid-2020 to early 2022 at interest rates around 2.5 per cent, and transitioning within the next 18 months into loans priced at 5.5 to 6 per cent. There is a large proportion of these loans falling due before the end of 2023.

“Unlike a year earlier when about half of borrowers were doing so, only 4 per cent of borrowers fixed their loans – both new loans and refinance – in October (the most recent data available).

“By contrast, 44 per cent of borrowers fixed in October 2021 and 46 per cent in August 2021, when fixing peaked,” Ms Avis said.

“While the Reserve Bank only started increasing the cash rate in May 2022, lenders knew it was coming, so they’d already started raising interest rates on their fixed- rate loans.

“In response, borrowers had begun shifting towards lower-rate variable loans.”

This is confirmed by Reserve Bank data on new owner-occupied loans.

In October 2021, the average interest rate on a new fixed loan (with a fixed period of three years or less) was 0.63 percentage points lower than a new variable loan. By February 2022, new fixed loans had become 0.09 percentage points dearer; by May they’d become 0.70 percentage points dearer.

That has since declined – by October, they were only 0.30 percentage points dearer.

Mr Mickenbecker said 39 percent of homeowners and 27 percent of borrowers polled in Canstar’s Consumer Pulse Survey in 2022 were unprepared for further rate rises.

“According to the survey, a small group of property owners (5 per cent) say they are considering selling in the next two years because they can’t afford higher loan repayments.

“While this is a small minority, the group is likely to be concentrated among more recent borrowers, with their larger loans and repayments, who have no time to have put together a buffer and have low equity.

“The impact of interest rate rises and falling property prices spreads unevenly, and recent first home buyers who overreached to get into the market will carry more than their share of the pain,” Mr Mickenbecker said.

Mortgage Stress Mounting

That pain will translate into falling house values and mortgage stress.

When surveyed for the Pulse Report, close to two fifths (39 per cent) of homeowners and more than a quarter (27 per cent) of investors were not prepared for higher interest rates.

The majority of these indicated they would need to to cut their living costs to make ends meet.

“If the price declines deepen to the point where many new loans in particular start falling into negative equity, the concern will heighten.

“At that stage, individuals will be feeling extreme pain and the system will be at risk,” Mr Mickenbecker said.

“With the full force of interest rate increases yet to take its toll, borrowers in particular look to be on a knife-edge, and have a limited buffer.

“A worthwhile New Year’s resolution for Australians might be to sit down and do a refresh of their household budget to work out a way to restore their financial resilience.”

Can There Be High Demand For Housing With High Interest Rates?

Dr Kristle Romero Cortes, Economist and real estate markets expert, UNSW Business School of Banking and Finance associate professor

Economist and real estate markets expert, UNSW Business School of Banking and Finance associate professor Dr Kristle Romero Cortés, told API Magazine she believes housing demand can withstand these financial pressures.

“Intrinsically, mortgage rates and house prices are related via supply and demand channels. If we see that the trend is that home purchases become unaffordable due to repayments, you may see a decrease in home purchases.

“However, high-income earners need more incentive to accept lower prices when selling their homes if they can afford their repayments.

“The repayment rates would need to reach a level that selling the house now to purchase one in the future eventually becomes an attractive option.

“There has already been a move to short-term fixed loans to stabilise payment expectations. This will remain the case for borrowers; it will be interesting to see how the long-run rates on fixed loans react (3 to 5 years) because, currently, those are priced high,” Ms Cortes said.

This article, first published 11 January, was updated on 13 January with the latest ABS refinancing data.

Article Q&A

What is a mortgage cliff?

When interest rates were at historic lows during Covid, many homebuyers entered the property market on very low fixed rate loans. The terms of a large proportion of these loans end over the next 12-18 months, meaning billions of dollars in loans will switch to higher variable rate mortgages. This steep, looming rise in repayments is termed a mortgage cliff.

Is now a good time to refinance the home loan?

A Google analysis in 2022, conducted by a Queensland bank, found that the number of people searching the term ‘refinancing’ had increased by a staggering 5,000 percent. Australians refinanced $17.8 billion of mortgages in October, close to the August record volume. Property finance experts suggest now is a good time to sit down and do a refresh of the household budget to work out a way to restore financial resilience.

Covid-19 is having an ever-changing impact on many things for all of us, with travel and movement restrictions, self-isolation, business shutdowns and job losses at an early stage in Australia.

The Government has been quick to act with support measures for many of those affected to reduce the impact, however there remains an understandable level of fear and misinformation floating around.

We have prepared the below summary to help you understand some of the issues being discussed and considered in regard to lending in Australia to help those affected.

It is essential to start with the clear and indisputable fact that if you haven’t been impacted through job loss, loss of rent or severe economic hardship then no actions will be available to you. There will be a requirement to provide evidence of the change in circumstances, so please understand that you can’t simply try and seek change under the hardship provisions unless you can indeed show clear evidence that something has occurred.

It is nice to know that these safeguards are in place if something happens to you, but please do not try and exploit the situation if it doesn’t.

For Those That Have Been Already Impacted

Most banks are now willing to consider changes to your current lending if you have indeed been adversely impacted by the economic consequences of Covid-19.

To qualify, you will need to either:

Have been diagnosed with Covid-19;

Lost your employment or income significantly reduced; or

Your rent on your investment property is not being paid

In these cases, banks are willing to:

Allow up to 6 months deferred repayment on your loans to assist your cash flow, but during this period interest will still be charged and accrued.

The loan term will either be extended for that period or you can pay the backlog during the existing term through a higher repayment once it recommences.

Taking a deferred mortgage repayment will not affect your credit rating.

For Those Not Impacted

If you have not been directly affected by Covid-19, then the banks are still assessing their options on existing clients, including whether or not to pass on the recent official interest rate cuts for investor loans.

There are some special fixed rates now available for owner-occupiers where they have passed on the recent reductions by up to 0.7%pa.

We do expect some further announcements shortly and will keep you posted.

The banks are currently offering higher discounts on variable interest rates, so if you haven’t had your loan reviewed recently, please contact us to ensure you are getting the best discount on your lending.

New Loans

Despite the current environment, banks are still willing to lend for new purchases and refinances.

Some restrictions may apply to employment in certain industries directly impacted by Covid-19 such as travel and tourism.

We would be pleased to help you further evaluate your options and assist in ensuring that you are achieving the best result for your circumstances. Simply email us at [email protected] to connect with one of our professional team members near you.

Buying an off-the-plan property is a great way to enter the property market, but there are a few considerations you need to know about when it comes to financing a new purchase.

There are many advantages to purchasing off-the-plan, despite the fact that your new home still hasn’t been built. Not only can you access possible tax benefits through depreciation, but you also get a brand new home with all the new fixtures and fittings.

Another key advantage is that you often only need to come up with a 10% deposit; however, the financing process has a few nuances that new buyers need to be aware of.

Have Your Finance In Order ASAP!

When buying off-the-plan make sure you have your finance in order as soon as possible. Submit your application up to four months prior to settlement. Once approval is granted, you will have to wait until the building is finished and valued before everything can be signed off and you can move in.

What Is Required In Terms Of LVR?

The LVR your lender requires depends on a few different factors. A key consideration is always based on whether the property is for an owner occupier or an investment. The size and location of the new building is also significant because if it is in a high-risk postcode or if the development has more than 50 units, this will impact the LVR requirements.

Generally speaking, the maximum LVR you would be able to access as an owner-occupier is 90/95% and 80-90% for investors.

Prepare For Potential Risks

One of the key considerations is that when you purchase an off-the-plan property you are having to sign the contract far in advance of moving in, which means there is a risk that lending policies might change between that time and final settlement.

Market conditions may also change, and the valuation of your new property, when completed, may come in lower than you anticipate. Be sure to have a buffer of cash, so you can settle even if the final valuation is on the low side and you aren’t able to access the full amount you need from your lender. It’s also important to note that failure to settle means you lose your 10% deposit.

Overcoming Any Hurdles

When purchasing a property off-the-plan, it is crucial to ensure that you are in a position to pass the servicing requirement for the total loan amount, at the date of settlement.

Having an additional buffer of cash available in case of lower lending or lower valuation is a good idea as well.

It is also essential to understand the area that you are looking to buy into. If the particular suburb has a large pipeline of new stock coming onto the market, then you might need to be careful as this could weigh on the final valuation when you are looking to settle.

An Example Of The Process:

When you have selected your new property, check that you can qualify for the loan amount required at settlement. Once the contract is signed, and a deposit of 10% is paid nothing further is required until nearer settlement. Then at least four months prior to settlement prepare the application for submission and make sure you have a cash buffer in place.

A Great Way To Enter The Market

Overall, buying off-the-plan property is a great way to get into the market, and at times you might even be able to access favourable lending terms with the help of the developer.

While there is some risk when it comes to gaining finance, given the time between signing the contract and final settlement, most of these risks can be overcome by fully understanding the process and planning for a final valuation that is in a range, rather than a set figure.

Article Q&A

What is the maximum LVR?

The maximum LVR you would be able to access as an owner-occupier is 90-95% and 80-90% as an investor.

Disclaimer

All information provided in this article is of a general or factual nature only and does not take into account your personal circumstances or objectives. Before making any decisions, you need to consider, with or without the assistance of a licensed adviser or broker, the appropriateness of any material presented in light of your individual needs and circumstances. The information in this article does not constitute a recommendation for any of the products or services provided by SMATS Services (Australia) Pty Ltd and or any of its related entities.

Whether you are hoping to create that dream home or looking to make a solid investment, purchasing a block and building new is a great option. As with any purchase, understanding the financial process and any potential risk is key to your overall success.

As a potential homeowner or investor, building your property from scratch comes with many benefits. Control over design specifications, fewer maintenance issues moving forward, lower energy costs and the ability to access greater tax incentives through depreciation make this an attractive option for many buyers.

A further financial upside of buying a block and then building is that stamp duty is only paid on the land, not the construction, therefore reducing your overall costs.

If this is the choice for you, securing finance is one of the first steps – as without funding, a construction project will never get off the ground.

So how do you go about financing your build, and what are some of the potential risks to look out for?

It’s A Process: Securing Finance

The process of financing a new build is different from established property as it involves two distinct components: land and construction.

You can obtain a packaged finance product that covers both: when signing the land contract you will be required to put down a 10% deposit, and then a 5% deposit when signing the construction contract.

On settlement of the land, you will pay your full contribution for the land and the build cost. The bank will then settle the balance for the land, and finance the entire build cost.

Interest is charged on the amount drawn, so initially, this will only be on the land component of the loan.

Generally, there are five staged payments to complete a house. After each stage is completed, the bank will pay the invoice and interest will be charged as each drawdown is made.

What Is Required In Terms Of LVR?

The required Loan to Value ratio (LVR), which is the amount of a loan compared to the value of the property, will differ for buyers looking to purchase their own home compared to those looking to invest.

For owner-occupier applicants, 90% finance or even up to 95% finance through some lenders is achievable. While for investors looking to obtain land and construction finance, 90% is currently the maximum.

Both homeowners and investors looking to borrow over 80% of the total land and construction value are required to obtain Lenders Mortgage Insurance (LMI). In some cases, this can be added to the loan, while in other instances, depending on the lending limit, the LMI needs to be paid on settlement.

Potential Pitfall: And How To Avoid It

Before signing a contract, potential investors or future homeowners should always obtain pre-approval, so they can be confident that their bank or financial institution will lend the total amount of financing required to settle.

Both contracts for the land and construction can be signed subject to finance. Then, the total land and construction project can be valued prior to the purchase becoming unconditional; to help ensure enough funding is secured and there is no shortfall.

An Example:

Let’s look at the breakdown of the numbers on a project with a land price: $300k and construction cost: $300k.

Land price: $300k

Construction cost: $300k

Loan: 80% LVR

Total cash deposit required: $120k

Total loan: $480k

Additional costs to settle: $15k (approx)

Once a buyer has obtained conditional approval for financing, 10% will be paid on the land ($30k) and 5% on the construction ($15k).

The balance of funds required for the total cash deposit is $75k. The loan to settle the land is $195k, and the loan to settle the construction is $285k. Having paid $15k up front, this means the bank pays the remainder of your construction cost.

Understanding The Process Is Key To Your Success

Whether you are hoping to create that dream home or looking to make a solid investment, purchasing a block and building new is a great option. As with any purchase, however, understanding the financial process and any potential risk is key to your overall success.

Disclaimer

All information provided in this article is of a general or factual nature only and does not take into account your personal circumstances or objectives. Before making any decisions, you need to consider, with or without the assistance of a licensed adviser or broker, the appropriateness of any material presented in light of your individual needs and circumstances. The information in this article does not constitute a recommendation for any of the products or services provided by SMATS Services (Australia) Pty Ltd and or any of its related entities.

How to make your offspring financially savvy.

Unlocking Financial Wisdom at any age, the Top 6 things you can impart now!

Nurturing Financial Life Skills in Children

In the intricate tapestry of life, imparting financial literacy to our children stands as a crucial thread. The earlier we weave this thread, the more resilient and empowered our children become in navigating the complexities of the financial world. It’s a lifelong skill that transcends age, and there’s no better time to start than now. I’ll discuss some easy principles to start with and some fun learning activities to engage in with your soon to be financially savvy offspring!

These activities lay the groundwork for a healthy financial relationship by instilling the values of saving, budgeting, earning, and making thoughtful financial decisions from an early age.

Starting Early: The Power of Seeds

Financial education is like planting seeds of wisdom. The earlier we sow them, the deeper the roots grow. As the adage goes, “mighty oaks from little acorns grow.” Simple lessons about saving, spending wisely, and understanding the value of money can be introduced even in the early years.

The Savings Jar – Start with a simple savings jar for each child. Teach them to allocate a portion of any money they receive into the jar. Discuss goals for the savings, whether it’s for a special toy or a future treat.

The Wish List – Create a wish list with your child, including items they desire. Discuss the concept of prioritising and saving for more significant items. Encourage them to revisit the list periodically, adjusting priorities as needed.

Going digital – cash was king, but now purchasing, buying habits even transferring money is all done online and with more and more banks shopping up shop and going completely digital perhaps setting up an online bank account and demonstrating that just because you don’t have physical cash doesn’t mean you need to rely on the plastic card.

Set your goal, save – then spend without any cash slipping through those fingers!

Age-Appropriate Lessons: Tailoring Wisdom

Adapt the lessons to the age of your child. For young children, start with tangible concepts like using piggy banks to save. As they grow, introduce budgeting for toys or treats. For teenagers, delve into more complex topics like loans and debts, preparing them for the financial decisions that await them.

Avoid the ‘satisfaction straight away’ stigma and teach the art of patience – wait for something, save up and then spend, don’t spend first with money you don’t have!

Budgeting Game – Develop a simple budgeting game where your child manages a hypothetical budget for a week. Allocate funds for various categories like toys, snacks, and savings. Discuss the outcomes, reinforcing the concept of making choices with limited resources.

Real-world Application: Learning by Doing

Children learn best by doing. Consider giving them an allowance and encouraging them to budget for items they desire. As they make choices, they grasp the concept of trade-offs and consequences. Real-world application transforms theoretical knowledge into practical wisdom.

Earning Allowance – Introduce the idea of earning money through chores or tasks, outside of their regular household duties. Think of these as little tasks you would get someone to do for you. Assign a monetary value to each task, allowing them to see the connection between effort and reward. Discuss the importance of work ethics and responsibility.

Open Conversations: Diminishing Financial Stigma

Create an open dialogue about money. Remove the stigma associated with financial discussions. Whether it’s a trip to the grocery store or planning a family vacation, involve your children in financial conversations. This demystifies money matters, fostering a healthy relationship with finances.

Grocery Shopping Adventure – Take your child grocery shopping and involve them in the process. Provide a small budget for a particular meal or snack. Encourage them to compare prices and make choices within the budget.

Utilise Resources: Tapping into Tools

In a digital age, educational resources are abundant. Utilise interactive online games, books, and educational apps that make learning about finances engaging. Many platforms provide age-appropriate content that transforms financial education into an enjoyable adventure.

Leading by Example: The Ripple Effect

Children emulate the behaviours they witness. Be a positive financial role model. Share stories of financial successes and challenges. Demonstrating responsible financial habits instils a lasting impact, shaping their own financial attitudes.

Role-Playing Purchases – Engage in role-playing scenarios where your child takes on the role of the buyer. Provide them with a set budget and guide them through making decisions. Emphasise the importance of critical thinking and making informed choices.

In a world where financial decisions impact every facet of life, instilling financial life skills in our children is an investment in their future. Remember, it’s never too early or too late to unlock the doors to financial wisdom for the next generation.

Specialist Mortgage, a part of the SMATS Group, specialises in providing tailored mortgage solutions for Australian expats and foreign investors. The team of experts led by Helen Avis, have consistently provided tailored mortgage solutions to clients worldwide, helping them achieve their property ownership dreams.

With a focus on personalised service and in-depth industry knowledge, Specialist Mortgage has established itself as a leader in expatriate and foreign national home loans.

A leading property management expert has identified three key areas landlords can address to ensure they get off to the best possible start with a new tenant and their property manager.

With rents still on the rise around the country, property investors could be excused for thinking the rental income will look after itself.

But with mortgage repayments devouring much, if not all, of that extra rental income, it can pay dividends to enlist a property manager and adhere to some essential tips to maximise rental returns from the outset of the investment.

Kirsty Pilcher, Head of Department – Property Management, aussieproperty.com, has identified three vital components to ensure a rental property is best placed to attract the right tenants, retain its value and capitalise on record low vacancy rates and a tight rental market.

Set the standard early

Presenting your property to the highest standard before a tenant has been secured has many benefits.

Your advertising photos will look fabulous and you are more likely to attract a higher quality tenant who is looking for a well-presented home.

However, something not often considered by an owner is that when a property is handed over at the start of a tenancy, if this property has been professionally cleaned and the gardens recently attended to, it sets the standard for all of the following routine inspections and ultimately the final inspection.

The tenants must continue to present the property to the same standard and return the property in the same condition when the tenancy comes to an end.

If the tenant chooses not to maintain the same standard throughout the tenancy, this is obvious and can be addressed by your property manager, usually at the tenants’ expense.

Prepare a maintenance budget

Maintenance issues at your investment property can be costly and may come at a bad time.

Under the Residential Tenancy Act WA, for example, reported maintenance must be attended to within certain timelines. An owner is obligated to meet these timeframes.

Having a maintenance budget allows your property manager to organise repairs in a timely manner and also service appliances regularly to help avoid emergency maintenance situations arising.

Have proof of ownership ready for your property manager

Under the Residential Tenancy Act your property manager must confirm you are the owner of the property being rented out.

We cannot begin the process of managing your property without this.

The best way to prove ownership is to provide a copy of your Certificate of Title.

Your property manager can order a new copy of this, however, there are costs involved.

To avoid that cost and any delays with getting your property advertised, have your copy ready to pass on at the time of signing your Management Authority.

In addition to these property management tips, property investors looking to buy a rental property should also be aware of these top three rental market factors when trying to pinpoint that successful investment, as well as the need to have adequate insurance coverage.

Article Q&A

What should landlords do before they rent out their property?

A leading property manager has identified three key areas that will ensure a new rental tenancy goes as smoothly as possible, including tips on maintenance, property presentation and contractual requirements.

With the Reserve Bank of Australia set to raise rates throughout 2022 and the banks following without hesitation, is it time for homeowners and investors to reshape their bank finance?

The Reserve Bank of Australia (RBA) has lifted its official cash rate by 25 basis points to 0.35 per cent, the first such upward movement since November 2010.

With markets pricing in the virtual certainty of another rise in June to take the cash rate target to at least 0.5 per cent, there is a degree of fear among many home owners and investors who face the prospect of repayments that stretch already-pressured household budgets.

If passed on in full by banks, the rate rise will add more than $65 a month to repayments on a $500,000 mortgage, and double that on a million-dollar loan.

Whatever the outcome for individual property owners or investors, industry leaders suggest there are numerous ways to prepare your mortgage and minimise interest rate rise shockwaves.

Time to refinance?

Now is the perfect time for homeowners and investors to review the interest rates attached to their borrowings.

Zippy Financial Director and Principal Broker Louisa Sanghera said as interest rates rise it will become harder to qualify for a new loan and is all the more reason to refinance.

“A 0.25 per cent difference to an investor not only eats away at their income, but it can make a difference to them being positively or negatively geared, which in turn could cost them in tax,” she said.

According to Two Red Shoes founder and mortgage broker Rebecca Jarrett-Dalton, if you haven’t reduced your rate during the last two years, you should definitely look at refinancing.

“Variable rates are so competitive, why wouldn’t you try and save some interest?” Ms Jarrett-Dalton said.

Mortgage broker at Specialist Mortgage, Carolyn Xaftellis, agreed one of the best reasons to refinance a home loan was to lower the interest rate on an existing loan.

“Refinancing can be a great financial move if it reduces your home loan repayment, shortens the term of your loan, or reduces the amount of interest you pay across the entire loan term.

“On a $500,000 principal and interest loan a drop of 0.5 per cent will save $135 per month,” Ms Xaftellis said.

However, it’s not just the interest rate that will make an impact.

“It’s important to look at initial and ongoing fees and the use of interest reducing facilities such as an offset account,” she said.

“An offset account with an average balance of $25,000 on a 3.19 per cent principal and interest loan will save $797 per year in interest costs, which will reduce the balance of the loan and overall loan term,” she said.

Paying regular attention to changes in lender offerings is also important, suggested Specialist Mortgage’s Senior Finance Executive, Bridget Bowman.

“If your current lender is not prepared to offer a competitive rate, there will be another lender that will.

“This can often result in savings of thousands of dollars over the course of a year, so it’s definitely worth asking the question,” Ms Bowman told API Magazine.

Fixing the problem

The decision whether to fix a rate or go with the variable alternative is, according to Ms Jarrett-Dalton, “crystal ball territory”.

“This one is a very hard one to answer,” Ms Jarrett-Dalton said.

“The standard caveat applies – it depends on your personal needs and circumstances, how long you plan to keep the property, how much extra you can repay, etc, but more than this, if you are fixing a rate right now you are effectively giving yourself a rate increase before the banks do so,” Ms Jarrett-Dalton said.

This is because the offered fixed rates currently are an average of 1 per cent to 2 per cent higher than variable rates.

Borrowers are largely ditching fixed rate home loans. Fixed rate lending is, at 28 percent of new lending in February, way down from a peak of 47 percent in July last year.

“You might still think this is worthwhile if it lets you sleep at night or if you think rates will rise more than this amount during the term you choose.

“For example, two-year fixed rates are hovering on average in the high 3 per cents; do you think variable rates will rise more than one full per cent within the next two years for you to have been better off in your fixed rate from now?”

Mortgage Choice and Smartline National Sales Director David Zammit said ultra-low fixed interest rates are now a thing of the past.

“To put things into perspective, the lowest fixed rate on the Mortgage Choice panel of lenders today is 2.69 per cent p.a. and the lowest variable rate offered by a lender on our panel is 1.89 per cent,” he said.

“Borrowers are responding – Mortgage Choice home loan submission data showed that in March, 20 per cent of loans had a fixed component (80 per cent variable) compared to March last year when 39 per cent of loans had a fixed component (62 per cent variable).

“That said, RBA rate rises will push up the cost of variable interest rates.

“Those borrowers looking for certainty will still favour fixing their rate so they know their maximum repayments for that period of time,” he said.

Making mortgage calculations

The quickest way to assess how a rate rise will impact a homeowner or investor is to use their lender’s online repayment calculator, says Specialist Mortgage’s Bridget Bowman.

“This allows customers to determine how much a percentage rate rise will impact them in terms of dollars.”

Ms Jarrett-Dalton said there is much that goes into a loan assessment, so it’s not as simple as only using a calculator.

“But if you’re going to, avoid the borrowing capacity calculators as these are very rough only – and stick to a simple loan comparison or simple maths; your current loan balance, multiplied by the potential interest rate saving, then divide this by 12 if you’d like a monthly figure,” she said.

After entering the loan amount and interest rate, Ms Sanghera recommends increasing the interest rate in the calculator by 0.25 per cent increments to see how their mortgage could potentially rise.

“I would recommend doing this up to, say, an interest rate of five or six per cent.

“If you are worried you cannot manage the potential repayments, then you should go and speak to your broker, who can restructure the debt to reduce repayments, or they could look to fix the interest rate on your home loan,” she said.

“We are already seeing our clients paying under the asking price and sales agents advertising “price adjusted” so prices are already slowing down,” Ms Sanghera said.

Ms Jarrett-Dalton has also witnessed hesitancy from property owners.

“People are factoring in price drops.

“If they aren’t yet in the market, they are also hopeful and waiting for a bargain.

“This is in itself a little bit self-fulfilling.

“Definitely as rates rise and it’s a little harder and dearer to borrow, this will have an impact but the biggest factor still seems to remain supply versus demand and this is without inward migration.”

While affordability is also a key concern, Carolyn Xaftellis suggested the cost of borrowing is likely to remain well below long-term averages.

“There will be continued housing demand for an extended period of time,” she said.

“Other factors to consider are trends in labour markets, demographic patterns, supply levels and affordability, which will all play a key role in how housing markets perform in different parts of the county.”

Optimistically, REINSW CEO Tim McKibbin’s overview is that in the current environment an interest rate rise is unlikely to result in too many mortgagors being pushed into difficulty.

“Through APRA, banks are already required to build into a finance facility the capacity for a mortgagor to absorb additional costs to service the debt,” he said.

A rate rise is also likely to create competition between banks.

“The competition between banks to win your business is going to be intense, so use your broker to make sure you get the best deal,” David Zammit said.