Undeterred by property prices in Melbourne and Sydney coming off the boil or the threat of higher interest rates, expatriate Australians are continuing to snap up prestige properties.

Undeterred by property prices in Melbourne and Sydney coming off the boil or the threat of higher interest rates, expatriate Australians are continuing to snap up properties priced considerably higher than median city values.

Helen Avis, the SMATS Group Director of Finance, said the expatriates that had recently returned to Australia were moving from rentals into their own properties and could afford prestige real estate in highly sought-after areas.

“The $2 million to $4 million bracket has been very active as expats plan their eventual return and want to buy the future home, or move from their temporary rentals having recently returned,” Ms Avis said.

The recently-name finalist in the national Better Business Awards, in Best Residential Broker category, said she had also seen a lot of buyers targeting regional areas, holiday locations and the holiday home market.

“There’s very little investor or expatriate interest in CBD city apartments – that market has dried up – but there is still a lot of demand for luxury apartments as well as houses in the higher-priced suburbs.”

The first quarter of the year has seen Australian dwelling values rise by 2.4 per cent, less than half the pace of the same period last year.

But expatriates seeking a home rather than an investment can afford to pay the premiums that two years of rapid price growth has delivered and are not phased at the prospect of higher interest rates.

Interesting times

The big four bank economists are forecasting official cash rate hikes could begin between June and September.

Not waiting for the Reserve Bank of Australia, Australia’s third and fourth largest banks, NAB and ANZ, on Friday (1 April) hiked fixed rates by up to 0.40 percentage points.

“We have seen all banks raise fixed rates so many times in the last six months and I expect the RBA will raise rates from June,” Ms Avis said.

Helen Avis, finalist in the Better Business Awards

“I don’t think they want to raise them and then continue to raise them regularly, so it should be a slow progression, but the market is expecting interest rates to rise.

“All borrowers are assessed at 3 per cent over the benchmark rate, so it shouldn’t put stress on people’s ability to maintain their loans.

“With the borders just opening back up, we should have a two-year backlog of intended migrants, expats and international students start to push up the rental market as well as CBD sales.

“The intended migrants will likely rent to start off with, but most will likely want to buy, so demand will again be strengthened.”

Ms Avis said SMATS Group’s aussieproperty.com had clients looking at all states’ markets but Queensland was generating the most interest.

Sydney, Melbourne, Perth and the West Australian southwest were also on the radar of returning expatriates, she said.

The Better Business Awards seek to champion the leading players of the broking industry in each state and territory of Australia.

Reaching the finalists stage is regarded as an incredible achievement across the Australian broking industry, showcasing the depth of dedication and commitment each individual and team brings to advancing the industry.

Ms Avis said she was humbled to be recognised and proud to be named as a finalist. Winners are announced at a ceremony on 19 May.

Applying for finance as a first-time investor can be a complicated process that features several subtle differences from obtaining a loan for a property intended to be lived in.

But if investors have a solid understanding of what lenders are looking for, the process can be as smooth as applying for owner-occupier finance.

Specialist Mortgage director of finance Helen Avis told Australian Property Investor Magazine that there were several crucial pieces of information a first-time investor needed to know before making an application.

“They need to know the full financial process – their borrowing capacity, how much cash is required to settle and their loan options, whether they lock in a variable or a fixed rate loan, and the fees associated with the finance,” Ms Avis said.

“They should be made aware of the timeline for the financing process and should have a pre-approval in place before making offers on a property.

“And they will need to appoint a conveyancer to assist with the legal aspect of buying a property.”

The biggest factor that the banks are looking for, Ms Avis said, was that there will be sufficient income – earned and rental – to support loan payments after deducting liabilities and expenses.

Other differences between owner-occupier and investment loans include the maximum loan-to-value ratio that banks are willing to lend on, as well as higher interest rates for investors as compared to borrowers who intend to live in the property.

Rebecca Jarrett-Dalton, founder of Sydney-based mortgage broker Two Red Shoes, said many investors were also not aware of the subtle differences between lenders.

“We sit in a really privileged position where we can overlook all of the lender policies and there are so many different nuances in policies coming into play at the moment, so it’s actually really challenging for somebody to get it right by walking in the door of their local bank branch,” Ms Jarrett-Dalton told API Magazine.

Ms Jarrett-Dalton said lenders would differ on the maximum debt-to-income ratio they allow, while there were several things a prospective borrower could do to ensure that ratio does not hold them back from achieving their goals.

“All of the standard stuff applies – getting your house in order, not spending all your money on Uber Eats, expanding your income as much as possible, reining in any unnecessary liabilities or expenses all helps you,” Ms Jarrett-Dalton said.

“For a first time investor, a crucial factor is knowing what you want to get out of it.

“Even as foolish as it sounds, you need to know your exit strategy before you begin and decide which type of property.”

Ms Jarrett-Dalton said understanding the drivers behind investing and what an investor’s future goals are was crucial in the decision-making process around what to buy.

“Every property is the right property for the right person. It’s not that there are wrong properties, but it might cost you more to hold a particular property as an investment,” she said.

“If you bought in Sydney at the moment, it’s going to cost you a lot more to hold the property because rents are so far behind property prices.

“But if you bought in a more regional area, you will get a greater rent return against your dollar spend.

“Neither of them are the wrong property, they’re just for the right purchaser.”

And Ms Jarrett-Dalton said buying a property that’s heavily negatively-geared for tax deduction purposes may seem like a sound strategy, but it could also put a handbrake on potentially building a portfolio.

“If your goal is to buy 10, just to pluck a number out of the air, and your first one is so heavily negative, that’s going to really hold you back.

“We are seeing a lot of popularity in regional dual-occupancy properties – houses with granny flats, or a duplex on a property, if you bought that one first, that’s probably going to help you moving forward.”

Ms Dalton also shared her top tips on what lenders may consider when assessing an investment loan application:

Rental income

Running costs

Your debt-to-income ratio

Have your documents in order

Understand your goals and find the right property

With the mortgage cliff around the halfway point of its gradual transition from low fixed to high variable rate loans, is a looming disaster unfolding or are borrowers proving to be more resilient than expected?

It’s late August and the midway point of what was dubbed the mortgage cliff.

This so-called cliff was named to denote the lemming-like fate that supposedly awaited all who had to move from super low fixed term loans secured from mid-2020 to mid-2022 to loans up to triple that interest rate.

While its progression is far from complete, and much of the impact of this mass switch may still be yet to play out in full, the doomsday scenarios have not eventuated at this stage at least.

There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings over the past few weeks.

But overall, the risk of arrears and default remains contained within Australia’s large mortgage market and a level of resilience demonstrated amid tight labour market conditions.

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season.

While homeowners are, in broad statistical terms at least, not selling up en masse, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

“The Mortgage Cliff Was All Media Hype” – Helen Avis, Director of Finance, Specialist Mortgage

The number of Aussie home loan holders refinancing soared 13.8 per cent in the financial year just completed, while those signing new mortgages fell 20.6 per cent, new research from PEXA shows.

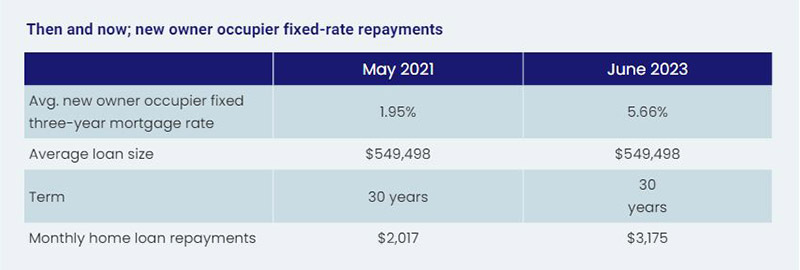

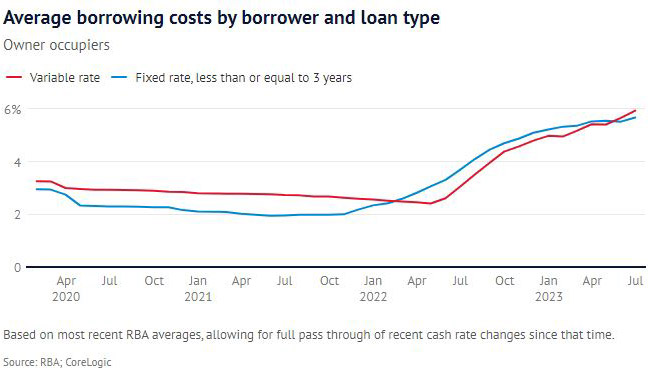

That comes as mortgage holders contend with a transition from interest rates on a loan of around 1.9 to 2.5 per cent leaping to between 6 and 7 per cent.

In terms of what that means to a household’s budget, the repayment on a $750,000 mortgage set at 2 per cent would soar from $3,180 a month to $4,830 a month – an increase of more than 50 per cent overnight, assuming a new rate of 6 per cent.

Yet it seems official data on mortgage stress has not seen a blow out in arrears amid the expiry of low fixed-term loans.

Portion Of Outstanding Loans In Arrears

Eliza Owen, Head of Residential Research Australia, said as home values rise, the risk of default also remains low.

“As what is likely to be the last of the RBA’s rate hikes is passed through to households with a mortgage, there may be a mild deterioration in housing market conditions if new listings decisions continue to rise.

“The good news for mortgage holders is that this period of economic slowdown will also take the RBA closer to its long-term inflation target, which could be the impetus for a reduction in the cash rate in the second half of 2024, as predicted by most major banks.”

Whether there is another 0.25 per cent increase in the official cash rate by the RBA is an even money bet. But the governor, Philip Lowe, used the just-released RBA Board Minutes for August to acknowledge the mortgage cliff was a consideration in their decision-making process around interest rates.

“Members noted that banks had continued passing increases in the cash rate through to their customers, and that outstanding mortgage rates and scheduled mortgage payments were set to increase further as a high share of fixed-rate loans roll onto higher rates through the rest of 2023.

“Scheduled mortgage payments as a share of household disposable income increased to 9.4 per cent in the June quarter, around its historical peak.

“Voluntary principal payments into borrowers’ offset and redraw accounts declined in the June quarter (while) net flows into these accounts had declined to be noticeably lower than the pre-pandemic average, consistent with pressures on disposable incomes.”

To be more concise, borrowers are hurting.

Finding more than $1,000 a month for mortgage repayments isn’t easy for everyone.

Climbing Or Falling From The Mortgage Cliff?

Industry sources are divided on just how severe the implications of the mortgage cliff’s continued unfolding will become. Some argued it was driven by an excitable media while others declare it’s downward spiral with no imminent escape route.

In the former camp, Helen Avis, Director of Finance at Specialist Mortgage, said “the mortgage cliff was all media hype.”

“I cannot see rates rising too much further, and if that is the case then we should not see much more of an adjustment from where we are at now.

“I am not surprised with the lack of delinquencies, with the still relatively strong property market and borrowers able to handle the increases.

“That said some borrowers have been affected and are struggling but the vast majority seem to be coping.

“I know some first home owners who have rented their property and gone back to live with parents, capitalising on the acutely tight rental market to offset the stress of higher mortgage repayments.”

Joe White, President, Real Estate Institute of Western Australia (REIWA), said we are well into 2023 and we have not seen the apocalypse we were told was coming.

“While there have been constant predictions of a flood of forced sales, REIWA data does not yet show an increase in properties advertised as mortgagee sales or mortgagee in possession.

“There is no denying 12 interest rate increases have had an impact on households, but it is disingenuous to underestimate a homeowner’s capacity and willingness to adjust their spending habits.

“Many homeowners on fixed rate loans have prepared for the dreaded mortgage cliff.

“They have paid extra onto their mortgage to be ahead with their repayments, have created a savings buffer or have refinanced.”

API Magazine’s recently released Property Sentiment Report found that the percentage of respondents defining their situation as being in mortgage or rental stress was easing.

While still disturbingly high at 36 per cent, it was an improvement on the 43 per cent of the previous quarter. Disconcertingly, 79 per cent said their financial stress status had eventuated over the past 12 months.

Mark Bouris, Executive Chairman, Yellow Brick Home Loans, however, was far less optimistic than others, reporting that the consequences of the interest rate hikes won’t be fully laid to bear until Christmas this year, as more and more home loans move from cheap fixed rates to high variable rates.

“Expect families to be forced to sell their homes, many to property investors and foreign buyers, and end up in the already-crowded rental market that is driving up inflation.

“Otherwise, families will be forced to cut back their spending on everything from holidays to food to recreational activities and school fees – the list goes on.

“This will hurt the small businesses that rely on consumer spending to pay their bills, which are also rising.

“It’s a vicious cycle, and there’s no clear way out.”

There has been a sharp spike in landlord exits from the property market across Australia.

Victoria is the worst-hit state, with the latest PropTrack figures revealing 30.1 per cent of sales were properties that had been listed for rent since they were purchased.

That’s up from 24.7 per cent in July 2022, and 16.9 per cent in July 2019, before the pandemic. New South Wales followed at 28 per cent, which like Victoria, was also the state’s highest share of investment home sales since late 2018. Queensland was third with 27.15 per cent of sales in July being rental properties.

Regardless of which side of the fence you sit on in terms of the mortgage cliff’s ultimate impact, the rest of the year promises to offer compelling viewing of the economy, housing market, and the financial viability of renters, home owners and investors alike.

Article Q&A

What is a mortgage cliff?

The mortgage cliff refers to the sudden large increase in repayments mortgage holders on fixed rate loans will face when their term ends and their loans revert to variable, and the subsequent effect this will have on the property market.

What has been the impact of the mortgage cliff?

While its progression is far from complete, the doomsday scenarios of the mortgage cliff have not eventuated at this stage at least. There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings.

Will property prices fall because of the mortgage cliff?

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season. While homeowners are, in broad statistical terms at least, not selling up en masse because of the mortgage cliff, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

By leveraging the equity in your current property, you can quickly take that one property…and build a portfolio that can fast-track you towards your financial goals.

By leveraging the equity in your current property, you can quickly take that one property… and build a portfolio that can fast-track you towards your financial goals.

If you already own a house or investment property, you may have equity available that you can put to use for your next.

So how can you leverage your current equity to make that next purchase?

Your equity amount is the current value of your property minus the outstanding loan. Banks will lend up to 80% of this amount for a new purchase without Lenders Mortgage Insurance or up to 90% with.

A risk to watch out for: with a higher loan on the property, annual holding costs are more than if you put in the cash deposit yourself.

To minimise this risk, ensure that you are purchasing a quality property that you feel will increase in value each year by more than the annual holding cost of the property.

The power of leverage. It really doesn’t take long to build yourself a very powerful property portfolio when you start leveraging your existing equity.

Living overseas as an expat can be a fantastic move financially and can allow you to progress up the property ladder quickly. When purchasing off-the-plan property, however, there can be a few additional hurdles to consider when applying for finance.

Living the life of an expat has plenty of benefits. You are generally paid extremely well and in many cases get to live rent-free in some of the most vibrant cities in the world.

On the flip side, for those Australians living and working overseas, the big catch can come when looking to gain finance to buy a property, back home. If you are looking to purchase off-the-plan, this process can be even tougher as it comes with some additional considerations.

If you are going to buy an off-the-plan property, it is well worth taking a few key steps early on in the piece to make sure everything is in order.

Gaining finance: it’s a process

When purchasing off-the-plan, it is important for you to have your financial position assessed early. In most instances, there is no subject to finance clause, and if settlement is 1 – 2 years away, there is the potential for market conditions or your personal circumstances to change during this time.

At least four months prior to the anticipated settlement, revisit your application, and make sure your ability to service the loan is still good before deciding who is the most suitable lender.

When the application is submitted and processed, the completed property is valued, loan documents are issued, then settlement can occur.

In terms of LVR – what is required?

For an expat, 80% is the maximum LVR achievable; however, It could potentially be reduced to 70% depending on the lender’s policy for using foreign income.

Risks to watch out for

Generally speaking, as an expat, you can get finance if you meet the usual criteria, such as having a good credit history, a stable income and meet serviceability. Issues can occur; however, when you are earning money in a currency that might not be considered as stable as the Aussie Dollar.

For off-the-plan finance, each lender will only finance a certain number of units per development. As an expat your more limited in your choice of lender, therefore it’s important to have your application submitted and approved early. You should also arrange for the final valuation to occur on the first day that the valuers are allowed in, to ensure that you are one of the first in line to gain formal approval.

Also, it’s important to note that when you purchase an off-the-plan property you pay a 10% deposit, therefore if you cannot settle, your deposit is at risk.

Protect yourself through careful planning

It’s sensible planning to ensure that you have a buffer of cash available in case the valuation comes in lower than you had previously anticipated, or at the very least have some equity available in another property, so you can still settle on the purchase.

A great way to get financially ahead

Living the life of an expat can often be a great way to get ahead financially, and it is the perfect opportunity to put some of that additional income to work by investing in property.

If you are well prepared and understand the process, getting finance for an off-the-plan property shouldn’t be a problem as an expat.

One of the most powerful things about investing in property is your ability to leverage the equity in your existing home or investment property.

One of the most powerful things about investing in property is your ability to leverage the equity in your existing home or investment property.

When you start to use that leverage, you can quickly take one property and build that into a portfolio that can set you up and allow you to achieve your financial goals.

If you already own an existing Australian property, you may have equity available which can be used towards purchasing another property without the need to put in your own cash. This is particularly beneficial for investors as they can maximise their investment by negatively gearing the property, leaving their cash available for other investments.

So how can potential investors leverage their current equity to purchase their next investment property?

Understanding the Loan-to-Value Ratio (LVR)

Equity is the current value of your property minus the outstanding loan. The banks will lend up to 80% of this amount without the need to pay Lenders Mortgage Insurance or up to 90% with Lenders Mortgage Insurance.

Risks to watch out for

As you would have a higher loan on the property, this, in turn, means that your annual holding costs on the property are higher than if you put in the cash deposit yourself.

To minimise this risk, you should ensure you are purchasing a quality property that you feel will increase in value each year by more than the annual holding cost of the property.

An example

John owns a property worth $450,000 and currently has a loan of $250,000 over the property. He doesn’t want to incur Lenders Mortgage Insurance so would like to keep his maximum loan to value ratio at 80%. His equity is calculated is as follows:

$450,000 ( value of the existing property) x 80% = $360,000 maximum loan available on existing property.

$360,000 ( maximum loan) – $250,000 (existing loan) = $110,000 equity available to use towards a new purchase.

The $110,000 in equity then needs to cover the 20% deposit on a new property, as well as roughly 5% for the costs of purchase such as stamp duty and legal fees.

In this case, John was able to purchase a property for $440,000 using the $110,000 in equity from his existing property – $88,000 of this went towards the 20% deposit and the remaining $22,000 covered his costs of purchase.

He then also had a new loan of $352,000 secured against the new property so he did not need to contribute any of his own cash to this purchase.

As the value of both of his homes continues to grow over time, John will be able to access that additional equity to continue to build his property portfolio. The more quality properties he owns, the faster that equity adds up.

The power of leverage

It really doesn’t take long to build yourself a very powerful property portfolio when you start leveraging your existing equity.

Life can present unexpected challenges and financial difficulties are a common concern. So, what can a mortgage broker do for clients who say they’re struggling?

A mortgage broker helps borrowers connect with lenders and seeks out the best lender for the borrower’s financial situation.

First and foremost, it’s essential to foster open and empathetic communication with clients. When clients express their financial struggles, it’s a sign they trust us and see us as a valuable resource. Listening attentively to their concerns is the first step in offering support.

Brokers can often be the initial point of contact for clients grappling with financial difficulties. Clients typically approach brokers with concerns about rising repayments and the challenges they face in meeting them.

Validating their concerns helps build trust and creates a safe space for honest discussions. To provide the best guidance, it’s crucial to review their financial situation thoroughly and trust plays a big part in this. Gathering all relevant financial information, including income, expenses and outstanding debts allows us to identify the root causes of their struggles.

Cracking the code with lenders

Brokers often face the challenge of discerning their obligations and differentiating them from the lender’s responsibilities. Under the National Credit Code, lenders are required to consider hardship arrangements when borrowers apply and state their inability to meet credit contract obligations, however, this section of the Code is broad and open to interpretation.

While lenders must determine when a hardship notice has been given, brokers play a pivotal role in recognising signs of hardship and guiding clients on how to communicate effectively with their lender.

Brokers serve as the main point of contact for many borrowers, and their ability to recognise signs of hardship and advise clients on how to approach lenders is paramount.

They have strong relationships with multiple lenders and can use these connections to negotiate on behalf of the client.

Lenders have a wide array of instruments at their disposal; depending on the circumstances, there may be various mortgage options available to alleviate their financial burden. This could involve refinancing to secure a lower interest rate, consolidating debts, extending the loan term to reduce monthly payments, payment holidays, temporary interest reductions, extending loan terms and looking at hardship applications with the lender.

Overcoming financial hardship

With the mounting pressures on consumers and small businesses due to rising interest rates and the soaring cost of living, the need for hardship assistance has become increasingly prevalent. Some clients may be unable to reprice or switch lenders, leading to potential financial hardship scenarios.

The struggles faced by Australian borrowers have garnered significant attention. A recent study by Roy Morgan revealed over 1.5 million borrowers are at risk of mortgage stress, with nearly a quarter of homebuyers allocating half their income to mortgage payments.

This precarious situation has prompted two thirds of homebuyers to request that their credit providers monitor their financial well-being to prevent payment defaults.

Financial hardship, however, should not be confused with occasional lapses, short-term unforeseen expenses, or temporary payment timing issues. It typically arises when clients experience significant life events such as job loss, illness, income reduction, relationship breakdown, or business failure, making it challenging to meet financial commitments.

In challenging times, it is a mortgage broker’s responsibility to stand by their clients, offering not just financial solutions but also unwavering support.

Collaborating with a financial planner can be beneficial for clients facing financial challenges. They can create a realistic budget and financial plan tailored to their specific needs, helping clients regain control of their finances.

I firmly believe in empowering my clients with financial knowledge. Educating them about responsible financial practices and the importance of maintaining a good credit score can prevent future challenges.

Interest rates add to burden

In most cases, when the RBA hikes the official cash rate, banks and lenders are quick to follow suit raising the rates of variable rate home loan borrowers.

The 29 per cent of borrowers in mortgage stress, the highest since May 2008, reflects the repercussions of the Reserve Bank’s interest rate hikes throughout this year.

The number of households deemed “at risk” of mortgage stress has swelled by a staggering 642,000 this year. Michele Levine, CEO of Roy Morgan, warns that further interest rate hikes could exacerbate this crisis, possibly inching closer to the record high of 35.6 per cent observed in May 2008 during the Global Financial Crisis.

If you find yourself in this situation, be sure to reach out for professional assistance to prevent matters deteriorating unnecessarily or excessively.