Experts are divided on the likelihood of an RBA interest rate cut in the next few months, but all agree borrowers are banking on it.

With inflation figures having fallen to the lowest level in almost two years, even the prospect of a cash rate rise in 2024 is up for debate.

Mortgage broker Helen Avis (pictured above left), director of Specialist Mortgage, said her clients would breathe a sigh of relief if there were no further rate hikes over the next 12 months, with many feeling the pinch of the rising cost of living.

“Many buyers are concerned about the prospect of rate increases and their ability to service their mortgage,” Avis said.

“This is particularly evident within the first home buyer market who are often shopping at their maximum borrowing capacity, investors using property as collateral to secure finance, and our overseas clients who are often faced with higher rates than Australian residents.”

High Hopes That Interest Rates Won’t Rise In First Half

Avis said her clients are hopeful rates will remain on hold for the next six months, with most believing they won’t see rate cuts until 2025.

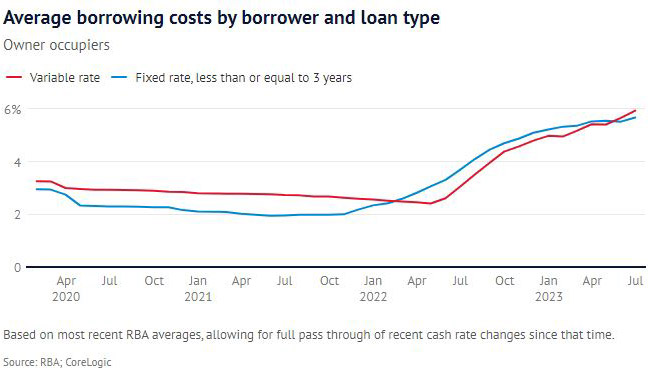

“Nearly all of our clients are choosing variable loans over fixed rates. This is in significate contrast to the height of the pandemic when borrowers were opting for low-rate fixed mortgages.”

Avis said clients’ sentiment towards the property market was still positive, “but they are approaching it with a little more caution”.

She said many clients were factoring in potential rate increases, often looking at property well under their maximum borrowing capacity.

Now is a great time for borrowers to take advantage of the competitive rate market.

“Our brokers are negotiating aggressively with our clients’ existing lenders to get the best variable rates, which is often preferable compared to switching to a new loan provider,” Avis said.

Buyers Need To Spend Within Means

aussieproperty.com buyers agent Julie Kelley said rate relief would instil confidence in the property market.

“As we all know taking on too much debt can lead to unnecessary stress; I always advise clients to shop in their comfort zone,” Kelley said.

“In such a competitive market, I understand buyers can feel frustrated by not being able to secure their dream home due to budget constraints, and they may feel pressured by selling agents to quickly submit an offer above their initial budget. But it’s important not to let emotions take over.

“We always advise our buyers that are considering pushing their borrowing limits to first speak with their mortgage broker and factor in all increased costs such as stamp duty, repayments and LMI before submitting an offer on a property”.

Financial comparison site Mozo’s money expert Rachel Wastell (pictured above centre), money expert at financial comparison site Mozo, said mortgage holders would welcome a rate cut, no matter how small.

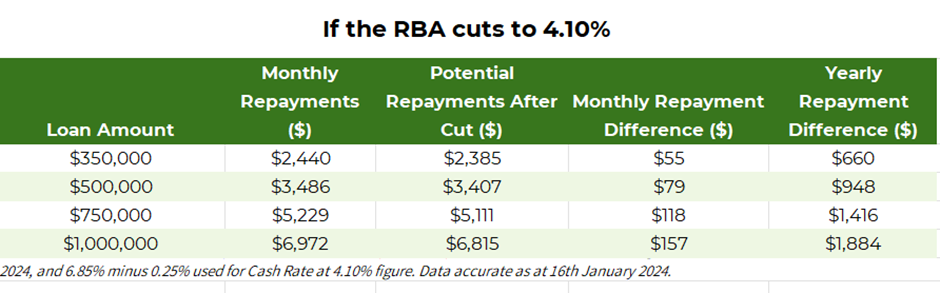

Mozo analysis shows someone with a $1 million mortgage, following a rate cut to 4.1%, will have an extra $157 a month in their pocket, equating to $1,884 a year based on the variable rate staying the same (see Mozo data below).

Source: Mozo

“I think borrowers will be cheering when a rate cut comes through,” Wastell said. “After one of the most aggressive rate hiking cycles since the early 1990s news about rates has unfortunately been quite doom and gloom.”

RBA On Track To Meet Inflation Goal?

Wastell said a rate cut will likely give borrowers some hope that the RBA is on track to meet their inflation target, and that more rate cuts could be on the horizon.

“In a cost-of-living crisis every cent counts; $100 more a month might not seem like much, but for those mortgage holders who have now resorted to credit cards or buy now pay later services to cover their everyday expenses,” Wastell said.

“That $100 could be the difference between clearing those monthly balances or being in the red.”

Despite what borrowers want, Wastell said a rate cut in the next few months was unlikely, as the unemployment rate was holding steady and inflation in services, particularly insurance, was still high.

“Later in the year, if there are no further rate hikes, and the CPI data for the June quarter shows we’re much closer to the RBA’s target of 2% to 3% we will probably see a rate cut or two, but I think it’s important homeowners don’t count their chickens before they hatch.”

Experts Predict February Cash Rate Pause

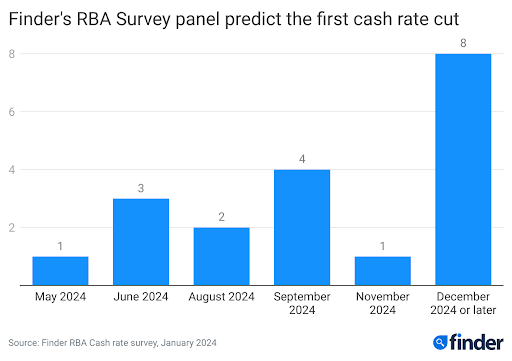

In this month’s Finder RBA Cash Rate Survey, 19 experts and economists weighed in on future cash rate moves and almost all of the experts, 89%, said the RBA would hold the cash rate at 4.35% in February.

Head of consumer research at Finder Graham Cooke (pictured above right) said many Australians were in urgent need of reprieve following the last rate rise in November.

“Homeowners are still reeling from 13 rate hikes in the last two years,” Cooke said.

“Our data shows a staggering 40% struggled to pay their mortgage in December. Even though inflation is falling, I expect the RBA will hold the cash rate for most, if not all of 2024.”

While one in three Finder panellists predict a cash rate cut by at least August this year, almost half, or 40%, don’t expect the RBA to start cutting rates until December 2024 or later.

The majority of Finder experts, or 71%, said they expected the cost-of-living crisis to ease eventually in 2024.

“While the gauge remains in the extreme range, it’s likely that this will be where the cost-of-living pressure peaks,” Cooke said. “We expect to see some relief on the horizon, and with a little luck the pressure will reduce slowly over many months.”

Earlier this month, Bank of Queensland chief economist Peter Munckton said talk of rate increases by the RBA this year were “in the rear mirror” and said the big question for 2024 is when would interest rates start to fall.

Property prices in Perth are defying a gradual easing in the rate of capital growth being seen elsewhere in the nation and dominating lists of the nation’s hottest real estate markets.

If you bought property anywhere in Australia other than Perth, then your home is not among the 10 fastest rising markets in the country.

All 10 suburbs where prices have risen the fastest in 2024 are in the West Australian capital, and one affordable part of the city has dominated within that list.

The working class City of Kwinana stands atop the national podium, with its suburbs of Medina, Parmelia and Orelia the three fastest growing property markets in the nation and Calista coming in sixth overall.

Top 10 fastest rising property markets for 2024

All of the suburbs in the PropTrack top 10 were relatively affordable places to buy.

South Australia came closest to competing with Perth for price growth in 2024 to date, with top ranked Elizabeth Park having house price growth of 17.1 per cent, still 6 per cent below Perth’s tenth placed Coolbellup.

With the exception of SA’s sixth placed West Lakes’ median house price of $1,074,000, eight of the other nine had even more affordable values than Perth’s top 10, being under $550,000.

Highlighting Melbourne’s stable but subdued property market throughout 2024, the top ten suburbs delivered capital growth between 6.7 per cent (Rutherglen) and 3.6 per cent (Kyabram).

CoreLogic’s daily home value index has seen a marked easing in the rolling four week change, with national values rising just 0.5 per cent over the four weeks to 18 July, down from a 0.7 per cent rise seen the same time last month.

The recent slowdown is notably stronger across more expensive markets and property types with house values and values in Sydney recording the most noticeable easing.

Melbourne and Hobart are the only capitals recording falling values, with high stock levels placing downside pressure on values.

Perth continues to lead the pack, with a rolling 28-day increase of 1.8 per cent, followed by Adelaide (1.7 per cent) and Brisbane (1.0 per cent). The trend for softer growth is less apparent in these cities.

Perth is the property story of 2024

But the real story of capital growth in Australia at the moment belongs to one boom city.

The median Perth house sale price set a new record month after month over the financial year, and is now $665,000 for the year to June 2024. This is 18.8 per cent higher than at the end of the 2022-23 financial year.

The median unit sale price increased 11.3 per cent year-on-year to reach $445,000, according to REIWA, just $5,000 below the previous record of $450,000 in 2014.

REIWA CEO Cath Hart said she expects this record to be broken in the next few months.

Viveash, which recorded the highest price growth for houses, had its median house sale price increase 40.9 per cent over 2023-24 to $620,000, highlighting the rush to mid and lower priced property.

“Affordability remains a focus for buyers and this is reflected in the makeup of the financial year’s top 10 suburbs for house price growth,” Ms Hart said.

“The majority have a median sale price below Perth’s median and only two have a median house sale price over $1million.

“It indicates strong demand for suburbs in more affordable price brackets.

“Demand is also reflected in their selling times, with the more affordable suburbs on the list having a median time on market that is nearly half that of the suburbs with a median over $1 million.”

In the unit market, Cottesloe was the top performer, with its median sale price rising 50.9 per cent to $1,200,000. Bayswater recorded growth of more than 40 per cent.

Like the top 10 list for house price growth, seven of the suburbs in the top 10 for units have a median sale price under Perth’s median unit price.

“While the unit market was slower to respond to market conditions over most of 2023, in 2024 we have seen demand and price growth accelerate,” Ms Hart said.

“The overall demand for property, and particularly the strong motivation to exit the challenging rental market, has seen demand for units increase. Units are generally more affordable than houses, which helps people put a foot on the property ladder in a rising market. This is helping drive price growth in the unit market.”

This financial year saw houses sell incredibly quickly, with a new monthly record of a median eight days on market set in October and November.

Which suburbs have the fastest rising property prices in Australia so far in 2024?

All 10 suburbs where prices have risen the fastest in 2024 are in the West Australian capital, and one affordable part of the city has dominated within that list. The working class City of Kwinana stands atop the national podium, with its suburbs of Medina, Parmelia and Orelia the three fastest growing property markets in the nation and Calista coming in sixth overall.

How fast are properties selling in Perth?

The 2023/24 financial year saw houses sell incredibly quickly, with a new monthly record of a median eight days on market set in October and November 2023.

Where are unit prices rising fastest in Perth?

In the unit market, Cottesloe was the top performer, with its median sale price rising 50.9 per cent to $1,200,000. Bayswater recorded growth of more than 40 per cent. Seven of the suburbs in the top 10 for units have a median sale price under Perth’s median unit price.

The Mortgage and Finance Association of Australia named Ms Avis Residential Finance Broker WA 2024, marking her second time atop this podium.

The mortgage and finance broking industry in Western Australia honoured this year’s achievers at the 2024 MFAA State Excellence Awards, with Helen Avis, Director of Finance, Specialist Mortgage, taking out one the most coveted awards for the second time.

The Mortgage and Finance Association of Australia named Ms Avis Residential Finance Broker WA 2024.

Ms Avis said the MFAA Excellence Awards are renowned for celebrating the highest standards of professionalism, integrity, and innovation in this finance field.

“This recognition is a significant milestone in my career, and I am deeply grateful for the acknowledgment of my hard work and dedication within the mortgage and finance industry,” Ms Avis said.

“Winning this award is not just a personal achievement but also a testament to the incredible team and clients I have had the privilege to work with.”

Ms Avis added that the award highlighted the significant contributions of women in the mortgage industry.

“It is a powerful reminder that with determination, passion, and the right support, we can achieve great heights.

“I hope this recognition inspires other women in our industry to pursue their goals with confidence and resilience.”

All Western Australia MFAA State Excellence Awards winners are finalists in their respective categories at the MFAA National Excellence Awards which will be held in Melbourne on Thursday 25 July following the MFAA National Conference.

Advice for borrowers struggling with deposit

While it’s often said a 20 per cent deposit is needed to qualify for a home loan, a significant number of borrowers are securing mortgages with smaller deposits, according to the latest data from APRA, the banking regulator.

Ms Avis said it was still possible to buy a property with a small deposit and could offer advice on structuring a loan application correctly.

In the March 2024 quarter, 31.0 per cent of new home loans (by value) had deposits of less than 20 per cent, while 6.2 per cent of new loans had deposits of less than 10 per cent.

“While more than three in 10 borrowers are taking out loans with deposits under 20 per cent, these figures are relatively low by historical standards.

“Back in December 2020, for example, 41.7 per cent of new loans had deposits of less than 20 per cent, while 11.3 per cent had deposits of less than 10 per cent.

“This illustrates how banks have tightened their lending standards, to ensure borrowers don’t take on an excessive amount of debt, yet it’s still possible to buy a property with a small deposit,” Ms Avis said.

Generally, these buyers will need to pay lender’s mortgage insurance (LMI) when purchasing a property with a deposit of less than 15-20 per cent.

Full list of MFAA winners

Residential Finance Broker Award

Helen Avis, Specialist Mortgage

Regional Finance Broker Award

Jasmine Bunter, Loan Market Geraldton

Business Development Manager Award – Aggregator

Renee Dewar, Loan Market

Business Development Manager Award – Lender/Support Service Provider

Petra Rebeira, Suncorp Bank

Commercial & Equipment Finance Broker Award

Steven McCaughey, Financewest Solutions

Community Champion Award

TAG Finance Australia

Customer Service Award – Business

Loan Market Ellenbrook

Customer Service Award – Individual

Nicole Williams, For Finance Sake

Diversified Business Award

TAG Finance Australia

Finance Broker Business Award

Loan Market Bal & Associates

Fintech Lender Award

ubank

Loan Administrator Award

Gracen Woodcock, Loan Market Geraldton

Major Lender Award

Macquarie Bank

Mutual/Credit Union Lender Award

P&N Bank

Newcomer Award

Kurtis Grace, Whiteroom Finance Goldfields

Non-Major Lender Award

Bankwest

Specialty Lender Award

Pepper Money

Young Professional Award

Robert Flynn, Vorteil Financial Group

Article Q&A

Can I buy property without a large deposit?

In the March 2024 quarter, 31.0 per cent of new home loans (by value) had deposits of less than 20 per cent, while 6.2 per cent of new loans had deposits of less than 10 per cent.

By refusing to make any major changes that will shift the dial on the housing crisis, the government has unwittingly guaranteed that property prices will keep rising, argues a leading national commentator.

A leading national commentator says the government has unintentionally created boom conditions for property investors.

By failing to make any significant structural changes that will address the lack of housing supply, Steve Douglas, Chairman of SMATS Group and Managing Director of Australasian Taxation Services and aussieproperty.com, said the next few years would deliver those getting into the property market now with years of strong gains.

By opting to continue with an extension of existing housing funding arrangements, only tinkering with rental support, and giving away one-off band-aid power bill credits, the government had missed an opportunity to really address the shortage of housing that is driving property prices higher.

“Governments are still greedily pulling in massive stamp duty taxes from the Australian public but are doing nothing to alleviate the pressure on the building industry, therefore ensuring the ambitious (1.2 million homes in five years) building target remains fanciful,” Mr Douglas said.

The head of the company that looks after more Australian landlords than any other accounting firm in the world said the inevitable result would be continued property price rises and huge opportunities for property investors.

“By dragging their heels, the Government has unknowingly created opportunity for property investors.

“If you’ve been procrastinating, now is the time to get into the property market or build on that existing real estate portfolio.

“There is nothing in the federal budget (released 14 May) that will put even a minor dent in the big issue impacting property prices – the lack of new supply.”

Investors discouraged from providing rental stock

Australia’s rental market remains extremely tight, despite a slight uptick in the vacancy rate.

PropTrack data released Thursday (16 May) shows that the national vacancy rate edged up slightly this month to 1.21 per cent, still way short of the 2 to 3 per cent band regarded as a balanced rental market.

Adelaide recorded the lowest vacancy rate of any market in April, with just 0.96 per cent of rental properties sitting vacant. Perth crept above the 1 per cent mark for the first time in almost two years, improving on Brisbane’s 1.02 per cent. Melbourne’s vacancy rate slipped back to 1.23 per cent, while Sydney improved slightly to 1.3 per cent.

With rents still rising despite the slowly improving vacancy rate, the budget’s 10 per cent increase in the maximum Commonwealth Rent Assistance payment, a supplemental payment for renters receiving government benefits, is unlikely to shift the dial in addressing the rental crisis.

Successive governments have failed to deliver any big ideas that could offer renters hope.

Mr Douglas pointed to the abundance of rental stock sitting in front of our collective noses that was being underutilised.

“For too long they have demonised and penalised property investors and landlords and that is a massive factor in why there is a shortage of rental properties, in combination with natural population growth, rising affluence and migration.

“Government should be looking to mobilise individuals in the fight against the housing affordability and rental crises.

He singled out unused rooms in millions of homes around the country as one source of a potential solution.

“If the process of letting out a room was taxed less, if at all, and made simpler, the housing situation could be massively improved almost overnight.”

He proposed a tax regime whereby owners of properties registered their spare room as being rented out, paid no tax for three years and then had the option to continue or not when that lapsed.

“This would give the market the time to catch up on the building and delivery of homes and social housing in the pipeline.

“It would cost the government next to nothing and as a short-term measure would release hundreds of thousands of rooms that are sitting empty, while at the same time help those households address their cost of living issues with some extra revenue.”

Landlords not the enemy

Mr Douglas said that landlords, whether based in Australia or overseas, had been demonised for too long.

“Overseas owners (and expats) that have had the capital gains tax (CGT) discount removed, and expats with their principal residence CGT exemption taken off them if they sell while living abroad, all go towards making it less likely they will sell into the market to relieve demand pressure.

“Then the entry costs of stamp duty (normal and extra foreign buyer duty) plus GST (foreigners have to buy new, expats often do too) combine with higher CGT costs to make it less viable or attractive to invest.

“The fact is that many landlords face a net holding cost (negative gearing) when owning a property with a mortgage, so they are in fact subsidising the tenant in the hope the property value will rise.

“While prices have risen in many markets, there is risk.

“For most apartment buyers in Melbourne they have only seen property values decline or stagnate for a decade, while for many property owners in Queensland and Western Australia it has been many years without capital growth and only in the last year or two have prices start to lift.”

He added tenancy laws across the country have made it increasingly difficult for landlords to have tenants respect their property, or to recover justifiable costs from bonds.

“If this or any government is serious about address the housing crisis, it needs to do more than hand out $300 energy credits and renew existing policies; it needs to think bigger and make significant structural changes that will encourage homeowners and investors to increase supply quickly.”

Article Q&A

Will the federal budget impact property prices?

By failing to make any significant structural changes that will address the lack of housing supply, Steve Douglas, Managing Director of aussieproperty.com, said the next few years would deliver those getting into the property market now with years of strong gains.

What is the vacancy rate in Australia?

PropTrack data released Thursday (16 May 2024) shows that the national rental vacancy rate edged up slightly this month to 1.21 per cent, still way short of the band of 2 to 3 per cent regarded as a balanced rental market.

How can the housing crisis be tackled?

Steve Douglas, Chairman of SMATS Group, pointed to the abundance of rental stock sitting in front of our collective noses that was being underutilised to tackle the housing crisis, saying Government should be looking to mobilise individuals in the fight against the housing affordability and rental crises. He singled out unused rooms in millions of homes around the country as one source of a potential solution.

The Reserve Bank Governor Philip Lowe has used his final monthly meeting to leave interest rates on hold for a third successive month.

The RBA Board decided to leave the cash rate target unchanged at 4.10 per cent, pointing to subsiding inflation, broad economic uncertainty and earlier interest rate hikes still working their way through the economy.

The decision to hold came as little surprise, with all but one of 38 panellists from Finder’s RBA Cash Rate Survey believing the RBA would hold the cash rate steady in September.

Mr Lowe’s final Monetary Policy Decision said the Australian economy is experiencing a period of below-trend growth that is expected to continue for a while.

“High inflation is weighing on people’s real incomes and household consumption growth is weak, as is dwelling investment,” he said.

“Notwithstanding this, conditions in the labour market remain tight, although they have eased a little.

“Given that the economy and employment are forecast to grow below trend, the unemployment rate is expected to rise gradually to around 4.5 per cent late next year.

“Wages growth has picked up over the past year but is still consistent with the inflation target, provided that productivity growth picks up.”

He added that there is increased uncertainty around the outlook for the Chinese economy due to ongoing stresses in the property market there.

Unlike previous monthly rates announcements, Mr Lowe on Tuesday (5 September) issued a softer than usual notice that more rate hikes may be necessary to curb inflation.

“Some further tightening of monetary policy may be required to ensure that inflation returns to target in a reasonable timeframe, but that will continue to depend upon the data and the evolving assessment of risks,” he said, tempering his usual bullish sentiment with the ‘but’ on this occasion.

Little prospect of a rate cut

The rate hold is relatively good news for borrowers but the prospects of an imminent rate cut remain slim.

Economist Saul Eslake, of Corinna Economic Advisory, said the latest monthly CPI data for July show a further and welcome decline in headline inflation to 4.9 per cent, the lowest since February 2022, but still well above the RBA’s target range of 2 to 3 per cent.

“Underlying inflation also fell, but only to 5.6 per cent, even further above the target range, so there’s no need to tighten policy further but nor any reason to anticipate any reductions in interest rates any time soon,” he said.

Former Labor Government trade minister, Craig Emerson, of Emerson Economics, concurred, saying, “The RBA will consider it too early to ease and will maintain its pause position.”

David Robertson, Chief Economist, Bendigo Bank was less optimistic, saying a rate hike was more likely than a rate in coming months.

“The RBA appears comfortable holding the cash rate at 4.1 per cent ahead of the next quarterly CPI report out on 25 October 25.

“Another hike to 4.35 per cent remains the risk, as core services inflation remains stubbornly high, but not until November at the earliest.”

Many believe the cash rate will hold at 4.1 per cent now until the new year and will start to ease back, back to 3 percentage points range by the end of 2024 according to CBA’s Senior Economist Belinda Allen and Economist Stephen Wu. NAB economists believe there will likely be one more hike this year and Westpac’s Chief Economist Bill Evans believes we won’t see rate cuts till this time next year.

What does the RBA decision mean for property market?

The 29.2 per cent of borrowers deemed to be in mortgage stress remains notably lower than the levels witnessed during the financial turmoil of a decade or more ago when mortgage holders in stress reached a peak of 35.6 per cent in mid-2008.

But more concerning is the surge in the number of mortgage holders considered extremely at risk, which has now climbed to 1,017,000 (20.3 per cent). This figure significantly exceeds the long-term average of 15.4 per cent over the last 15 years and reflects an increase of more than 470,000 mortgage holders compared to a year ago, marking a 7.6 per cent rise.

Helen Avis, Director of Finance at Specialist Mortgage, said borrowers were refinancing in record numbers and increasingly turning towards mortgage brokers in an attempt to alleviate financial pressures.

Ms Avis said she expected the RBA to hold off on any further moves for several months as the current raft of increases gradually take effect.

“The majority of home price falls recorded last year have been reversed in 2023, with August marking the eight consecutive month of national home price growth. Strong demand and limited supply have offset the impact of rate rises that continued this year.

Eleanor Creagh, PropTrack Senior Economist, said subsiding momentum in inflation and consumer spending have eased pressure on the RBA to continue lifting interest rates as it tries to avoid a recession while taming inflation.

“The decision by the Reserve Bank to continue holding the cash rate steady in September is likely to maintain both buyer and seller confidence as the spring selling season begins, with home prices likely to continue lifting in the period ahead.

“The majority of home price falls recorded last year have been reversed in 2023, with August marking the eight consecutive month of national home price growth.

“Strong demand and limited supply have offset the impact of rate rises that continued this year.”

Rich Harvey, CEO, Propertybuyer, said as overstretched investors sell it could be a good time to enter the property market.

“Inflation is decreasing slowly as households are finally feeling the real pinch of significantly higher mortgage repayments, so there’s likely to be many discussions around the dinner table as to how households will adjust spending patterns to cope with higher rates.

“Discretionary spending is down and likely to stay low for next six months, and likely to see some investors offload investment properties if the drag on their budget is too strong.

“All this provides good buying opportunities for savvy buyers with financial means to secure more property,” Mr Harvey said.

Interest rates being pushed up by rampant inflation are forcing mortgagees and prospective buyers to find new ways of servicing debt.

Borrowers are increasingly turning to refinancing and pairing up with friends and family to overcome the weighty burden of rapidly rising interest rates.

NAB research released Friday (27 January) reveals that 40 per cent of young Australians are considering buying a property with someone other than a romantic partner.

Outside of dropping their price range, buying with another person tops the list of compromises Aussies aged 18 to 29 are prepared to make to get into the market.

Almost a third are willing to buy and rent the property out initially, while 20 per cent say they’re up for moving into a share house.

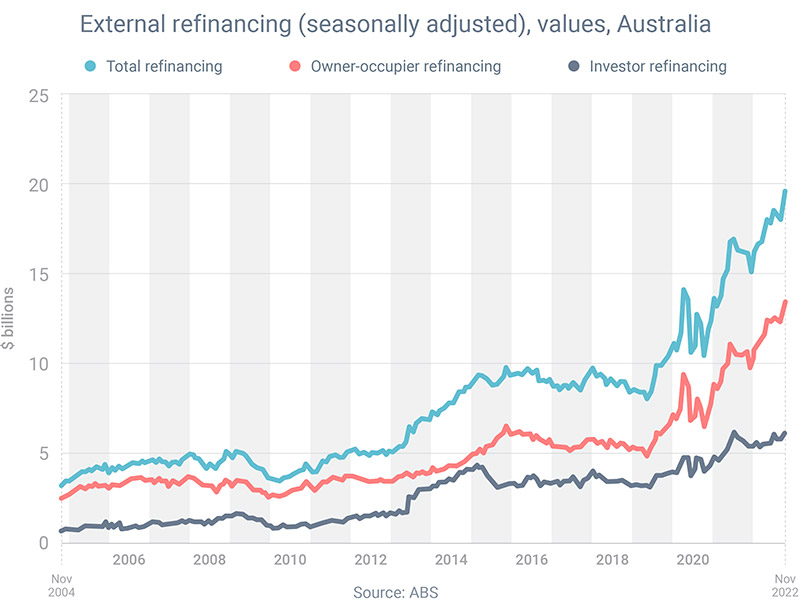

For those already paying off a mortgage, record numbers are refinancing in the quest for a better deal.

Borrowers refinanced a record $19.5 billion of loans in November, the most recent month for which we have data, according to the Reserve Bank of Australia (RBA).

By way of comparison, that was 20.4% higher than the year before and 88.2% higher than two years before.

Helen Avis, Director of Finance, Specialist Mortgage, said the RBA has hinted that at least one more rate rise is coming as it wrestles with inflation that has taken off, recently hitting 7.3 per cent.

“In December, it said it wanted to ‘return inflation to the 2-3% target range over time’ and would ‘do what is necessary to achieve that outcome’, by which it means increasing the official cash rate yet again.”

“So if it’s been a while since you took out your home loan, now would be a good time to think about refinancing,” Ms Avis said.

Borrowers getting creative

NAB Executive (Home Ownership), Andy Kerr, said younger people are getting creative when it comes to making their property dreams come true.

“Younger Australians aren’t letting meeting a partner or getting married later in life hold them back from owning a home now.

“People are definitely looking at their options and casting the net wider when thinking about who they could buy with,” Mr Kerr said.

“Rentvesting – purchasing in one location and then renting in another – is another trend that is creeping up in popularity.

“Interestingly, our data shows that first home buyers aren’t being deterred from entering the property market, despite the market softening overall and rising cost-of-living.

“Buyers are just thinking outside of the box to make it happen.”

The NAB research also found that the most common compromise (41 per cent) buyers of all ages were willing to make was the amount they’re willing to spend.

About one in three said they would trade off the size of the land, garden or outdoor space (31 per cent), while about 28 per cent would give up their preferred location.

One in 10 aren’t willing to budge at all on their wish list.

Mr Kerr said regardless of who you were buying with it’s important that you talk about how you’ll jointly save for a deposit, agree on the property and meet ongoing costs.

“As buying a home is the biggest purchase most of us will make, it’s also worth considering getting a solicitor involved for additional comfort,” he said.

Undeterred by property prices in Melbourne and Sydney coming off the boil or the threat of higher interest rates, expatriate Australians are continuing to snap up prestige properties.

Undeterred by property prices in Melbourne and Sydney coming off the boil or the threat of higher interest rates, expatriate Australians are continuing to snap up properties priced considerably higher than median city values.

Helen Avis, the SMATS Group Director of Finance, said the expatriates that had recently returned to Australia were moving from rentals into their own properties and could afford prestige real estate in highly sought-after areas.

“The $2 million to $4 million bracket has been very active as expats plan their eventual return and want to buy the future home, or move from their temporary rentals having recently returned,” Ms Avis said.

The recently-name finalist in the national Better Business Awards, in Best Residential Broker category, said she had also seen a lot of buyers targeting regional areas, holiday locations and the holiday home market.

“There’s very little investor or expatriate interest in CBD city apartments – that market has dried up – but there is still a lot of demand for luxury apartments as well as houses in the higher-priced suburbs.”

The first quarter of the year has seen Australian dwelling values rise by 2.4 per cent, less than half the pace of the same period last year.

But expatriates seeking a home rather than an investment can afford to pay the premiums that two years of rapid price growth has delivered and are not phased at the prospect of higher interest rates.

Interesting times

The big four bank economists are forecasting official cash rate hikes could begin between June and September.

Not waiting for the Reserve Bank of Australia, Australia’s third and fourth largest banks, NAB and ANZ, on Friday (1 April) hiked fixed rates by up to 0.40 percentage points.

“We have seen all banks raise fixed rates so many times in the last six months and I expect the RBA will raise rates from June,” Ms Avis said.

Helen Avis, finalist in the Better Business Awards

“I don’t think they want to raise them and then continue to raise them regularly, so it should be a slow progression, but the market is expecting interest rates to rise.

“All borrowers are assessed at 3 per cent over the benchmark rate, so it shouldn’t put stress on people’s ability to maintain their loans.

“With the borders just opening back up, we should have a two-year backlog of intended migrants, expats and international students start to push up the rental market as well as CBD sales.

“The intended migrants will likely rent to start off with, but most will likely want to buy, so demand will again be strengthened.”

Ms Avis said SMATS Group’s aussieproperty.com had clients looking at all states’ markets but Queensland was generating the most interest.

Sydney, Melbourne, Perth and the West Australian southwest were also on the radar of returning expatriates, she said.

The Better Business Awards seek to champion the leading players of the broking industry in each state and territory of Australia.

Reaching the finalists stage is regarded as an incredible achievement across the Australian broking industry, showcasing the depth of dedication and commitment each individual and team brings to advancing the industry.

Ms Avis said she was humbled to be recognised and proud to be named as a finalist. Winners are announced at a ceremony on 19 May.

Specialist Mortgage director Helen Avis settled more than $25 million in loans in July, as returning expats and those looking to move to lifestyle locations underpinned a record quarterly performance for mortgage brokers across the country.

Ms Avis completed 49 settlements collectively worth $25.03 million over the month, with that total eclipsing the next highest Australia-based Specialist Finance Group broker by more than $5 million.

Specialist Mortgage which operates in Sydney, Melbourne and Perth as well as international cities such as Singapore, Hong Kong, New York, Dubai and London aggregates to SFG.

The July total adds to a long list of achievements for Ms Avis, including winning St Georges Bank’s Top Flame Broker award in 2013 and 2014, and being named SFG’s International Broker of the year in 2016, 2017, 2018 and 2019.

Ms Avis said a big proportion of the July loans went to returning expats seeking a home in Australia to ride out the pandemic.

More than 500,000 Australians have returned from international cities since the onset of COVID-19, with that influx a big contributing factor to the meteoric rise in housing values over the past 12 months.

“The market is hugely competitive at the moment, and with the appeal of Australia being a safe haven from COVID-19, I’ve seen high demand for family homes being sought in Queensland and New South Wales,” Ms Avis said.

“Clients are looking at options for where to stay when they make it out of quarantine, and somewhere comfortable that they’ll be in for the future.”

One of those expats was Stewart Duncan, who heralded Ms Avis’ expertise in the complicated process of signing and notarising crucial documents for an offshore client.

“It was all a bit complex for a layman, but Helen navigated everything on my behalf and explained the pros and cons of different scenarios,” Mr Duncan said.

“I felt very comfortable being able to reach out to Helen at any time and get a quick response, especially not being in Australia with time differences and trying to get something in a timely manner.

“Doing business transactions is completely different to finding a house for the family and the support from having someone on the ground was immeasurable.”

Mr Duncan said he was extremely satisfied with the rates and the terms of the loan provided by Ms Avis.

“The process requires somebody familiar with the expatriate financial packages and terms and conditions to be able to explain them to the banks,” he said.

Another happy client was Peter, who recently returned to Australia from Singapore and purchased a family home on Sydney’s Lower North Shore and refinanced an investment property.

“We found dealing with Helen and her team a very positive experience,” Peter said.

“From quickly ascertaining our requirements and forwarding a number of attractive options from several lenders, we were able to work with Helen quickly from pre-approval to settlement.”

The strong monthly performance came in an environment of elevated demand for housing finance, with the value of new settlements in the second quarter of the year up 47.25 per cent compared to the same time in 2020.

Data released by the Mortgage & Finance Association of Australia showed there was more than $77.75 billion in new lending facilitated by brokers in the three months to the end of June, up $24.95 billion on the previous quarter.

The second quarter performance represented the biggest observed result for a June quarter and was $13.65 billion more than the previous record three month period since the MFAA commissioned CoreLogic to provide the data in 2013.

SMATS Group executive chairman Steve Douglas, who heads up the main holding entity of Specialist Mortgage, said 2021 had been one of the busiest he’d been involved in through his 25-plus years in migration and financial services.

“We are seeing more clients refinancing with these unprecedented low interest rates, and migrants wanting to return back to Australia are re-entering the property market to secure a property for their return,” Mr Douglas said.

“Given the relative safety from COVID-19 in Australia is it any wonder those Aussies living abroad are trying to get back?

“We’re not surprised, it’s certainly been keeping us busy.”

With the mortgage cliff around the halfway point of its gradual transition from low fixed to high variable rate loans, is a looming disaster unfolding or are borrowers proving to be more resilient than expected?

It’s late August and the midway point of what was dubbed the mortgage cliff.

This so-called cliff was named to denote the lemming-like fate that supposedly awaited all who had to move from super low fixed term loans secured from mid-2020 to mid-2022 to loans up to triple that interest rate.

While its progression is far from complete, and much of the impact of this mass switch may still be yet to play out in full, the doomsday scenarios have not eventuated at this stage at least.

There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings over the past few weeks.

But overall, the risk of arrears and default remains contained within Australia’s large mortgage market and a level of resilience demonstrated amid tight labour market conditions.

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season.

While homeowners are, in broad statistical terms at least, not selling up en masse, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

“The Mortgage Cliff Was All Media Hype” – Helen Avis, Director of Finance, Specialist Mortgage

The number of Aussie home loan holders refinancing soared 13.8 per cent in the financial year just completed, while those signing new mortgages fell 20.6 per cent, new research from PEXA shows.

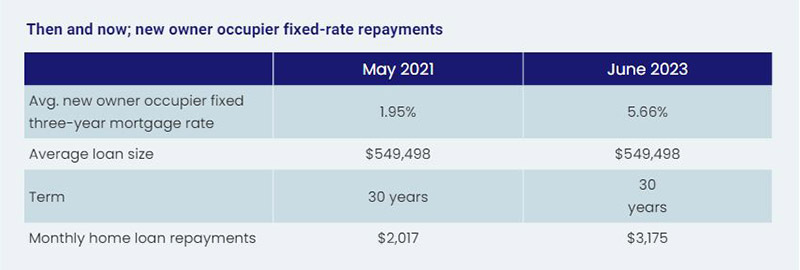

That comes as mortgage holders contend with a transition from interest rates on a loan of around 1.9 to 2.5 per cent leaping to between 6 and 7 per cent.

In terms of what that means to a household’s budget, the repayment on a $750,000 mortgage set at 2 per cent would soar from $3,180 a month to $4,830 a month – an increase of more than 50 per cent overnight, assuming a new rate of 6 per cent.

Yet it seems official data on mortgage stress has not seen a blow out in arrears amid the expiry of low fixed-term loans.

Portion Of Outstanding Loans In Arrears

Eliza Owen, Head of Residential Research Australia, said as home values rise, the risk of default also remains low.

“As what is likely to be the last of the RBA’s rate hikes is passed through to households with a mortgage, there may be a mild deterioration in housing market conditions if new listings decisions continue to rise.

“The good news for mortgage holders is that this period of economic slowdown will also take the RBA closer to its long-term inflation target, which could be the impetus for a reduction in the cash rate in the second half of 2024, as predicted by most major banks.”

Whether there is another 0.25 per cent increase in the official cash rate by the RBA is an even money bet. But the governor, Philip Lowe, used the just-released RBA Board Minutes for August to acknowledge the mortgage cliff was a consideration in their decision-making process around interest rates.

“Members noted that banks had continued passing increases in the cash rate through to their customers, and that outstanding mortgage rates and scheduled mortgage payments were set to increase further as a high share of fixed-rate loans roll onto higher rates through the rest of 2023.

“Scheduled mortgage payments as a share of household disposable income increased to 9.4 per cent in the June quarter, around its historical peak.

“Voluntary principal payments into borrowers’ offset and redraw accounts declined in the June quarter (while) net flows into these accounts had declined to be noticeably lower than the pre-pandemic average, consistent with pressures on disposable incomes.”

To be more concise, borrowers are hurting.

Finding more than $1,000 a month for mortgage repayments isn’t easy for everyone.

Climbing Or Falling From The Mortgage Cliff?

Industry sources are divided on just how severe the implications of the mortgage cliff’s continued unfolding will become. Some argued it was driven by an excitable media while others declare it’s downward spiral with no imminent escape route.

In the former camp, Helen Avis, Director of Finance at Specialist Mortgage, said “the mortgage cliff was all media hype.”

“I cannot see rates rising too much further, and if that is the case then we should not see much more of an adjustment from where we are at now.

“I am not surprised with the lack of delinquencies, with the still relatively strong property market and borrowers able to handle the increases.

“That said some borrowers have been affected and are struggling but the vast majority seem to be coping.

“I know some first home owners who have rented their property and gone back to live with parents, capitalising on the acutely tight rental market to offset the stress of higher mortgage repayments.”

Joe White, President, Real Estate Institute of Western Australia (REIWA), said we are well into 2023 and we have not seen the apocalypse we were told was coming.

“While there have been constant predictions of a flood of forced sales, REIWA data does not yet show an increase in properties advertised as mortgagee sales or mortgagee in possession.

“There is no denying 12 interest rate increases have had an impact on households, but it is disingenuous to underestimate a homeowner’s capacity and willingness to adjust their spending habits.

“Many homeowners on fixed rate loans have prepared for the dreaded mortgage cliff.

“They have paid extra onto their mortgage to be ahead with their repayments, have created a savings buffer or have refinanced.”

API Magazine’s recently released Property Sentiment Report found that the percentage of respondents defining their situation as being in mortgage or rental stress was easing.

While still disturbingly high at 36 per cent, it was an improvement on the 43 per cent of the previous quarter. Disconcertingly, 79 per cent said their financial stress status had eventuated over the past 12 months.

Mark Bouris, Executive Chairman, Yellow Brick Home Loans, however, was far less optimistic than others, reporting that the consequences of the interest rate hikes won’t be fully laid to bear until Christmas this year, as more and more home loans move from cheap fixed rates to high variable rates.

“Expect families to be forced to sell their homes, many to property investors and foreign buyers, and end up in the already-crowded rental market that is driving up inflation.

“Otherwise, families will be forced to cut back their spending on everything from holidays to food to recreational activities and school fees – the list goes on.

“This will hurt the small businesses that rely on consumer spending to pay their bills, which are also rising.

“It’s a vicious cycle, and there’s no clear way out.”

There has been a sharp spike in landlord exits from the property market across Australia.

Victoria is the worst-hit state, with the latest PropTrack figures revealing 30.1 per cent of sales were properties that had been listed for rent since they were purchased.

That’s up from 24.7 per cent in July 2022, and 16.9 per cent in July 2019, before the pandemic. New South Wales followed at 28 per cent, which like Victoria, was also the state’s highest share of investment home sales since late 2018. Queensland was third with 27.15 per cent of sales in July being rental properties.

Regardless of which side of the fence you sit on in terms of the mortgage cliff’s ultimate impact, the rest of the year promises to offer compelling viewing of the economy, housing market, and the financial viability of renters, home owners and investors alike.

Article Q&A

What is a mortgage cliff?

The mortgage cliff refers to the sudden large increase in repayments mortgage holders on fixed rate loans will face when their term ends and their loans revert to variable, and the subsequent effect this will have on the property market.

What has been the impact of the mortgage cliff?

While its progression is far from complete, the doomsday scenarios of the mortgage cliff have not eventuated at this stage at least. There has been a slowdown in economic activity and housing market momentum in response to higher rates across all mortgage holders, while CoreLogic has recorded an unusual increase in new listings.

Will property prices fall because of the mortgage cliff?

Property prices have remained resilient for most of 2023 but buyers and sellers alike are eyeing off a crucial spring selling season. While homeowners are, in broad statistical terms at least, not selling up en masse because of the mortgage cliff, they are taking steps beyond trimming the socialising budget to meet these new, sometimes dramatically higher, repayment levels.

East Coast investors are drawn to the perfect storm that is pushing up Western Australia’s house prices faster than in any other state.

With the property market continuing to heat up in Western Australia, investors from interstate have shown an increasing interest in buying Perth property.

At a recent presentation to UDIA WA members in Perth, REA Group Economist Anne Flaherty said investor activity in WA had ‘surged’, with the portion of investors in WA property increasing by 53 per cent over the year to May 2024.

Admittedly, this surge is coming off a low base, given investors have been scarce in the WA market in recent years, likely due to a range of factors including the five-year downturn the WA property market experienced in the lead up to 2020, rising interest rates, restrictions during the pandemic and rental reforms causing uncertainty.

It is also important to note that, according to the Australian Bureau of Statistics, the portion of investors in WA in January to May this year was still only 36 per cent, which, while up from 29.5 per cent last year, still remains far less than owner occupiers (42 per cent), combined with first home buyers (21 per cent).

According to UDIA WA’s Urban Development Index, 32 per cent of new land sales in the Perth metropolitan area were to investors in Q1 2024, with 34 per cent to first home buyers and the remaining 34 per cent to owner occupiers. This breakdown is compared with 2021, when the portion of investors in the new land market was just 17 per cent.

East coasters targeting WA property

East Coast investors are no doubt recognising the perfect storm that is pushing up WA’s house prices faster than any other state.

While Perth remains one of the most affordable capital cities in Australia, that mantle is slipping as, according to the PropTrack Home Price Index for June 2024, the annual growth rate for median house values in Perth was the highest for any other capital city, at 22.5 per cent over the last financial year.

Some of the most significant price growth has occurred in Perth’s northern and southern growth corridors, as well as regional centres such as Bunbury and Mandurah.

That growth is likely to continue as, according to Ms Flaherty, WA continues to grapple with our housing supply shortage over the next three years at least.

Ms Flaherty highlighted what many of us in the industry here in WA are already acutely aware of, and that is our booming population growth, strong economic growth and dire housing shortage that has been compounded by the longer time it takes to build a new house in WA compared to anywhere else in Australia.

This is heating up demand while we struggle to deliver enough supply. In fact, UDIA WA has forecast a shortfall in excess of 30,000 dwellings over the next five years.

The rental market is also experiencing escalating prices, with Perth rents growing 18 per cent over the last year to $640 per week according to PropTrack. This is in the context of a 0.5 per cent rental vacancy rate.

All these factors are contributing to investor interest in our market as they recognise the potential return.

Why investors should be welcomed in WA

While we have seen some negative press recently around the increased appetite from investors wanting to enter the WA market, it is important to understand that investors are a critical ingredient in boosting housing supply, particularly in the rental market.

We have seen the impact that an exodus of investors has had on the Perth apartment market in particular in recent years, with the challenge in securing sufficient presales stalling many potential projects.

According to Urbis, only 441 new apartments were available for sale in Q1 2024. That is compared to more than 1,500 in Q3 2021. New apartment approvals are also at their lowest level since 2009.

There are several factors influencing the lack of new apartment projects getting off the ground in WA, but a big factor is securing presales to appropriately finance a project.

Investors are an important source of presales and are desperately needed to assist with getting more apartments onto the local market.

While there is some fear mongering from some quarters about the impact of investors on our already tight housing supply, the fact is that investors are important in getting stock on the market.

This is especially the case if they are buying new house and land or apartments, as these contribute to getting more new stock on the ground and available to renters.

Tax reforms needed

UDIA WA continues to advocate for a range of recommendations to get more homes on the ground in WA, faster.

In terms of attracting further investment in the housing market, we believe there are property tax incentives that can be implemented in the short term, including making the transfer duty concession for pre-construction and under construction apartments permanent, extending it to grouped dwellings, and removing the purchase price thresholds.

We are also asking for the land tax exemption for build-to-rent projects to be increased, and for the Foreign Buyer Surcharge to be removed or at least frozen for two years.

We believe these particular changes could boost investment in the WA market and hopefully get more supply on the ground, meaning more homes for the people that so desperately need them.

Article Q&A

How active are property investors in Western Australia?

According to the Australian Bureau of Statistics, the portion of investors in WA in January to May this year was still only 36 per cent, which, while up from 29.5 per cent last year, still remains far less than owner occupiers (42 per cent), combined with first home buyers (21 per cent).

How bad is the housing crisis in Western Australia?

UDIA WA has forecast a shortfall in excess of 30,000 dwellings over the next five years.